Guidance and expertise

Citizens Securities Advisors will help you implement a disciplined process to help balance competing priorities and reach your short- and long-term financial goals.

Save and grow your money*

- Buy a home or vacation property

- Save for college

- Start a business

- Save and invest for retirement

Prepare for retirement

- Invest your retirement savings*

- Manage your retirement income

- Generational planning strategies

Protect your family

- Protect your family with term life or whole life insurance

- Ensure future college expenses are covered

- Cover future funeral expenses

Transition your wealth

- Create a comprehensive estate plan

- Minimize estate taxes

- Protect your heirs

Financial planning designed for you

Receive a personalized plan aimed at helping you save and grow your money, secure your income, protect your family, and transition your wealth.*

Clarifying goals

Creating the right approach for your personalized financial plan begins with understanding your ambitions and setting clear objectives.†

Assessing your situation

Examining where you are in life - along with where you'd like to go - will inform a plan that evolves with you and your family.†

Looking at the journey ahead

Planning involves preparing for possible "what if" scenarios so that you can be prepared for important financial decisions you might encounter in the future.†

Support your business

Select from a full range of retirement accounts, including 401(k) Plans, SIMPLE IRA Plans, and Simplified Employee Pension Plans. We can also provide solutions to protect your business and personal assets and assist you with your business succession plans.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

FINRA BROKERCHECK: Check the background of Citizens Securities, Inc. on FINRA BROKERCHECK.

Citizens Securities, Inc. Business Continuity Plan

Citizens Securities, Inc. Managed Account Program Form ADV Disclosure Brochure

Citizens Securities, Inc. Digital Advisory Program Form ADV Disclosure Brochure

Quarterly Order Routing

Reg.BI Disclosure

Form CRS

Fiduciary Acknowledgement

Citizens Private Wealth Form ADV Disclosure Brochure

CRS Citizens Private Wealth

Fiduciary Acknowledgment Clarfeld

CSI Deposit Sweep

Risk of Investing: All investing involves risk, including the risk of loss of principal. Investment risk exists with equity, fixed income, and other marketable securities. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

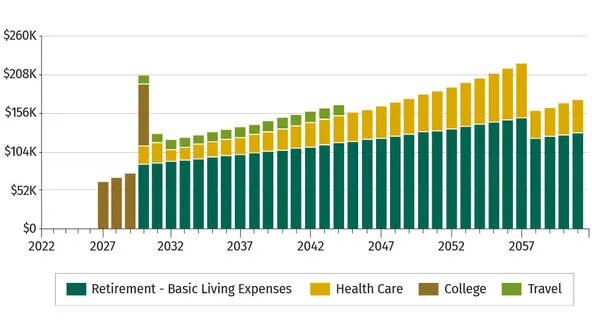

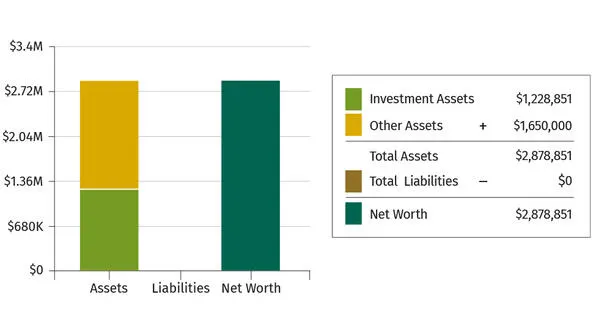

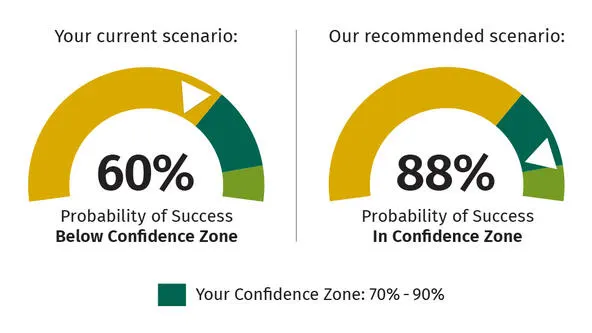

Charts: All charts are constructed with sample data and are for example purposes only.

Content Not Advice: This content is intended for informational purposes only and should not be construed as advice. Citizens Securities, Inc. does not provide legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

Investment Decisions: The investment products and financial strategies suggested herein are subject to investment risk, including possible loss of principal amount invested. There can be no guarantee the suggested strategies or investments will lead to successful outcomes. Investment decisions should be based on each individual's goals, time horizon and tolerance for risk.

Citizens provides Wealth and Investment services in the United States: AL, AK, AR, AZ, CA, CO, CT, DC, DE, FL, GA, HI, IA, ID, IL, IN, KS, KY, LA, MA, MD, ME, MI, MN, MO, MS, MT, NC, ND, NE, NH, NJ, NM, NV, NY, OH, OK, OR, PA, RI, SC, SD, TN, TX, UT, VA, VT, WA, WI, WV, WY.

Citizens Wealth Management: Citizens Wealth Management (in certain instances DBA Citizens Private Wealth) is a division of Citizens Bank, N.A. (“Citizens”). Securities, insurance, brokerage services, and investment advisory services offered by Citizens Securities, Inc. (“CSI”), a registered broker-dealer and SEC registered investment adviser - Member FINRA / SIPC. Investment advisory services may also be offered by Clarfeld Financial Advisors, LLC (“CFA”), an SEC registered investment adviser, or by unaffiliated members of FINRA and SIPC providing brokerage and custody services to CFA clients (see Form ADV for details). Insurance products may also be offered by Estate Preservation Services, LLC (“EPS”) or an unaffiliated party. CSI, CFA and EPS are affiliates of Citizens. Banking products and trust services offered by Citizens.

SECURITIES, INVESTMENTS AND INSURANCE PRODUCTS ARE SUBJECT TO RISK, INCLUDING PRINCIPAL AMOUNT INVESTED, AND ARE:

· NOT FDIC INSURED · NOT BANK GUARANTEED · NOT A DEPOSIT · NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY · MAY LOSE VALUE