5 Trends to Watch in 2023 Middle-Market M&A

By Jason Wallace, Head of M&A Advisory, Citizens Capital Markets

Download a print-friendly version of this article.

- Even with macroeconomic headwinds, M&A valuation expectations are upbeat, and middle-market businesses expect company performance in-line with 2022

- Though still very positive, fewer buyers and sellers are confident in completing deals

- The pipelines of buyers and sellers continue to recover toward pre-pandemic levels

- Interest in growth through M&A is high, but interest in international opportunities is down

- Half of buyers say that financing markets are still supportive for M&A plans

In the 2023 M&A outlook, a survey of 400 U.S. businesses and private equity (PE) firms, respondents expect mostly positive trends in M&A in 2023, despite the uncertainties of the macro environment. Now in its 12th year, the survey covers U.S. middle-market businesses with revenues of $50 million to $1 billion as well as PE firms who are active in the acquisition and sale of U.S.-based companies in the same revenue range.

This year, we found that companies had a more optimistic view of their own prospects than news headlines would suggest. There were also signs that the M&A environment will return to more normalized expectations and volume levels, after the highs and lows of the pandemic. Here are five key trends to watch this year.

Read the full 2023 M&A Outlook Report here.

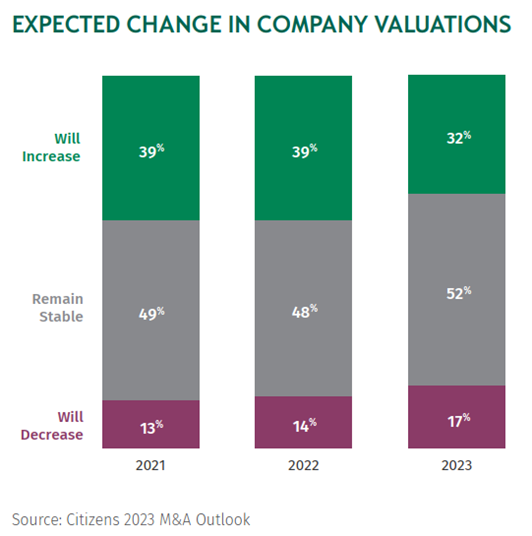

1 - Valuation expectations are upbeat, alongside solid company-performance outlooks

Compared to recent years, companies and PE firms both give a slightly moderated view of valuations. Most believe valuations will stay stable or increase, while only 17% believe valuations will decrease. While expectations vary, nearly all sectors had an upbeat outlook with respondents only indicating a more negative valuation view of Transportation and Logistics.

According to Pitchbook, M&A deal multiples held steady around a median 2x revenue in 2022, even as public company multiples fell from 3.3x in 2021 to 2.3x in late 2022. It could be that the market sees a floor for deal values – especially in light of solid company performance. In the M&A outlook study, a fifth of managers say they expect the U.S. economy to worsen in 2023, yet 91% say they expect their company performance to be the same or better than last year.

Indeed, middle-market businesses have navigated the inflationary era well. Eighty-four percent say they were able to pass some or most of their price increases on to customers, and the majority believe they’ll be able to maintain those dynamics through 2023.

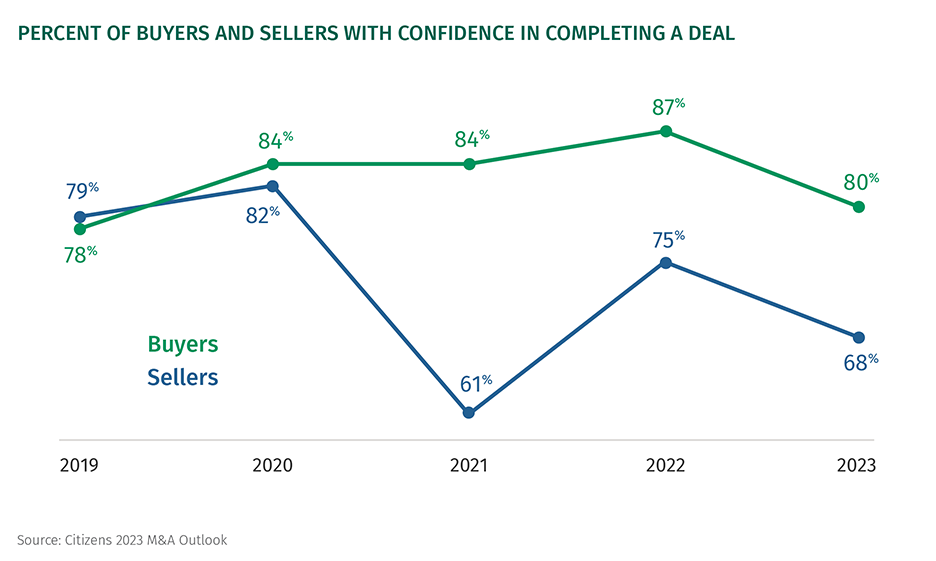

2 - Both buyers & sellers show a dip in confidence

While confidence in company performance is solid, we saw uneasiness around the M&A backdrop appear in other answers – such as the declining confidence about getting a deal done.

Seller confidence remains notably below pre-pandemic levels, even though companies and PE firms both say the market environment favors sellers somewhat. Would-be sellers may be nervous about public stock values or negative headlines around stricter financing conditions and debt-syndication issues from some 2022 mega deals.

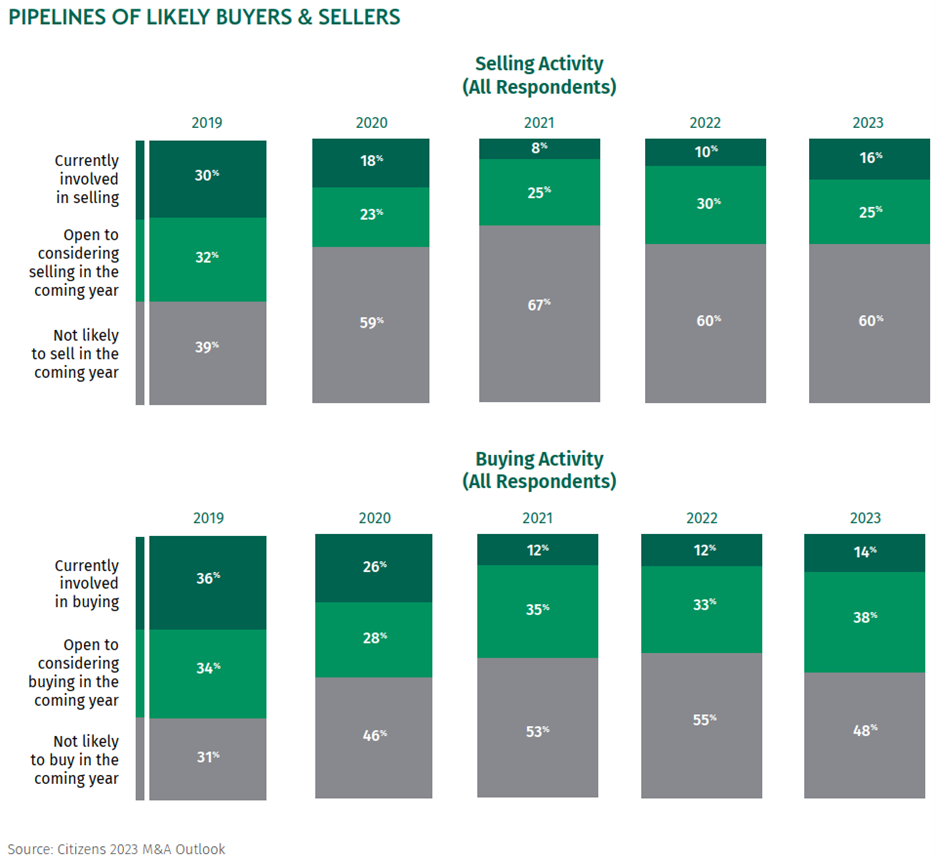

3 - Pipelines return to pre-pandemic norms

Forty percent of middle-market businesses say they are currently involved in selling activity or open to it in 2023, identical to last year and in-line with the pre-pandemic 2020 outlook. The buyer pipeline has also recovered to pre-pandemic levels with 53% of companies saying they are currently involved in buying activity or open to it.

PE firms expect reasonable deal flow in 2023. Thirty-four percent of PE firms say deal flow will increase and 44% believe it will stay the same as in 2022, while 22% say it will decrease. These figures are down substantially from the 2022 Outlook, but they still indicate optimism. Deal volumes in 2022 returned to a pre-pandemic trendline, according to BCG, and 2023 could hold more of the same

Among PE firms who believe there will be higher deal flow in 2023, 52% believe it will be driven by an increase in private equity assets coming to market. Thirty-six percent say that interest rates will be lower, prompting more transactions.

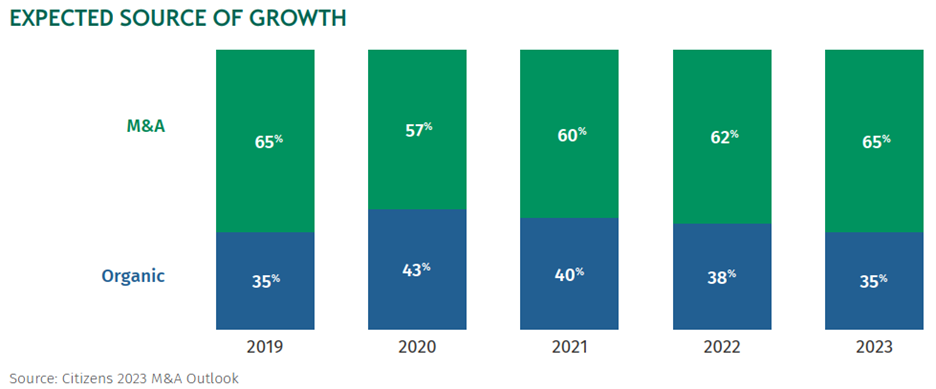

4 - Interest in growth via M&A remains high; interest in international opportunities is down

The hunt for growth continues to be a major factor for M&A activity. With markets showing signs of contraction and misaligned short- and long-term interest rates, middle-market companies and PE firms continue to prioritize and value growth.

Two-thirds of companies say the majority of their growth in 2023 will come from M&A while only a third point to organic growth. Among buyers, the hunt for growth is by far the biggest motivation for coming to market, cited by 62% of respondents. Sellers also cite strategic growth as a top reason for coming to market, though the most popular selling motivation is “lack of a succession plan” – businesses that need new leadership and a monetizing event to transition a founder out.

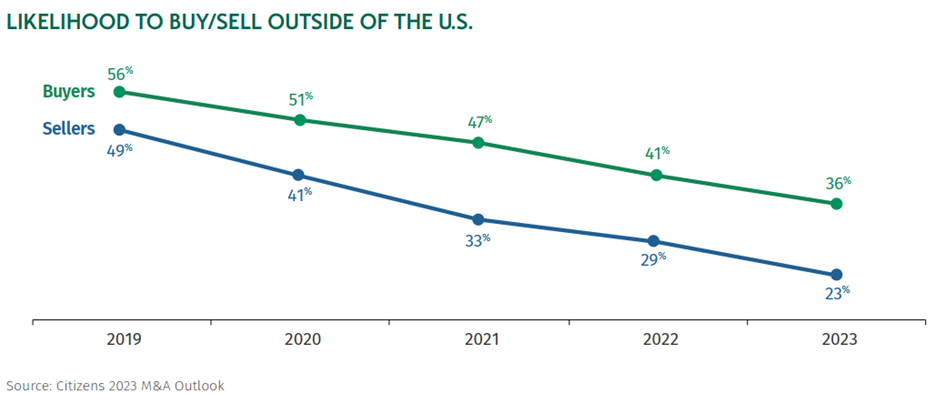

While interest in growth is up, interest in international transactions is down amid geopolitical tensions and global economic headwinds. Only 36% of buyers say they are interested in an international acquisition, down for the fourth consecutive year from a peak of 56% in the 2019 Outlook. Twenty-three percent of sellers are interested in an international buyer, also at a five-year low. Even PE firms showed lower interest in international opportunities, down to 37% from 55% the year before.

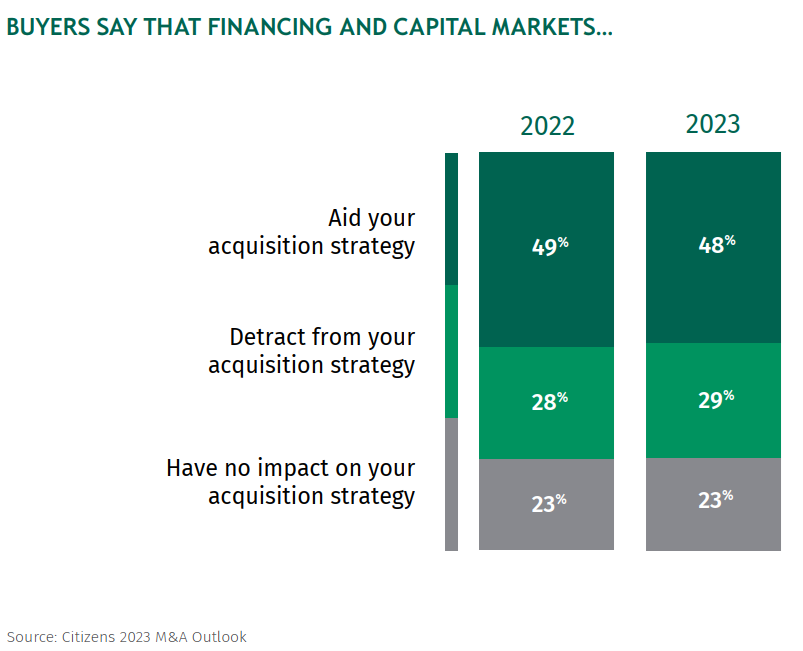

5 - Some buyers say that current interest rates can help them

Buyers and sellers say rising interest rates makes them hesitate to pursue M&A. However, that view is not universal. In fact, nearly half of buyers say that current financing and capital markets can aid their acquisition strategies in 2023.

Indeed, many respondents say that current capital markets conditions make it more likely they’ll acquire another company. While interest rates moved quickly off record lows, it could be that many buyers still see current interest rates at historically appealing levels. However, buyers do acknowledge that higher rates take a bite out of prospective returns.

Looking toward a more "typical" deal environment

The steep inflation of 2022 and rapid climb in interest rates were anything but typical, capping a pandemic era marked by shifting macroeconomic conditions. Middle-market companies have piloted their businesses through these changes and, in many cases, emerged leaner and better equipped to compete.

In the 2023 Outlook, companies and PE firms gave the first real signals that deal activity could be settling into a more typical, post-pandemic normal. Buyer and seller pipelines have fully recovered. Deal flow expectations are solid and valuation outlooks are moderated but healthy. Underlying these trends is the fundamental point that companies feel positive about their own performance outlooks.

While there was more focus in 2021 and 2022 on capturing high valuations, the themes of this year’s survey were more evergreen – such as the PE firms who said deal flow will come from private equity assets coming to market, and the sellers who said they’re in the market because they lack a succession plan.

Still, there are signs that uncertainty lingers among companies and PE firms. Deal confidence levels are down and the middle market is significantly more focused on domestic transactions compared to recent years. In the 2022 Outlook, many buyers and sellers said they looked to an M&A advisor to help them speed up the deal process. But this year, as they cope with ambiguity about shorter-term conditions, both buyers and sellers are more likely to say they look to their M&A advisor to be “an expert sounding board.” More buyers and sellers also indicate that they want an M&A advisor to help them get the best price, another sign that they are looking to advisors to lock-in price certainty and for clarity about the environment.

Key Takeaways:

If your company is considering M&A in 2023, keep these trends in mind:

- Prepare for the possibility of stable or higher valuations. Though some macro signals look recessionary, individual companies continue to forecast solid performance. Across buyers, sellers and PE firms, valuation outlooks are stable or higher.

- Be ready for a competitive deal environment when the macro backdrop stabilizes. The slower deal flow of late 2022 could reverse quickly if macroeconomic trends stabilize.

- Know what’s in demand this year. Growth through M&A continues to be a top motivation for buyers. Companies looking to sell should keep that dynamic top of mind as they take steps to prepare their businesses for a transaction.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales, and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS. (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE