The employee benefit that 7 in 10 middle-market companies are using to compete in a tight labor market

By Kavita Kurella | Director of Product Strategy and Merchant Services

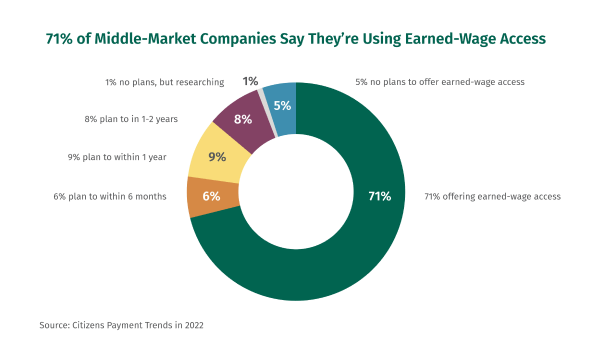

In a competitive employment market, companies have to be strategic about attracting and retaining workers—but it’s not just a matter of higher wages. One benefit that’s increasingly popular with employees is on-demand access to earned pay. Our 2022 Payments Pulse survey found that seven in 10 middle-market companies were offering earned-wage access (EWA) to some employees today. Another 24% said they were planning to implement earned-wage access in the near future, leaving a mere 5% of respondents who said they had no plans to offer earned-wage access.

Read more: 2022 Payment Trends

Our survey of 200 companies tracks the payment trends in middle-market businesses. Find out what treasury executives said about digitization tools, new payment methods, and more.

Earned-wage access is when employees can withdraw and have access to a percentage of their accrued pay on-demand, rather than waiting for the traditional weekly or biweekly payday. The practice goes by many names, including on-demand pay and instant pay.

EWA stood out in our survey for its high adoption among middle-market companies. Real-time payments, another tech on the rise, are currently in use by 51% of companies. And social tokens, where a user’s phone number or email address are used for transactions rather than their bank account information, have gained ground in peer-to-peer payments but only 36% of middle-market firms expressed strong interest in using them to request payments.

Understanding earned-wage access

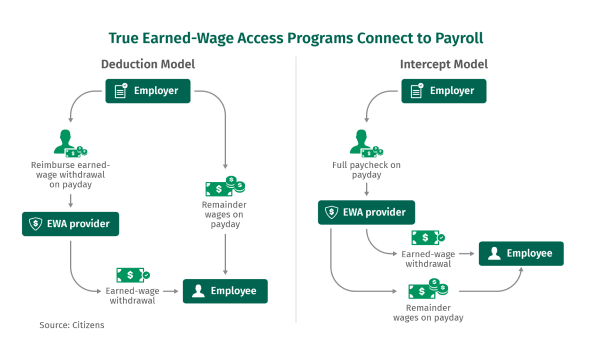

In order to provide access to earned wages, EWA providers connect directly to the employer’s payroll function. EWA models generally follow two forms. The first version is called the deduction version. In this model, the EWA provider funds the earned wage withdrawal, and at the end of the payroll cycle, the employer reimburses the EWA company and separately sends the remaining wages to the employee. The employee pays a small fee to the EWA company for this service. In some cases, there is no fee if the employee has the earned wages sent by ACH or funded to a pay card.

The second payroll-connected EWA model is the intercept model. In this form, the EWA provider funds the earned wage withdrawal as needed. At the end of the payroll cycle, the employer sends the employee’s full wages to the EWA company, which deducts the portion already disbursed and then sends the rest of the wages on to the employee. Again, a small fee may be paid by the employee, depending on the withdrawal option they choose.

In both of these EWA models, the EWA provider is connected to payroll and time and expense records through the employer. Both models also, importantly, allow employers to enable EWA without disrupting working capital or payroll administration. From the employer’s perspective, payroll remains on the regular cash flow cycle.

A means of relieving financial stresses

Some think of EWA as a tool mainly for low-income workers. Advocates point out that access to pay allows workers to avoid late fees, penalties, overdraft fees, credit card interest, and even high-interest payday loans. Indeed, EWA has become mainstream across low-wage retail, rideshare, and fast-food companies, embraced early by major brands like Walmart, Uber and McDonald’s.

Research from EY found that 70% of workers in the U.S. face financial stress regularly. 35% report that they have encountered shortfalls in cash between paychecks—and that the mismatch happens approximately every four months.

While the lowest income brackets undoubtedly face the steepest financial stressors, the burden of living paycheck to paycheck is common across higher income levels as well. Among those earning $10,000, 40% report financial shortfalls. But among those earning $100,000 or more, 30% report shortfalls. According to EY’s analysis, debt is a key factor. People with higher debt levels are much more likely to face a cash crunch, whether they are high earners or not.

Appealing to workers in a tight market

Relief from inter-payday financial stress may be the primary mission of some EWA advocates. But on-demand pay has broad appeal. 83% of workers believe they should have access to their pay daily, according to a recent Harris poll. At that level of popularity, EWA is not just a function of relieving financial stress—it’s the mainstream preference for pay.

Popular pay benefits could translate to a competitive edge in a tight labor market. In the Harris poll, a majority of workers also said that free on-demand pay would increase their loyalty to an employer and make them feel more valued as an employee. It could even be the deciding factor in securing workers from competing jobs; 81% said they would take a job with no-cost EWA over an employer that does not.

A benefit that would tip the scales for 8 in 10

- 83% believe they should have access to earned wages at the end of each day/shift

- 80% would prefer to have pay automatically deposited as they earn it

- 78% said free access to pay would increase their loyalty to their employer

- 81% would take a job with an employer that provides free access to on-demand wages over an employer who does not

Source: The Harris Poll

In an economic cycle marked by historically high inflation and full employment, competing for talent is a challenge. In early 2022, job openings remained near record highs in the U.S., according to Reuters. Meanwhile, the Atlanta Federal Reserve reported wage inflation at a three-month moving average of 5.8% year over year. Before the pandemic, it measured around 3.5%. But higher wages are just a symptom of dynamics in the labor market more broadly. Labor-force participation remains low, with the latest reading showing 62% of the American population working or looking for work—a level not seen since the late 70s, not including the recent pandemic dip. Between the aging workforce, pandemic-induced early retirements, and lower-than-projected immigration levels, some believe the worker shortage could take years to resolve.

Catching up to competitors

Looking at the 5% of middle-market companies who said they do not plan to implement EWA, six in 10 said that accounting complexity was a reason. The same share said they weren’t convinced of EWA’s value to employees. About a third noted cash-flow or tax-reporting concerns with the practice.

Reasons for not implementing earned-wage access

|

Accounting complexity

|

61% |

| Not convinced about its value | 61% |

| Creates too much of a cash flow challenge (impacts forecasting ability and liquidity) | 35% |

| Tax problems with reporting | 31% |

Source: Citizens Payment Trends in 2022

EWA has already garnered high interest from employees, and it’s also increasingly sought after by employers. As a maturing service that has been in the market a decade, based on the 2011 founding of PayActiv according to Ernst & Young, employers may be surprised to learn how flexible and accommodating an EWA provider can be. And with more than 70% of middle-market companies reporting that they already use EWA, it seems likely to move soon from “edge” to “norm.” Middle-market companies can potentially use EWA to their advantage now, or suffer the disadvantage of not embracing a benefit that peers are using.

Three actions to consider:

- Learn more about earned wage access. EWA programs encompass a number of providers and business models. Explore the possibilities for your industry and review some of the publicly available surveys and white papers on the subject.

- Address the concerns of your management team. For businesses worried about the accounting or cash flow implications, the mainstream EWA providers use models that leave pay cycles undisturbed with no impact to working capital, from the employer’s perspective.

- Consider a pilot program. Many companies have some share of seasonal or contract workers. Consider launching a test program to see if it is an appealing benefit to your employees and work through some of the logistics of getting EWA started at your firm.

Kavita Kurella is Director of Product Strategy and Merchant Services. She has over 20 years of global management consulting and corporate experience. Kavita leads treasury management initiatives that enable Citizens commercial customers to achieve their strategic business objectives and stay competitive among their peers.

Related Reading

Payment trends in 2022

Access insights from 200 middle-market treasury executives on how they view the latest payment-processing trends.

Essential strategies to optimize corporate travel financial management

Traveling for business is presenting new and renewed challenges for mid-market companies. Refresh your strategic thinking on employee travel and expense management with timely insights.

Mitigate fraud with virtual cards

Virtual Card Payments can help fight Accounts Payable fraud and increase efficiency through digitalization.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE