By Cecilia Loftus, Managing Director, and Head of ESOP Banking Services | Published May 2024

Key takeaways

- Employee Stock Ownership Plans (ESOPs) allow business owners to create liquidity and diversify their investments while helping employees to build wealth and save for retirement.

- Structured correctly, an ESOP can confer greater financial benefits and better succession planning for the business than a sale to a strategic buyer or private equity firm.

- The complexity involved with setting up and maintaining an ESOP means a company needs to work with a savvy group of ESOP experts: advisors, trustees, lawyers and bankers.

Employee Stock Ownership Plans (ESOPs) are a way for business owners nearing retirement to create some liquidity and diversify their investments, while giving employees an effective way to save for their own retirement. According to the National Center for Employee Ownership (NCEO), employees in ESOPs have twice the retirement savings as those not participating in ESOPs. These benefits are all the more important as the US population ages—a record number of Americans are turning 65 in 2024 (4.1 million), with the surge continuing through 2027, according to the Alliance for Lifetime Income.

Moreover, companies with ESOPs perform better than non-ESOP peers, with 2.3% higher sales and 10% higher profit margins, according to the ESOP Association. While the benefits are significant, ESOPs are also complex to set up and maintain, which dissuades some owners from pursuing them. But with the right set of professional advisors, trustees, lawyers, and banks, it’s a manageable and potentially advantageous undertaking.

The benefits of ESOPs

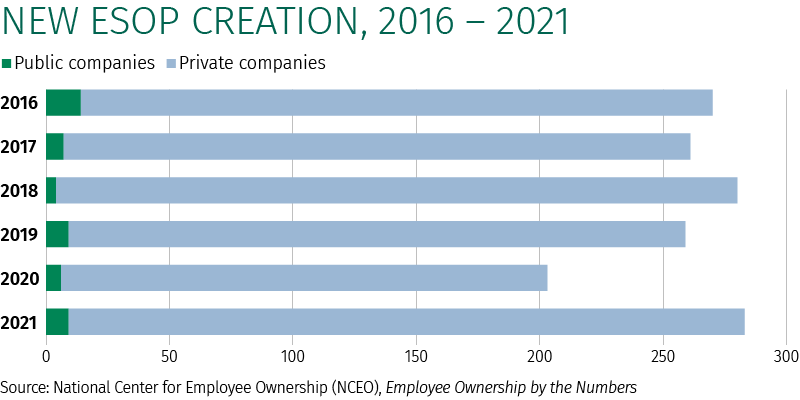

According to the NCEO there are about 6,500 ESOPs in the U.S. holding $2.1 trillion. Since 2016, an average of 259 new ESOPs have been created each year.

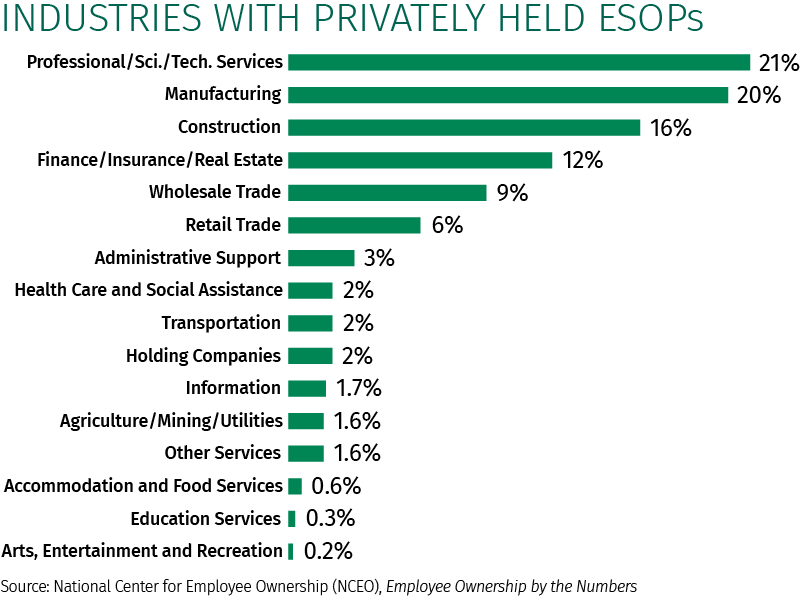

Any type of company can set up an ESOP, although three industries account for more than half of all ESOPs: professional services (21%), manufacturing (20%) and construction (16%). According to the NCEO, 57% of ESOPs involve private companies with less than 100 participants, and less than 10% of ESOPs are public companies.

Business owners might not realize that a properly structured ESOP, taking full advantage of various tax benefits, can create an equivalent or better financial outcome and succession planning for the business than selling a stake to a strategic or private equity buyer. ESOPs allow the owner to diversify his or her holdings while still maintaining control as corporate governance remains basically unchanged. Owners avoid sharing decision-making with a strategic buyer in the boardroom or a private equity buyer looking for an exit in three to five years.

Another consideration for owners is how ESOPs can benefit the local community by building the wealth of employees. Many owners are deeply invested in their towns and cities and want to see their communities and their employees thrive. Their business is their legacy, and they often worry that a sale could mean their life’s work closing or moving locations. Also, by giving employees an ownership stake and aligning financial interests, employees are even more committed to the company. The NCEO notes that voluntary quit rates at companies with ESOPs are about one-third the national average. In a related finding, the ESOP Association found that 80% of ESOP business leaders feel they do a better job than non-ESOP competitors recruiting and retaining workers.

The challenges and costs

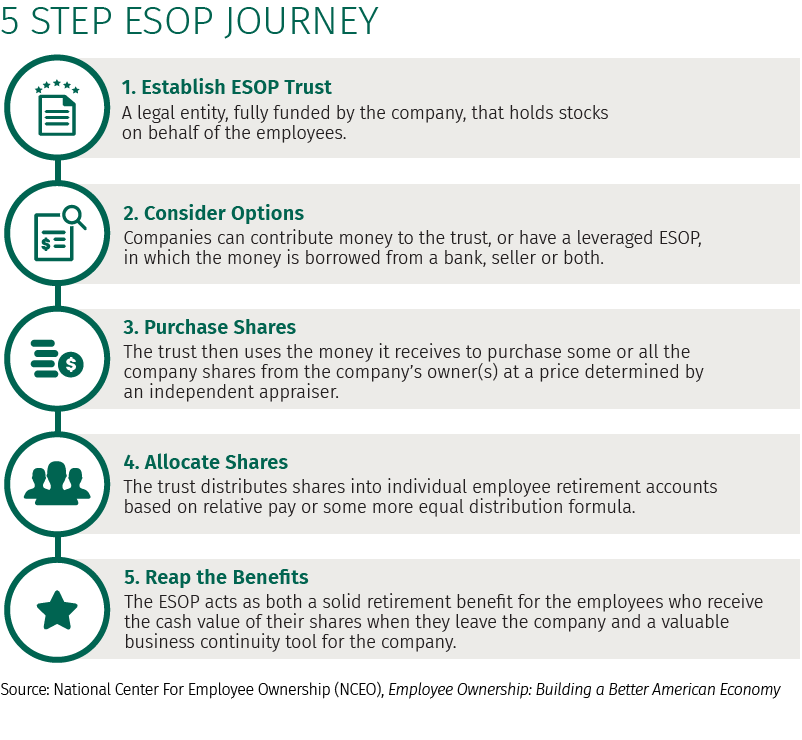

While ESOPs have many benefits, setting up and administering an ESOP is complex. The business owners sell some or all of their shares to an ESOP trust, which owns those shares on behalf of employees. ESOPs can be funded in many ways, but usually the transaction involves a loan. The company can take out a loan and then reloan the funds to the ESOP trust. The company makes contributions to the trust, which the trust uses to repay the loan. As the loan is repaid, shares become available to allocate to employee accounts.

Because the government allows tax advantages, the paperwork and approvals can take several months to assemble and complete, including management interviews and site tours. For example, regulators scrutinize these transactions to ensure stock values are not inflated. The ESOP trust is a financial buyer and overpaying for the asset can result in significant penalties for the seller and the company. The amount of senior financing secured for the transaction must be appropriate, allowing the company to comfortably pay down the facility and continue operations. And, of course, the company must continue to administer the plan in accordance with federal laws and regulations that govern issues such as contribution and allocation limits, vesting, benefit distributions, diversification, and more.

This complexity and regulatory scrutiny are why a company considering an ESOP must assemble a good team. This should include an advisor to the company, an ESOP trustee, financing bank, and specialized ESOP attorneys. While the structuring advisor (e.g., a boutique investment bank) bows out after the ESOP is created, the trustee, legal advisors on both sides, and a bank advisor continue to work with the company to maintain the ESOP, resulting in ongoing administrative costs. Additionally, since an ESOP is a qualified retirement plan, a knowledgeable administrator must regularly conduct nondiscrimination tests. Finally, in the long term, the company needs to manage cash flows carefully (as the value of the stock theoretically increases) in order to pay out employees as they leave or retire.

In short, the benefits of ESOPs for owners, employees, and local communities are compelling. But their complexity means a company must educate itself before committing. For a company just starting on this journey, connecting with the right sources to learn about ESOPs is critical. A few next steps include:

- Tap into organizations such as the NCEO, the ESOP Association, or Employee-Owned S Corporations of America (ESCA), all of whom have deep ESOP resources including data, research reports, and surveys.

- Seek out companies that have transitioned to an ESOP to hear their first-hand experiences. A lawyer or bank that specializes in ESOPs can put someone in touch with these companies.

- It’s important to interview a number of ESOP advisors to ensure the advisor is credible, experienced and trustworthy, especially since transactions are highly scrutinized by the IRS and the US Department of Labor. Again, a lawyer or bank that specializes in ESOPs can provide advisor referrals.

Cecilia Loftus is Managing Director, Head of ESOP Banking Services at Citizens Commercial Banking. For 20 years she has focused on ESOPs, working with clients on all aspects of repurchase obligation studies, sustainability planning, and ESOP structuring for initial and second stage equity sales.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE