How to Sell Your Business in a Challenging Market

By Ivan Hsu, Director, Trinity Capital, a division of Citizens Capital Markets

Download a print-friendly version of this article.

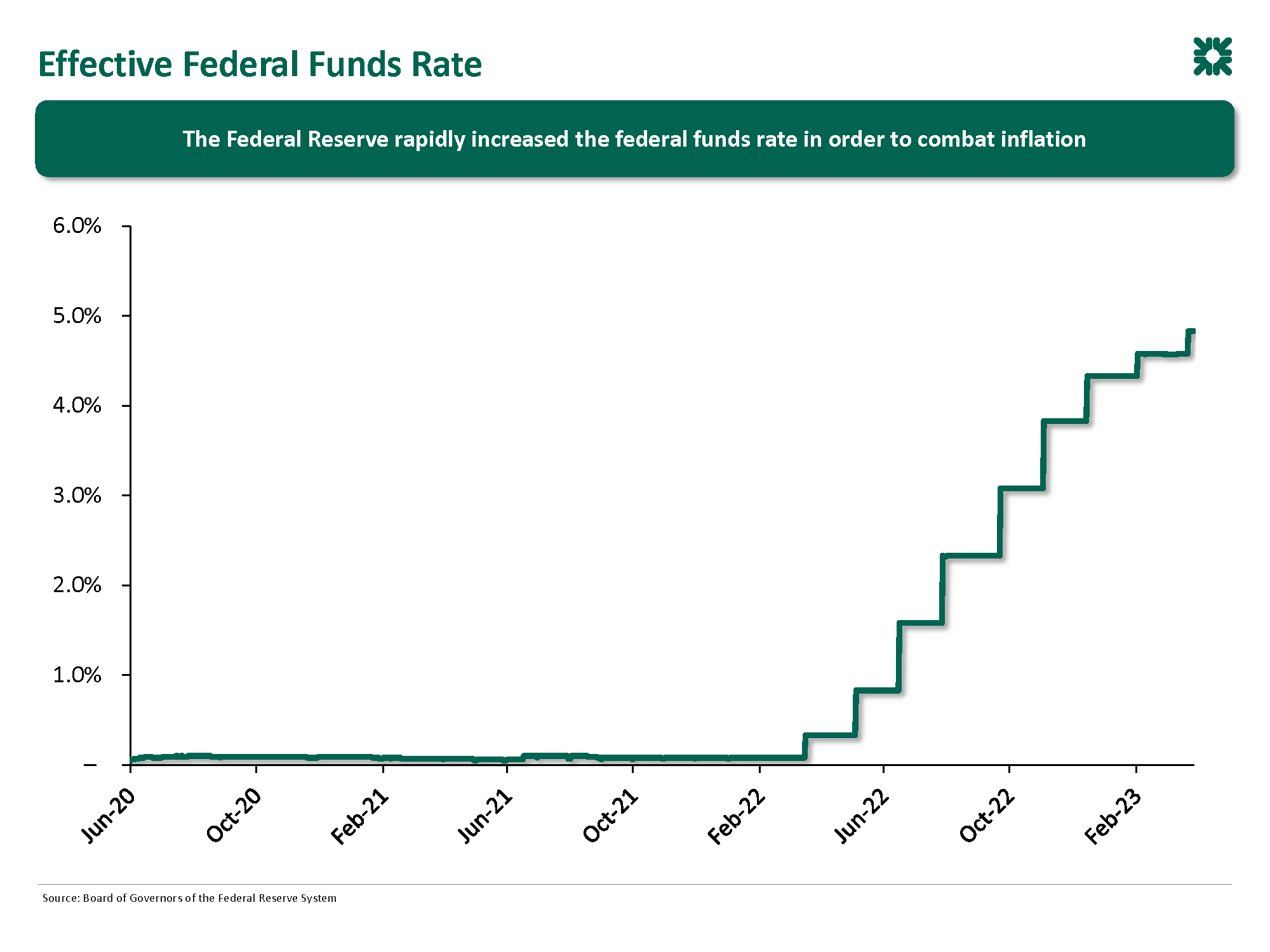

The Federal Reserve’s (Fed) effort to curb inflation through aggressive rate hikes has dominated business headlines over the last year. The effective federal funds rate has jumped from nearly zero in March 2022 to almost 5% today.

- Many franchise owners are now re-evaluating their options for selling and moving on to their next venture.

- Valuations are only one factor in the sales process. There are dozens of deal terms, some arguably more important than valuation in certain cases, which could make or break a deal.

- Considerations like seller financing, earn-outs, non-exclusive negotiations, and minority investments might be employed sparingly under normal market conditions but are anticipated to see greater use as capital markets remain choppy.

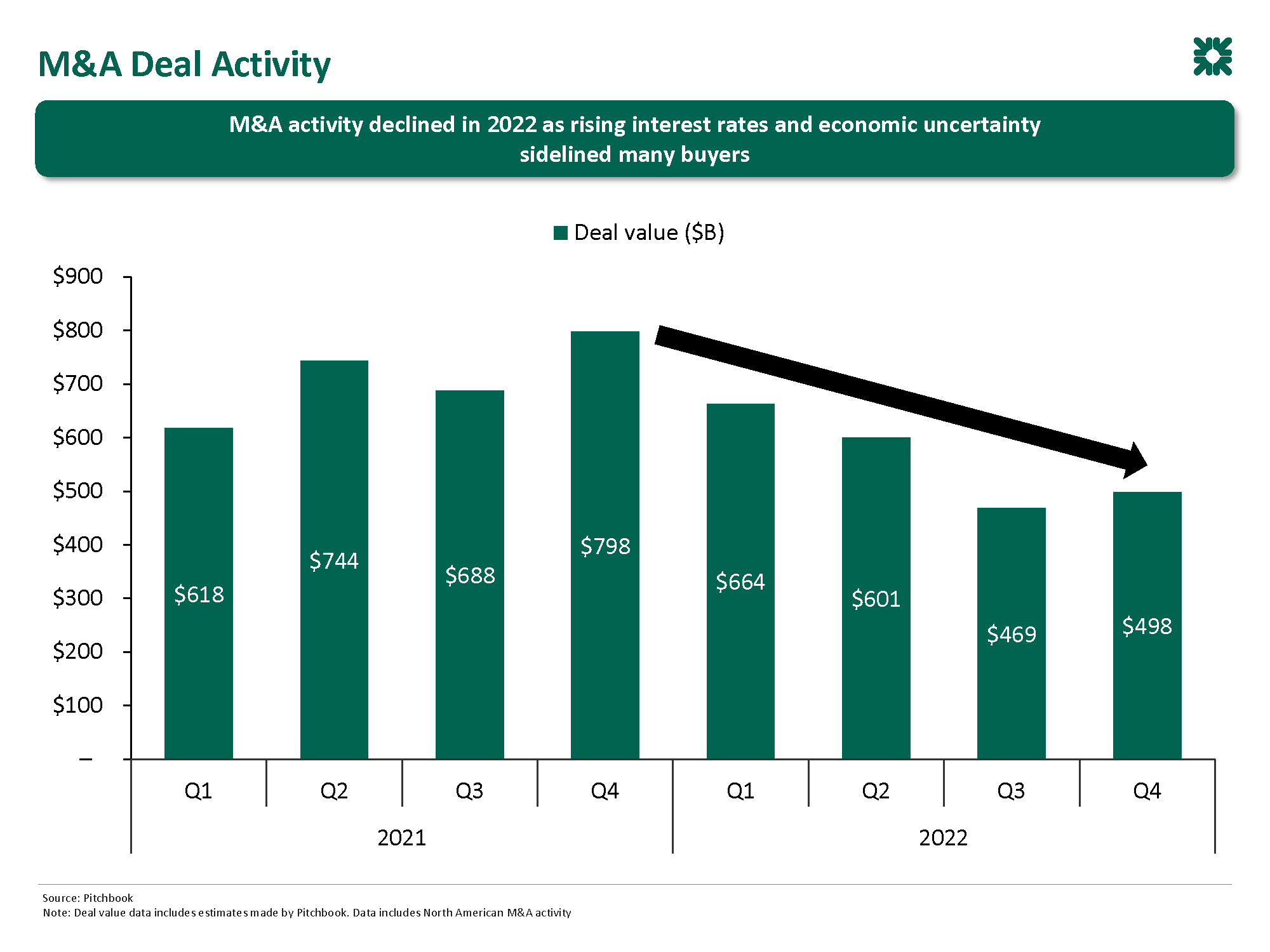

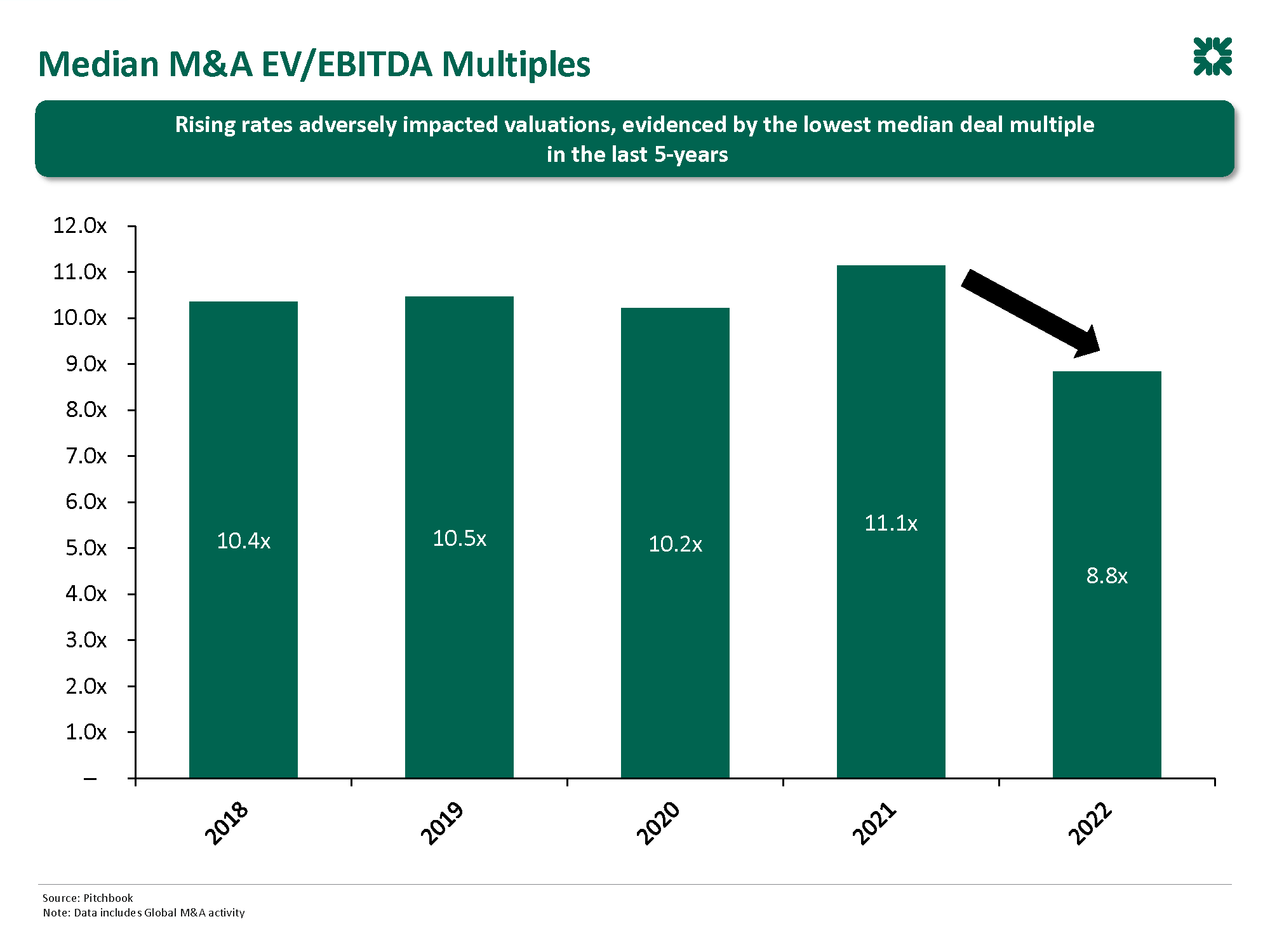

The impact of these rate hikes on the M&A market has been notable. The volume and value of M&A transactions in 2022 were both lower than the previous year. North American M&A transaction value declined by 21.6% year-over-year. Valuations and EBITDA multiples1 are down as well. The median transaction multiple in 2022 declined to 8.8x after reaching a 14-year high of 11.1x in 2021. However, this was to be expected. With interest costs nearly tripling in some cases, the ability of buyers to pay inflated multiples has naturally come down.

As a result, many franchise owners are now re-evaluating their options of selling and moving on to their next venture. While there is no silver bullet, here are a few ideas to help navigate a challenging market. No matter which strategy is chosen, owners should confer with experts throughout the process to ensure that the solutions employed align with their goals.

Get creative

There is a common misconception that valuation is the only significant variable involved in getting a deal done. This notion is perhaps propagated by the popular TV show “Shark Tank.” Shark – “I’ll offer to buy 40% at a $1 million valuation.” Unsuspecting entrepreneur – “Done!”

Valuations are only one factor in the sales process. There are dozens of deal terms, some arguably more important than valuation in certain cases, which could make or break a deal. Here are terms or considerations that might be employed sparingly under normal market conditions to bridge differences between buyers and sellers, but ones now anticipated to see greater use as capital markets remain choppy.

Seller financing

As the name suggests, this allows the seller to play the role of lender and fill any financing gaps. Post-transaction, the seller is owed a seller note that is typically repaid over five to seven years. This seller note might contain limitations in terms of principal amortization, but it usually commands a market-based yield.

Earn-out

An earn-out allows the seller to earn more proceeds after the transaction closes and is usually used to bridge any valuation gaps. Earn-outs are often tied to certain future performance metrics (e.g., revenue, EBITDA) and are typically structured for one or two years after a transaction closes. The key with earn-outs is to tightly define the performance metric so there are no ambiguities. It is also wise to structure the earn-out on a sliding scale instead of binary (i.e., all or nothing).

Non-exclusive negotiations

In a sale process, a seller usually requests interested parties submit a letter of intent (LOI) and provide a buyer time for diligence and perhaps access to the management team. If the seller owns a desirable business, they may receive several LOIs from various parties. The seller usually negotiates the best LOI, picks a buyer, then enters exclusive negotiations with that buyer. During the exclusivity period, the seller is not permitted to speak with other prospective buyers. Some or all of the LOIs may contain financing contingencies.

One strategy to reduce risk of deal failure is to enter non-exclusive negotiations with more than one interested party, and whoever gets to the finish line first, is awarded the deal. There are several important considerations when pursuing this strategy, and messaging to the various buyers is crucial as they want to avoid resource commitment toward due diligence without exclusivity. M&A advisors can help sellers and buyers navigate this path.

Minority investments

Sellers should consider the pros and cons of taking on a minority partner and evaluate how this might fit with their overall goals. The biggest advantage of a minority deal is that it generally would not necessitate refinancing cheaper existing debt for more expensive new debt, which would very likely be the case in a majority recapitalization. A minority investment may require the sale of a smaller stake at a less favorable valuation today, but it buys time to sell a larger stake in the future when conditions normalize.

Understand what your business is worth today and why

In the franchise business, many sellers already have a number in mind when they think about selling their business, but often these figures are not based on market conditions today. Instead, these figures could be based on a franchise transaction from last year or one they read about in the press. Unfortunately, in a rapidly rising interest rate environment, it is unwise to get anchored to valuations from even a couple of months ago and to assume those numbers are still valid today.

While sellers need not master the detailed mechanics of valuation analysis, it is important to understand the valuation drivers for their business. For a restaurant franchise, for example, the segment (QSR, fast casual, full service), the geography (urban vs. rural, state specific), the quality of the brick & mortar units, lease tenure, the management team qualifications and, of course, the financing market can all cause valuations to differ widely from one business to another. Without the appropriate diligence, it can sometimes be difficult to understand what might cause one business to be valued differently from another seemingly very similar one.

Deep valuation analysis, industry expertise and negotiating transaction deal points are core skills of investment banking advisors. Advisors can help determine the key drivers of business valuation, so that owners can maximize the overall transaction value when it is time to sell. Additionally, advisors can help owners evaluate complex structuring options to best meet their goals and negotiate favorable deal points for other considerations such as non-compete clauses, limiting indemnification liabilities and representation and warranty covenants that often play important roles in transactions.

Considerations

While the environment for M&A is expected to remain challenging for the foreseeable future, deals are still getting executed. Private equity firms have a record amount of dry powder capital that needs to be deployed2. Additionally, corporate cash piles remain materially above pre-pandemic levels3. While it is unclear if the high valuations of the past few years will return, there is still demand to ensure goals are achieved. Greater deal-making creativity and a better understanding of the market are keys to achieving the best outcome for franchise owners.

Ivan Hsu is a Director at Trinity Capital, a division of Citizens Capital Markets with more than 15 years of extensive experience as an investment banking veteran executing transactions involving mergers and acquisitions and private debt placements in the consumer/retail space, with a keen focus on health and wellness and active lifestyle.

Related Reading

Small Restaurant Franchisees are at a Crossroads

Franchisees with one or just a handful of franchise restaurants face the decision of whether to grow their businesses or exit the industry.

M&A Deal Making Dynamics

The universe of potential buyers of middle market companies has grown as more private equity firms enter the market.

Family-Owned Business Succession Planning

By taking steps to evaluate your business and prepare it for a transition, you can maximize value and bolster the company’s position.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

1As a refresher, earnings before interest, taxes, depreciation and amortization (“EBITDA”) is a proxy for a business’ cash flows and businesses often trade on a multiple of EBITDA

2Source: Bain & Company Global Private Equity Report 2023

3Source: U.S. Census Bureau, Quarterly Financial Report: U.S. Corporations: All Information: Cash and Demand Deposits in the U.S.

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE