By Andy Mertz, Managing Director and Head of Equity Capital Markets, Citizens Commercial Banking | Published July 2024

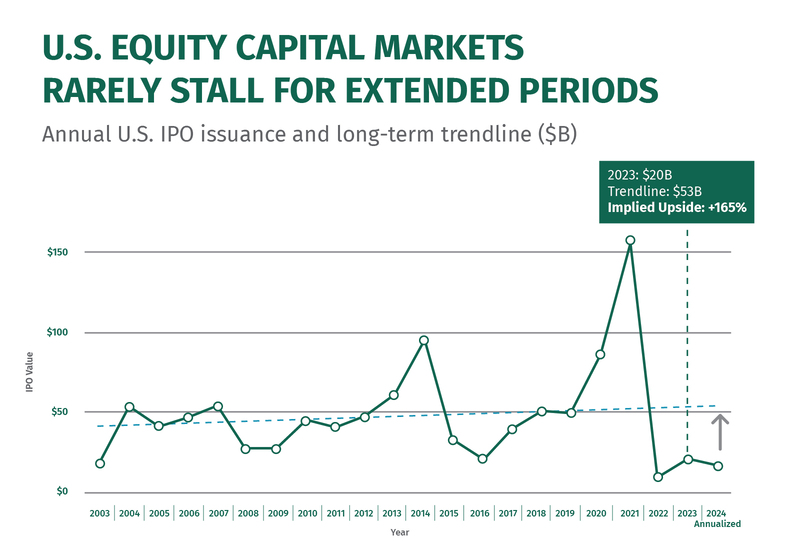

Historically, subdued Initial Public Offering (IPO) markets—like those of 2022 and 2023—rarely last for more than a few years. Over the last quarter century, U.S. annual equity issuance hovered close to a long-term trendline—a pattern suggesting a potential annual IPO market in 2024 and 2025 of approximately $53 billion. Reviewing prior IPO-volume troughs, it usually takes one to two years for markets to “reclaim” the potential represented by the long-term trendline. Given this, and with IPOs demonstrating recent below-trend issuances, a backlog of activity could be accumulating for a potential IPO market resurgence.

IPO activity can be keenly sensitive to a range of factors, including market confidence, valuations, and the cyclical state of company financials. Companies and investors need to be aware of six key factors as they consider a potential rebound for the market.

Six things needed for a sustained IPO rebound

1. A soft landing and greater macroeconomic certainty.

The economic backdrop is a critical informer of overall confidence in the capital markets—economic activity needs to demonstrate a favorable outlook for the medium term.

But it’s not just about a growth environment. A key factor is also stability of the environment—market confidence is directly connected to the certainty of the macro backdrop. If the near-term outlook comes with uncertainty, companies are unlikely to make plans for a significant issuance. A better scenario is a positive growth environment, with healthy consumer spending and capital expenditure trends paired with high confidence about near-term market balance.

2. Stability in inflation, interest rates, and volatility.

Beyond economic growth, capital raisers should watch inflation and its impact on interest rates and market volatility.

Fully tamed inflation and interest-rate cuts are not an absolute necessity for a positive IPO environment. IPO activity in the first half of ’24 shows that companies can, and will, raise capital through IPOs when rates are higher than previous periods. In fact, the longer that rates remain high, the more normalized the environment becomes for companies (and even for consumers, as trends in homebuying show a similar dynamic). Rate cuts could be another tailwind for IPOs, but they are not necessarily a condition for a rebounding IPO environment.

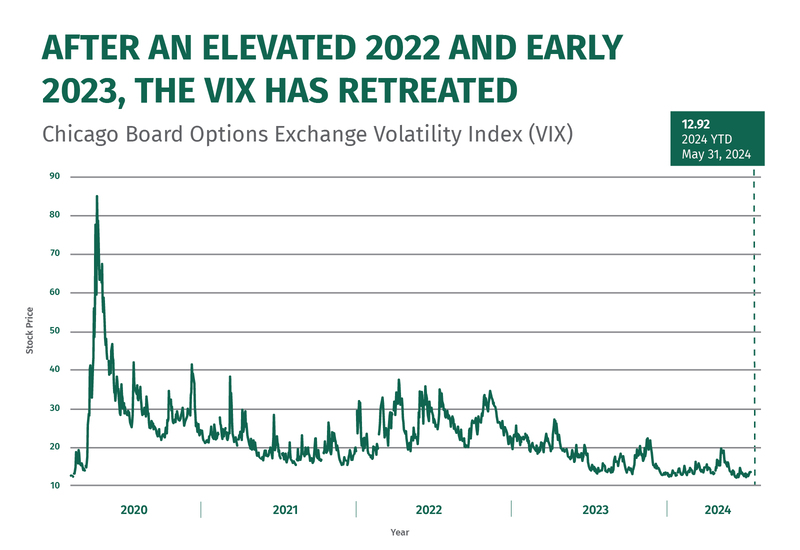

However, inflation shocks could destabilize these dynamics and drive market price volatility higher—a scenario that is not conducive to IPOs. Market volatility, as measured by the VIX (the Chicago Board Options Exchange Volatility Index), must stay in a below-20 range. When the VIX is higher, it’s a signal that the market environment is coping with a good deal of uncertainty.

3. A recent track record of IPO success.

Companies that are considering IPOs closely track the performance of recent transactions. Strong institutional demand and follow-on performance are two more signals to would-be capital raisers of a favorable market environment.

2024 is off to a good start, with tech names Reddit, Astera Labs, Kaspi.KZ, and Rubrik among the largest capital raisers, with most exhibiting strong follow-on returns. A number of consumer companies have also performed well, including Viking Holdings, Amer Sports, BBB Foods and Ibotta. There have also been strong market responses to issuance in financials, including insurance company Bowhead Specialty, as well as momentum from last year’s deals (e.g., Skyward Specialty). These favorable outcomes are providing impetus for capital raisers to execute on deals in their pipeline.

4. Sturdy valuations.

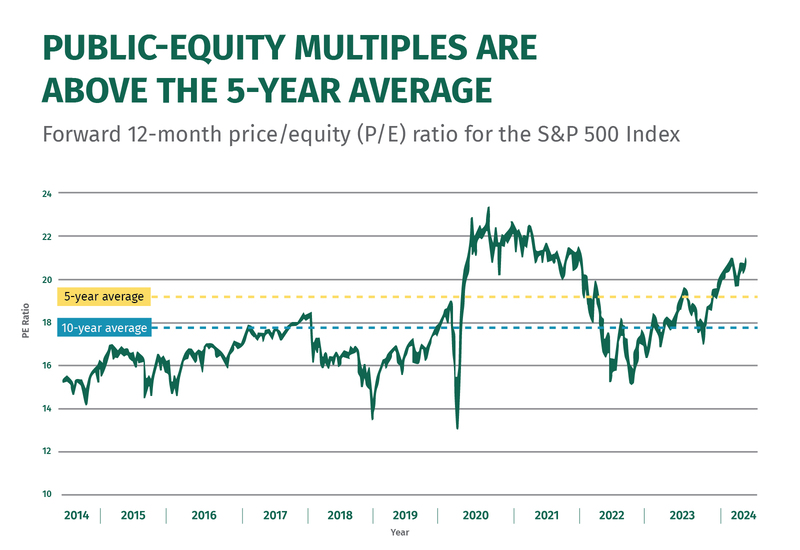

Valuations remain a critical issue in liquidity decisions. Though valuations have improved from recent lows, they have not returned to the high-water marks of 2021-2022, particularly in the technology sector. Still, multiples on sales and earnings have recovered to more attractive levels. In the public markets, S&P 500 Index pricing has been above the five- and 10-year averages for all of 2024.

For some companies considering an IPO, small-cap valuations may be a more appropriate comparison—and small caps have not yet recovered as much as larger-company peers. Small-cap benchmarks could provide a proxy for the expectations of IPO valuations.

5. Positive trends in company financials.

When evaluating an issuance, companies need to present positive year-over-year trends in the market. Company financials relate closely to the broader GDP backdrop, as better growth environments bode well for companies’ financial performance. However, profitability also depends on cost dynamics—and the inflation surge of 2021-2022 proved challenging for company financials. This year, we are seeing signs that company financials have improved. Looking at the S&P 500 Index as a proxy for broader activity, FactSet data shows that year-over-year revenue growth for companies has recovered to mid-single-digits, while earnings growth is forecast into the 15-20% range for tech sectors, an important leading actor of the IPO market. Healthcare companies, another IPO powerhouse sector, have a more modest but still positive outlook for company financials in 2024.

6. Stability in global factors.

A final factor to consider is the overall stability of global economic activity, including both growth and geopolitical risks.

Global growth has generally lagged behind the U.S., but it still remains positive overall. A May 2024 report from the OECD offered a stable estimate for annual growth, forecasting that 2024 would look a lot like 2023 for global GDP growth trends. Key metrics, such as the price of oil, have also demonstrated stability this year even as two wars continue. One wild card for 2024 is the number of elections taking place around the world, including the U.S. presidential election, which could deliver volatility to markets late in the year. However, a presidential election is not necessarily a barrier to IPO activity; the broader performance of the markets is a more important factor, historically.

A return to trendline could be in motion

If these six factors continue to improve or remain steady, then a return to more normal IPO volumes could be on the horizon. The backlog represents not just earlier-stage companies looking for a public debut; private equity also maintains a bench of pending transactions. In fact, private equity exit activity ticked steadily upward across each quarter of 2023, though average “age” of portfolio companies continues to rise within funds, representing a backlog of exits.

These factors continue to play a large role in potential IPO activity. Positive shifts in the dynamics could set the market up for a true return to more normal trendlines.

Tips for IPO readiness in 2024

Companies considering an IPO in the medium term can take steps toward readiness today:

- Seek experienced advice from a team of experts. Every market environment is unique, but there are key patterns that return time and again which an experienced advisor can help you identify. And, while market dynamics are important, a company’s IPO success will depend heavily on aligning with an advisor now to coordinate a successful IPO down the road.

- Emphasize growth opportunities. Investors are focused on durable growth stories that are profitable (or at least near breakeven) with solid unit economics and a sustainable advantage. Set expectations that are consistent with the opportunity and control the narrative by meeting with public investors and or participating in conferences prior to the IPO process officially starting.

- Stay informed on trends. Seek out market updates with the latest trends in IPO and other capital market activity, which can be a valuable input to your own company’s plans.

Andy Mertz is a Managing Director and Head of Equity Capital Markets at Citizens JMP. Citizens is a fast-growing provider of investment banking services with a broad platform featuring M&A, debt, and equities sales, trading, and institutional research services.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE