Key takeaways

- Midsize companies are digitizing their payment processes to improve cash management efficiency, financial visibility and control and cash flow forecasting.

- More companies adopt Real-Time Payments (RTP®) as banks expand enablement.

- Midsize companies capture greater value from the seamless integration of payments with existing treasury processes.

- Checks remain an important payment option for many companies, driven by vendor and contractor preferences.

- Midsize companies using machine learning and AI for fraud mitigation report lower incidences of fraud.

Digital Adoption Results In Improved Cash Flow and Control

For Citizens' fifth annual survey on payment trends, we surveyed executives at midsize companies with primary or shared decision-making responsibility for their organization's treasury functions. All respondents worked for companies in non-banking industries with annual revenues of between $5 million and $1 billion.

In this report, smaller midsize companies are those with annual revenues between $5 million and $50 million and larger midsize companies are those with annual revenues between $50 million and $1 billion.

The survey finds that treasury leaders at midsize companies are increasingly recognizing the benefits of digital payment technologies. The move away from paper-based to digitized workflows in treasury functions is resulting in improved cash management efficiency, enhanced visibility/control and refined cashflow forecasting.

In addition, midsize companies are embracing real-time monitoring and two-factor authentication to stay a step ahead of an increasingly sophisticated fraud environment.

RTP Leads All Instant Payment Methods Because Banks Enable It Within Existing Treasury Workflows

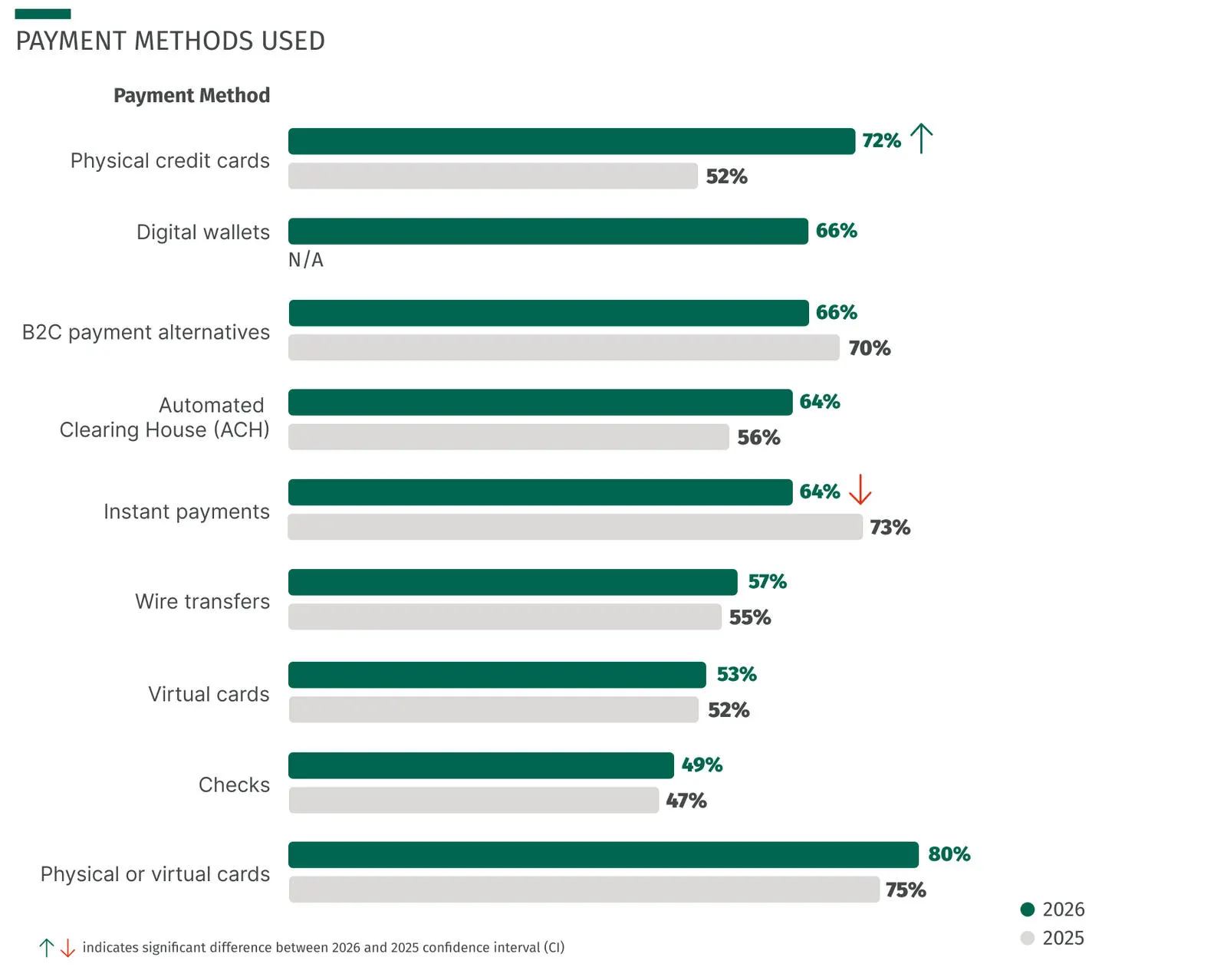

The use of instant payments by midsize companies fell from 73% to 64% in the past year. Instant payments were largely replaced by physical credit cards (which jumped from 52% to 72%), ACH and digital wallets (a choice newly added to the survey this year). It's important to note that instant payment usage may not truly be falling; these results may be reflective of category dilution as instant payment options are more often presented alongside ACH.

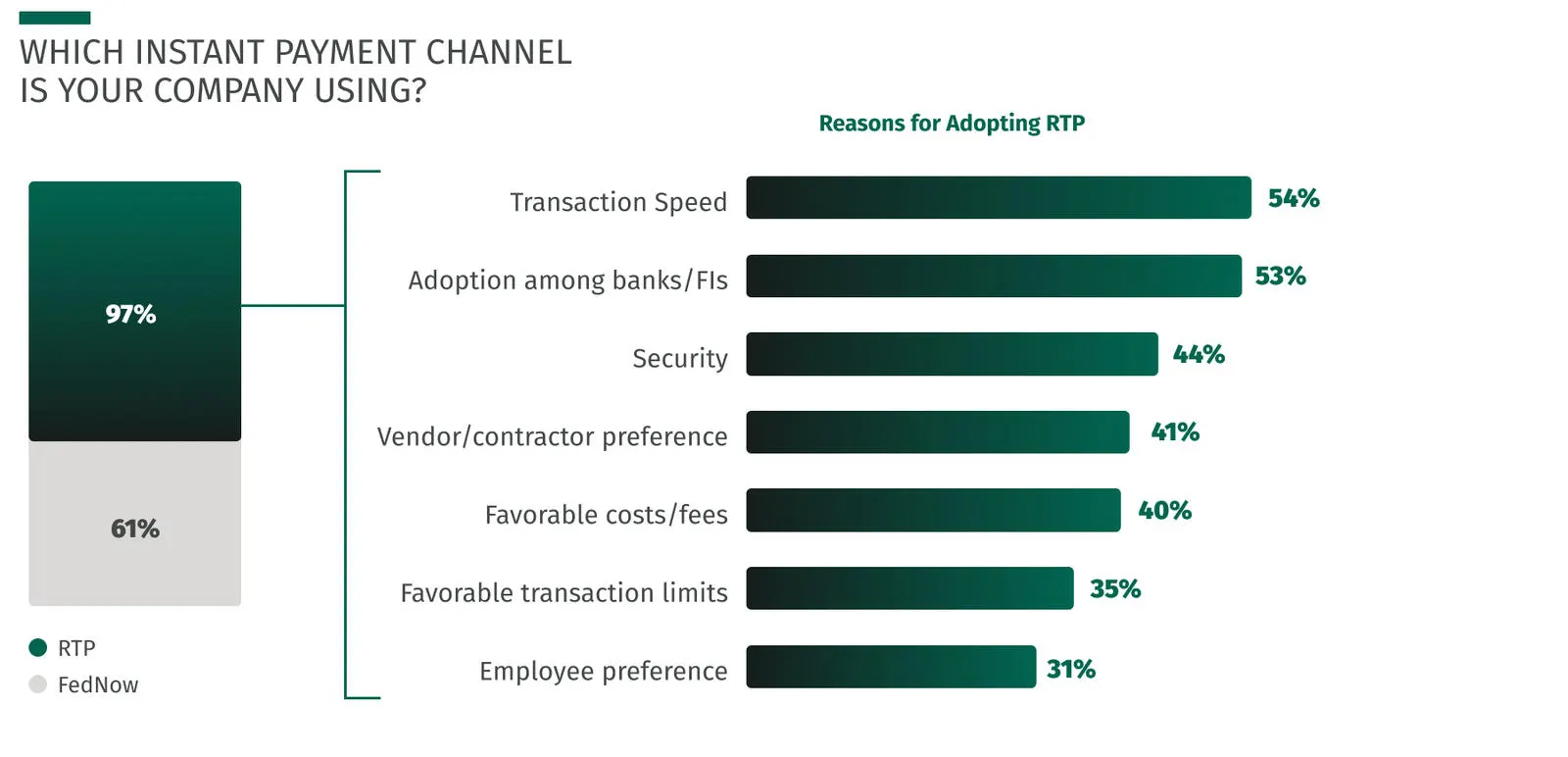

Within the cohort of companies that currently use instant payments, the RTP® network from The Clearing House (RTP) remains the leading method, increasing its stranglehold from 91% in 2025 to 97% in 2026. Comparatively, the usage of FedNow® has remained roughly flat year over year at 61%. Respondents cited transaction speed (54%) and financial institution adoption (53%) as the leading reasons for adopting RTP.

-

"The real shift in 2026 isn't just faster payments. It's embedding those capabilities directly into how clients operate. Treasury leaders don't want another channel. They want their bank seamlessly integrated into their ERP and workflows. Open Banking and Commercial APIs are making that possible, bringing real-time connectivity, payments, data and insights into the systems clients already use. The institutions that win will be the ones that meet clients where they are, combining connectivity, simplicity and trust into the core of the experience."

Michael Cummins

EVP, Head of Treasury Solutions and Payments

Midsize Companies Continue To Use Checks For Paying Vendors and Contractors

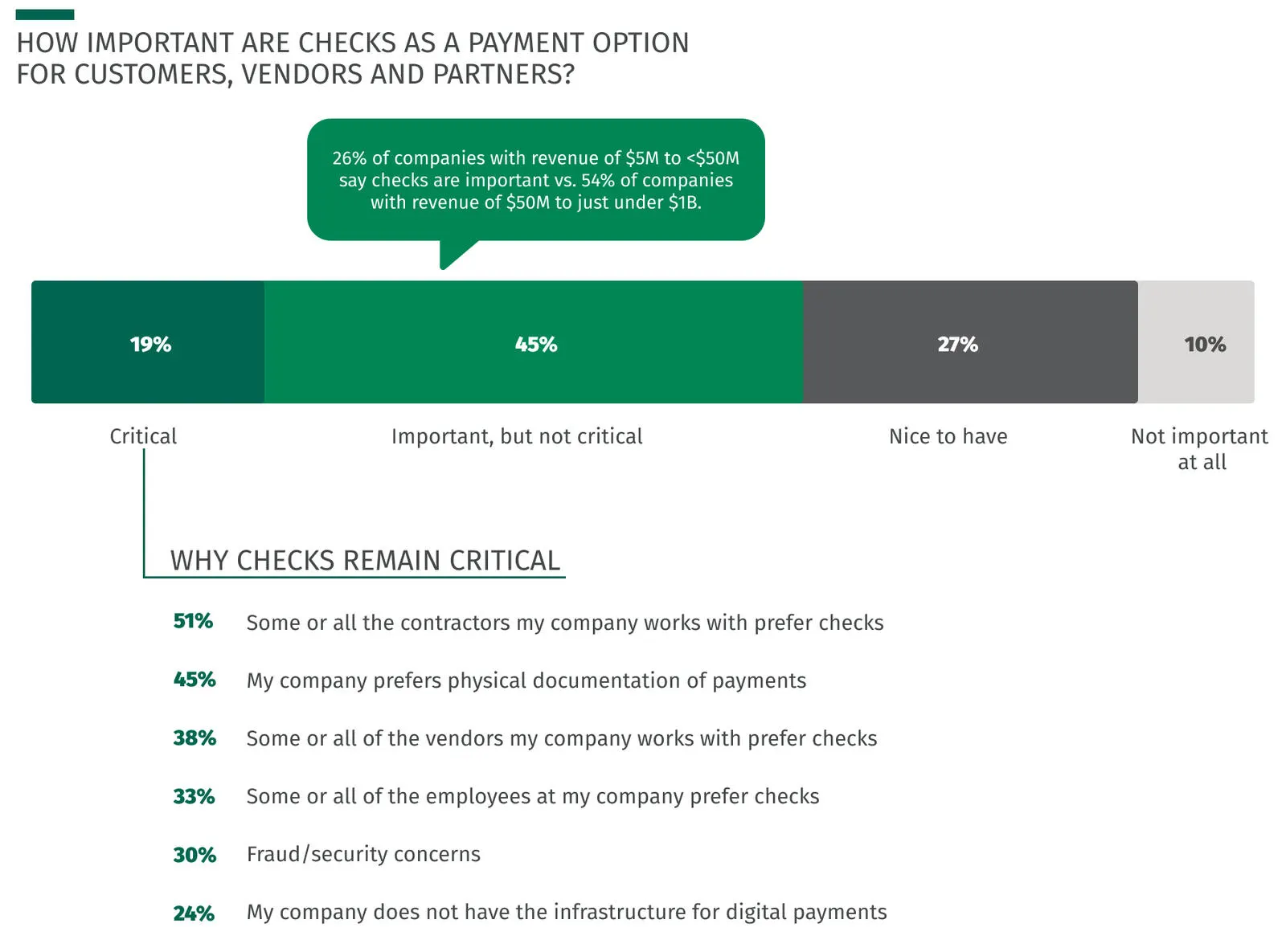

Although just 19% of respondents cite checks as a critical payment option for their customers, vendors and partners, 64% state it still has value for this purpose.

This importance is significantly higher for larger companies as compared with smaller organizations, as 54% of companies with annual revenues of $50M to $1B say checks are important (but not critical), compared with just 26% of companies with revenues of $5M to $50M.

Of those respondents that cite checks as a critical payment option, 51% noted a preference for checks among their contractors, and 38% cite vendor preference.

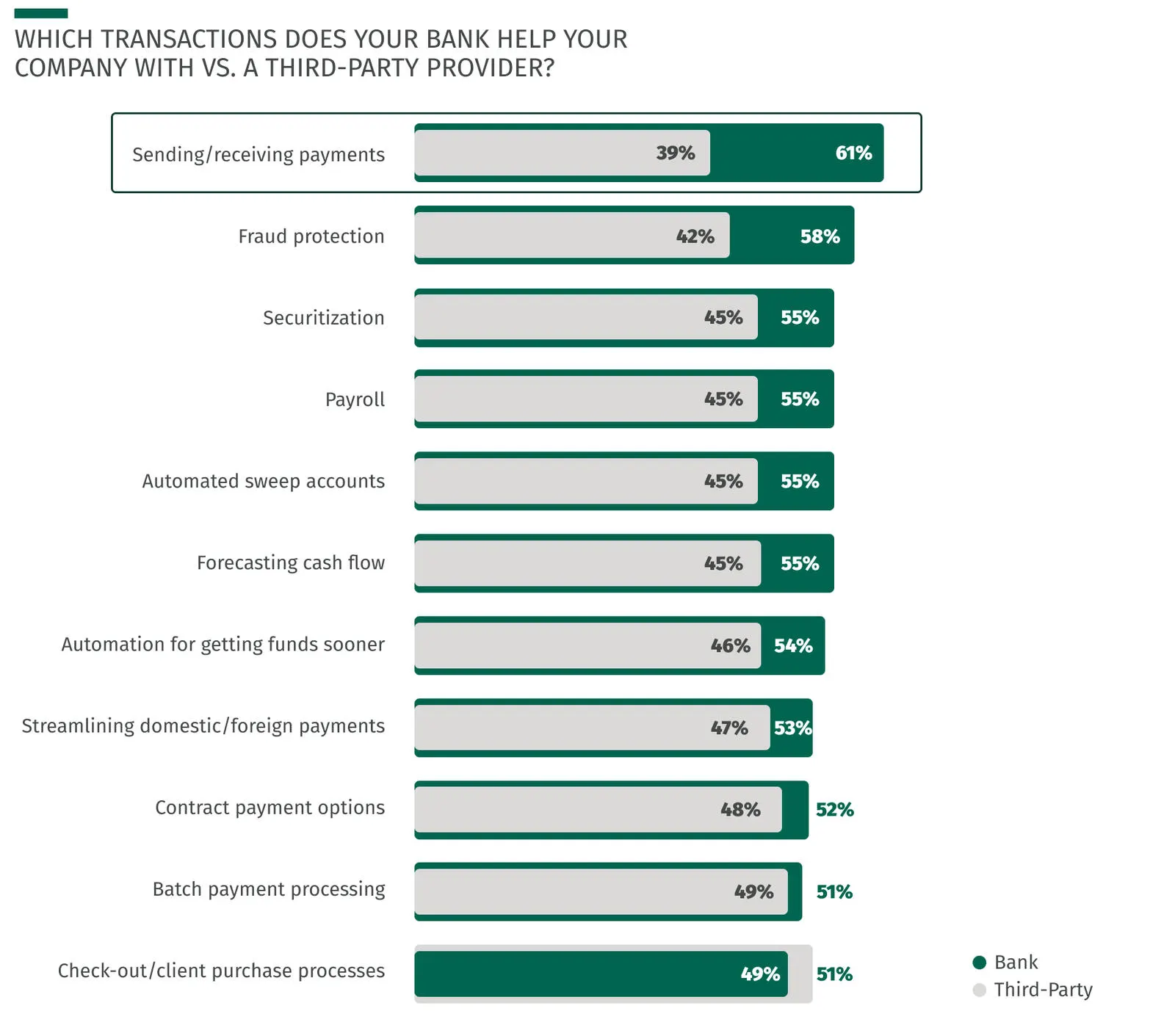

Midsize Companies Rely On Banks For Most Payment Services, Including Sending and Receiving Payments

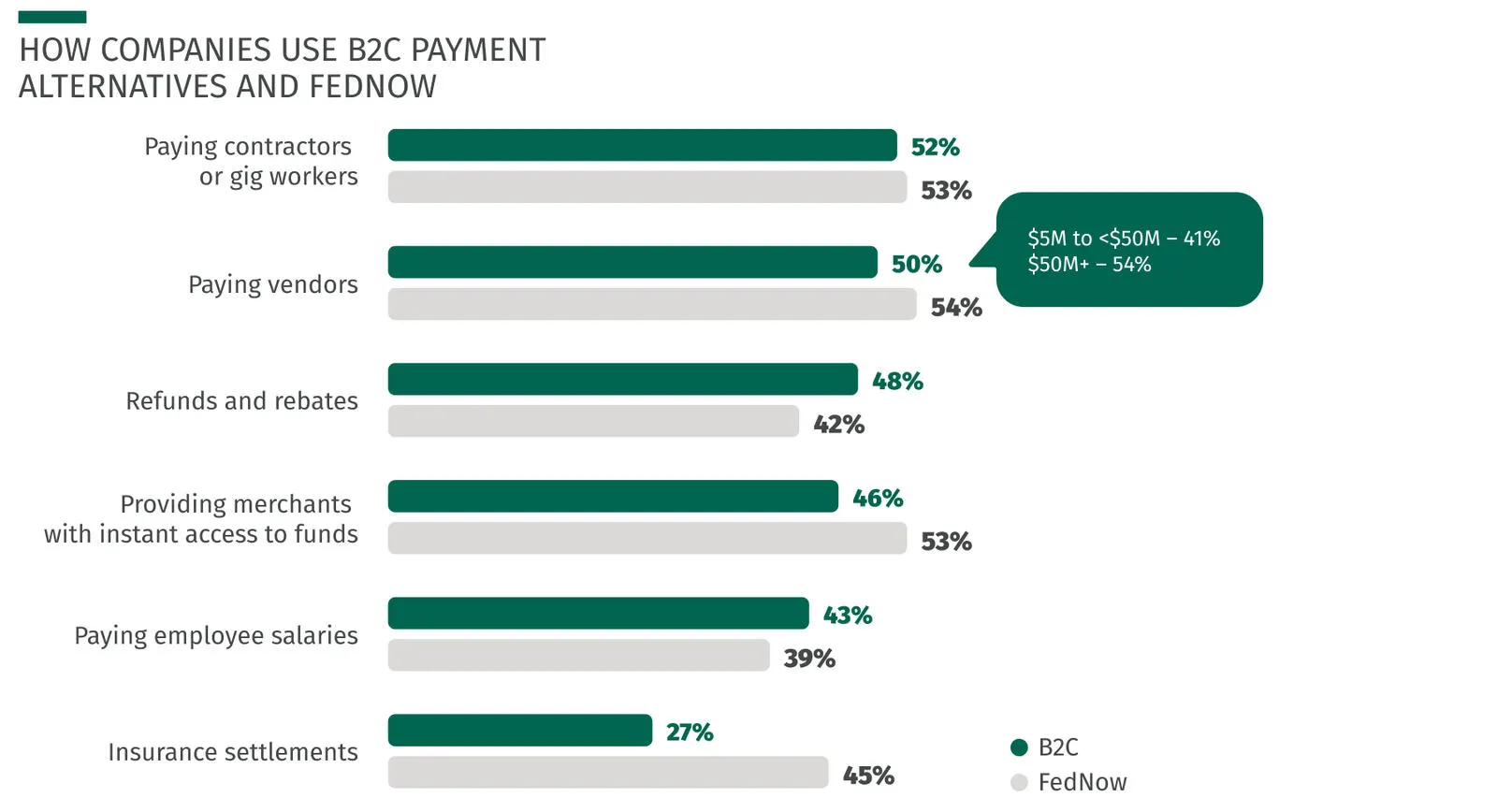

Midsize companies that employ FedNow instant payments or partner with third party business-to-consumer (B2C) payment alternatives like Venmo, PayPal and Cash App use these options primarily to pay contractors and vendors. These trends remained roughly flat from 2025.

Yet companies continue to rely on their bank for most services, except for point-of-sale (POS) checkout and client purchase processes.

The largest divergence is in sending and receiving payments, where 61% of midsize companies say they use a bank for sending or receiving payments compared with 39% that use a third party.

-

"When it comes to paying contractors and vendors, it's becoming increasingly important for small businesses to offer choice. While many service providers still prefer to be paid by check, a growing number — especially among the gig worker community — accept electronic payments via ACH, real-time payments, and B2C rails like Zelle®. Such methods offer organizations greater speed, flexibility and auditability. Banks can serve as the central hub for a comprehensive payment ecosystem, enabling companies to integrate payment choice into their current workflows."

Mark Valentino

EVP, Head of Business Banking

Majority Of Midsize Companies Use Bank APIs To Embed Payments Into Their ERP

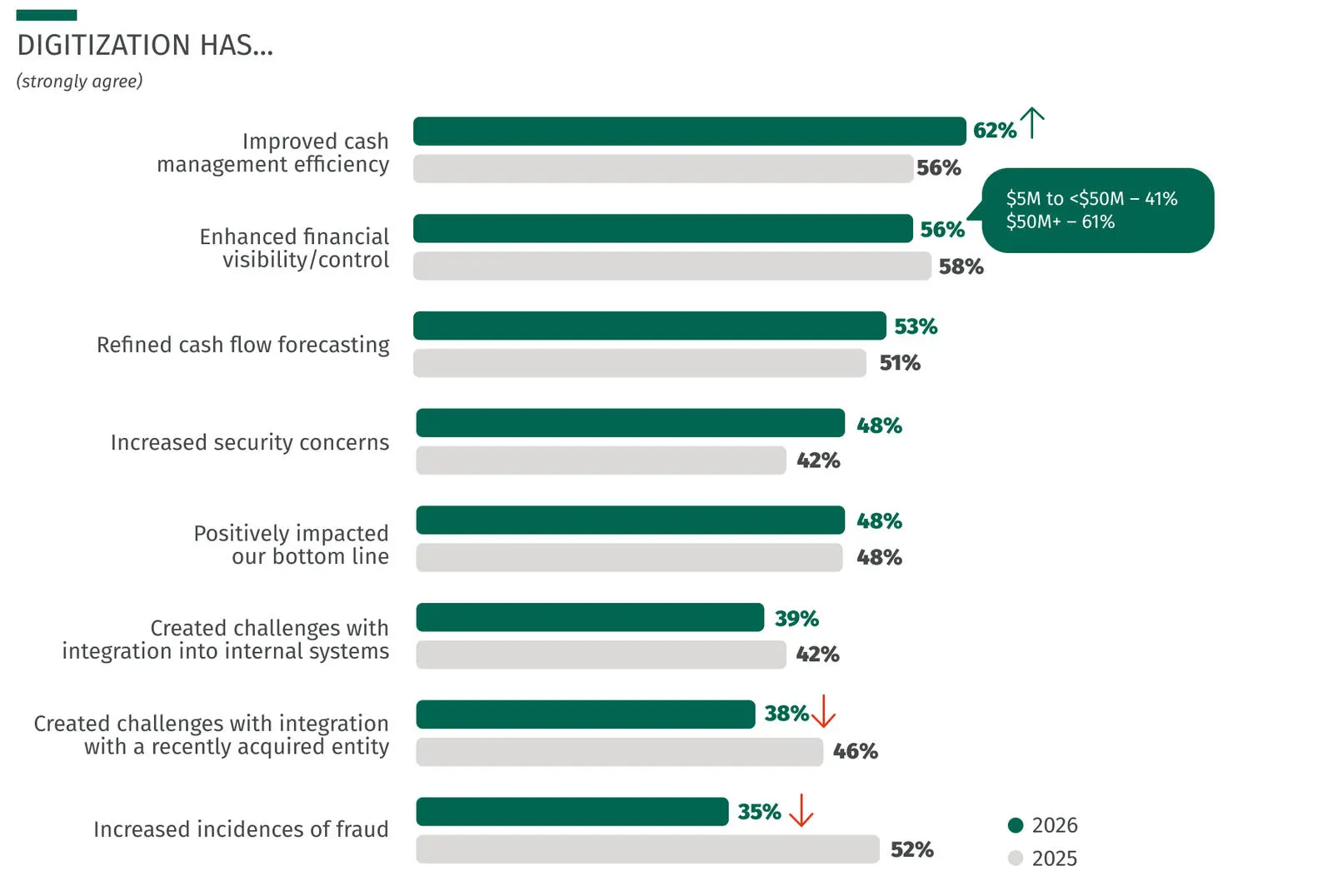

When asked about how the transition from paper-dominated processes is impacting the treasury function, more than half of respondents strongly agree that digitization has improved cash management efficiency, enhanced visibility/control and refined cashflow forecasting. The biggest mover from 2025 is "improved cash management efficiency," which rose six points to 62%. Meanwhile, larger companies (those with revenues of $50M to $1B) have recognized greater levels of improvement in financial visibility and control than smaller companies (those with revenues of $5M to $50M).

Seventy-six percent of respondents are using APIs from their financial institution to embed payment processes into their enterprise resource planning (ERP) system. Among those currently using embedded finance, 80% are partnering with banks to advance such processes into their existing platform, as compared with just 68% that are partnering with FinTechs. Only 3% of respondents are building embedded finance processes internally.

When asked about digital enablement pain points, a growing percentage of respondents cite security concerns, contrasting with a declining share that say digitization has created integration challenges or increased incidences of fraud.

-

"Embedded finance is rapidly becoming table stakes in the treasury function. Midsize companies are largely choosing to work with the financial institutions they already know and trust to integrate these technologies into their existing ERP processes."

Eric McCabe

SVP, Head of Embedded Finance

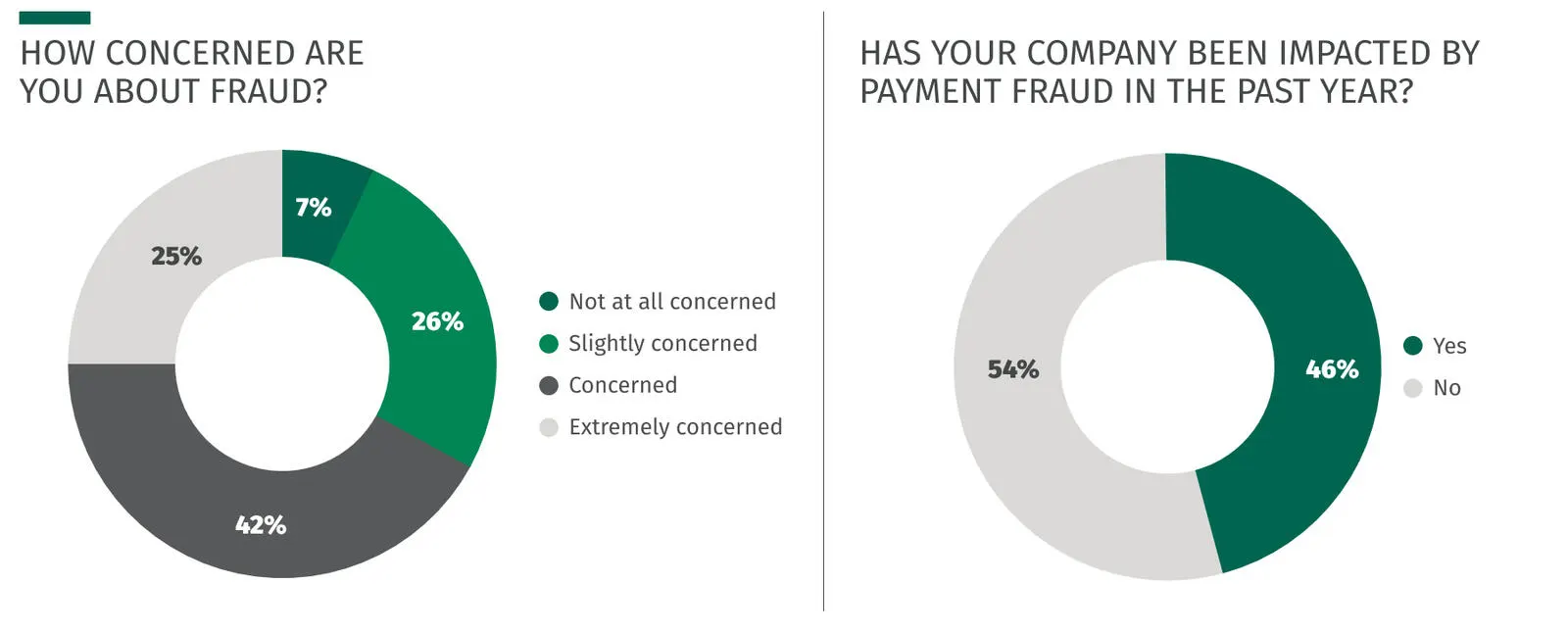

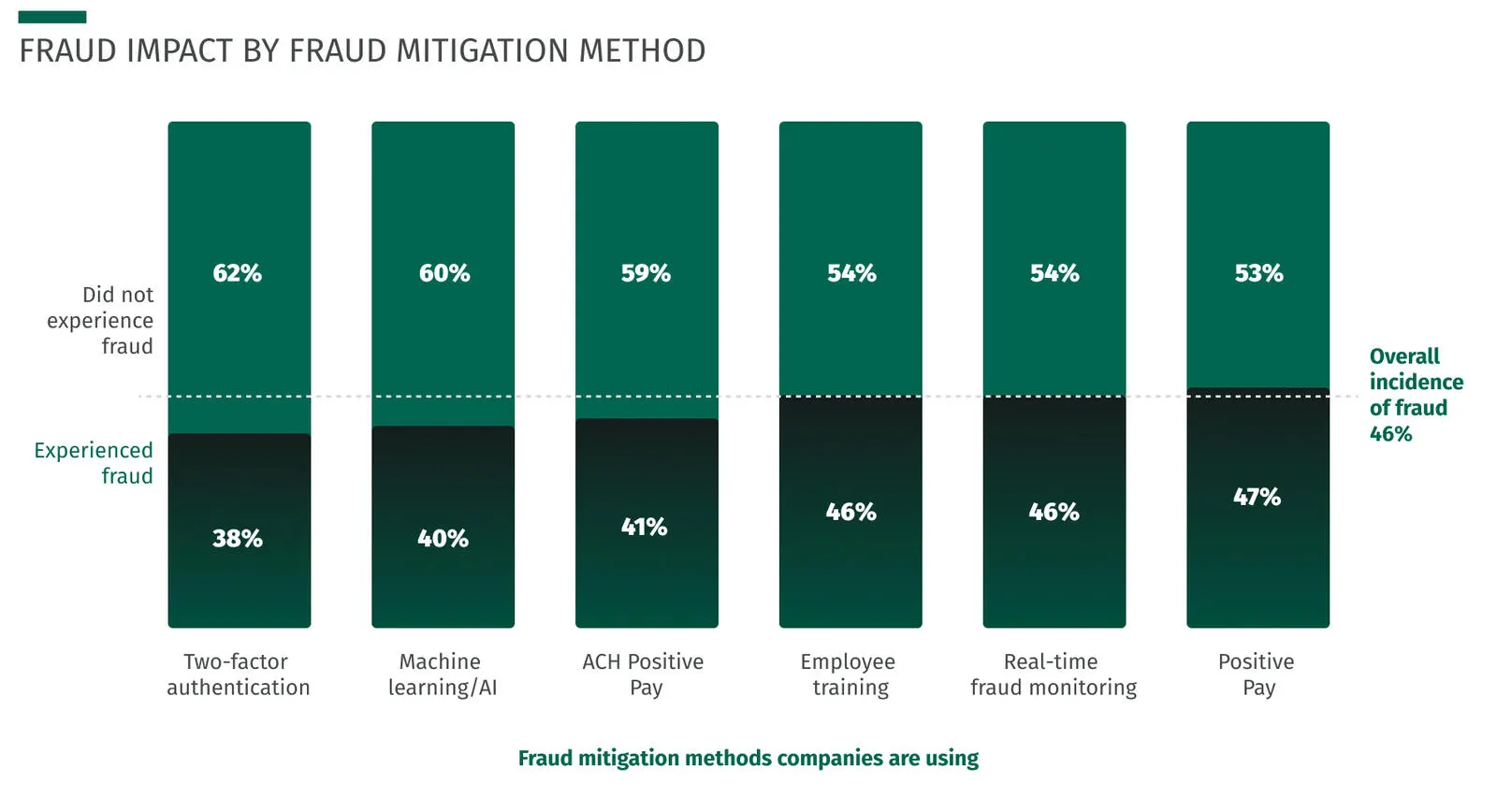

Fraud Concerns Remain High, But Use of AI Offers Relief

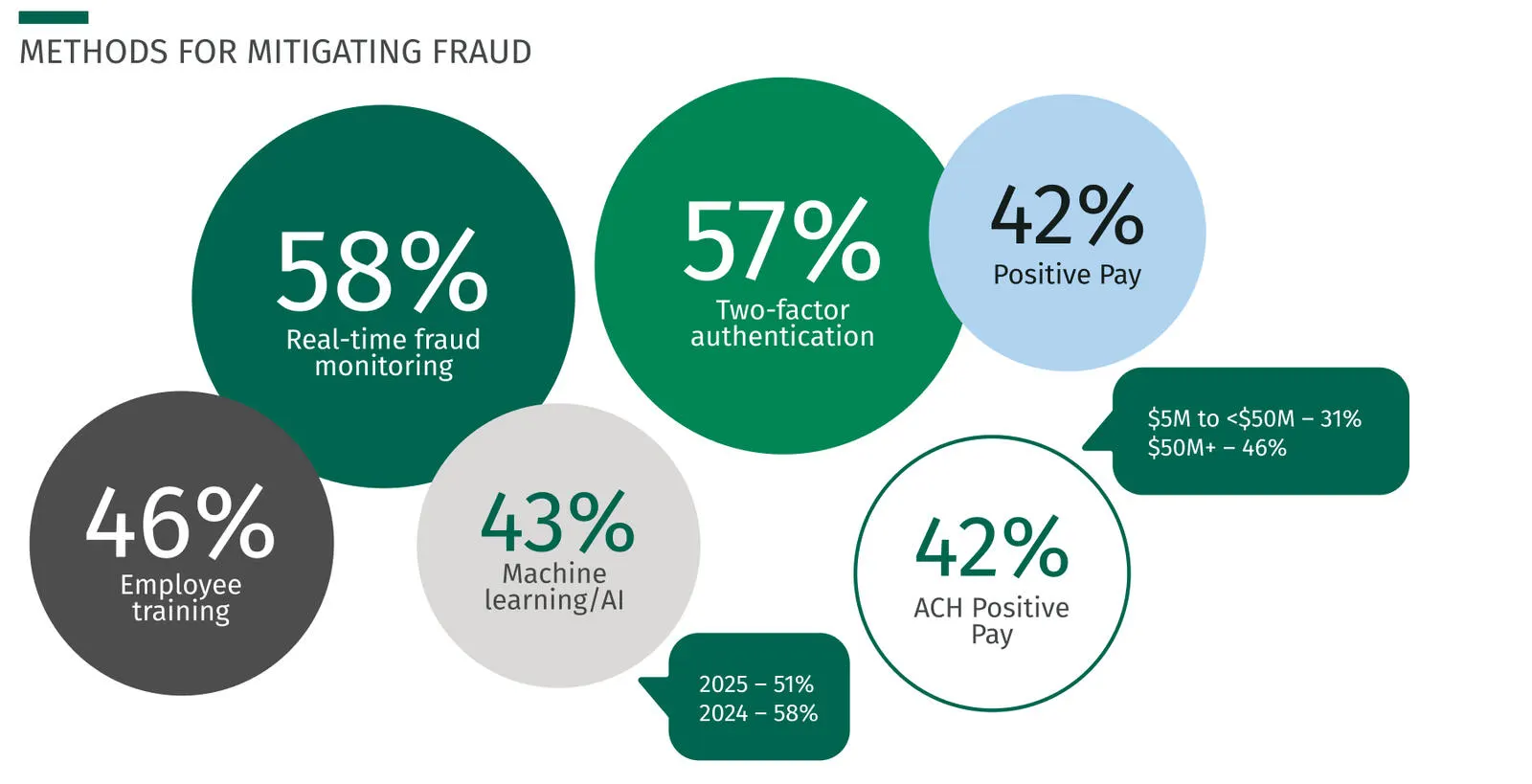

Sixty-seven percent of respondents remain concerned about fraud and 46% say they have been impacted by fraud in the past year. Real-time fraud monitoring and two-factor authentication are the most widely used fraud mitigation methods in 2026.

Use of ML/AI Declines Year Over Year

Interestingly, the proportion of respondents saying they use machine learning or AI for fraud mitigation has trended downward in each of the past three surveys. The percentage declined from 58% in 2024, to 51% in 2025, to just 43% in this year's survey.

Despite this trend, there is evidence that the use of machine learning or AI (as well as two-factor authentication) is correlated with a lower incidence of fraud. Of the companies surveyed that use machine learning and AI technologies in fraud mitigation, just 40% stated they were impacted by payment fraud in the past year, well below the 46% of the total survey population that experienced fraud.

What explains this counterintuitive decline in the use of cognitive technologies for fraud mitigation? It may be a matter of perception.

-

"The apparent decline in reported use of AI and machine learning for fraud mitigation may be misleading, as modern real-time monitoring relies heavily on these technologies. As midsize businesses increasingly outsource fraud prevention, they have less visibility into how these tools work, leading to underrecognition of their impact."

Jen Martin

EVP, Head of Fraud

Recommended Actions For Treasury Leaders In 2026

- Survey vendors and contractors on payment preferences to identify opportunities to replace checks and reduce processing costs.

- Talk with your bank about offering instant payment options (e.g., RTP) to accelerate payments and improve supplier satisfaction.

- Audit third-party fraud providers to verify their use of AI and machine learning for real-time monitoring and detection.

- Work with your financial institution to understand the best payment solutions to meet your specific use cases. Make sure you understand any associated fraud risks and controls, and select the best, safest products for your needs.

- Accelerate treasury digitization by leveraging your bank as a cash management hub to gain real-time visibility and tighter financial control.

Explanation Of Methodology

Citizens worked with research firm Escalent to survey more than 300 financial decision-makers at midsize companies on their attitudes and motivations around the use of various payments and receivables methodologies, using both banking and credit rails. Participations were also surveyed on their attitudes toward the adoption of social token functionality in the B2C space.

- All participants were C-level executives and/or the heads of treasury or accounting functions.

- All participants worked in industries other than banking at the time of the survey.

- 208 participants were financial leaders at midsize companies with annual revenues between $50 million and $1 billion. 99 respondents worked at companies with annual revenues of between $5 million and $50 million.

- Internet-based surveys were conducted with Escalent between March 24 and April 2, 2026.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE