By Nate Hesch | Associate | Willamette Management Associates, a Citizens company

- Despite the popularity of sustainable investments, incorporating environmental, social and governance (ESG) criteria into equity valuations is still new and relatively undefined.

- Rating systems can help identify what counts as an ESG investment by giving companies scores on each of the three categories (i.e., E, S and G).

- Analysts can build ESG factors into valuations across areas like cost of capital, risk premiums and risk tail dependence.

In the 1990s, investment assets involving environmental, social and governance (ESG) considerations were just starting to gain traction. Now, after decades of explosive growth, they hold substantial sway in the average portfolio.

Portfolios actively using ESG criteria held over $8 trillion of assets under management in 2022.1 Plus, about a third of the market now is in sustainable investments.2

As consumers and investors demand companies take positive action for climate change, natural resources and social justice, ESG affiliation will be even more critical for profitability, financing and shareholder value. Despite this field's prominence, however, the systems for calculating ESG equity valuations are a work in progress — but they're getting better.

ESG's value and benefits for shareholders

A McKinsey survey from 2020 found that most business leaders and investment professionals think ESG programs within a company can create both short- and long-term value for shareholders.3 These benefits include:

- Decreased reputational, political and regulatory risk

- Increased customer and employee loyalty

- Reduced risk of litigation

- Savings from lower energy and water usage

- Favorable loan interest terms

Considering these possible benefits, ESG factors should — theoretically — improve a company's financial and investment performance. For example, ESG programs have the potential to prevent environmental lawsuits and reduce the volatility of a company's cash flow and profitability. Essentially, responsible business practices can serve as downside risk insurance.

Challenges with classifying ESG investments

ESG factors affect a company's performance and valuation, but determining this exact impact is easier said than done.

One challenge companies might face is identifying what counts as an ESG investment. This is because the concept of what benefits society can be subjective. Consider, for example, nuclear power plants. They can be called a positive environmental investment because they generate carbon-free energy but also a negative due to their radioactive waste and long-term impact on local communities.

Many companies also have conflicting attributes that make their ESG value difficult to weigh. For example, a tobacco or weapons company might support employee safety and gender equality. But those internal policies may or may not be enough to create a net positive social impact for the company overall.

It's also harder to pin down ESG valuation since investor priorities evolve over time. In the 1990s, smog, ozone pollution and apartheid were clear ESG concerns. Today, our global society recognizes significantly more sets of contributors to manmade climate change and human injustices.

How ESG rating systems can help

To clarify the muddiness, several ESG rating systems have been developed. Some of the most popular include the MSCI ESG Score, Sustainalytics ESG Risk Ratings, and Moody's Vigeo Eiris dataset. These systems rate publicly traded companies across their ESG performance, offering a data-point basis in evaluations.

To value privately held companies, these rating systems' publicly available methods can be used to construct scores. However, it might be simpler to compare select key issues against those of a similar publicly traded company. For instance, a private soft-drink company's carbon footprint, water stress and product safety might be examined in comparison to Coca-Cola's.

Rating systems aren't perfect and are open to debate. A company that makes vegan products may never accept that a meat processing company counts as an ESG investment, even if it scores highly within the rating systems across categories that include animal welfare. Still, the rating systems can provide a consistent measure and starting point to base ESG performance benchmarks.

Views on measuring ESG vs. non-ESG performance

With a system to classify ESG versus non-ESG companies, the next step is determining how ESG impacts investment performance. Since most ESG ratings have only been around for a few decades, the data is still coming in. However, some recent studies have identified impactful ways ESG can matter for equity valuations.

Portfolio theory

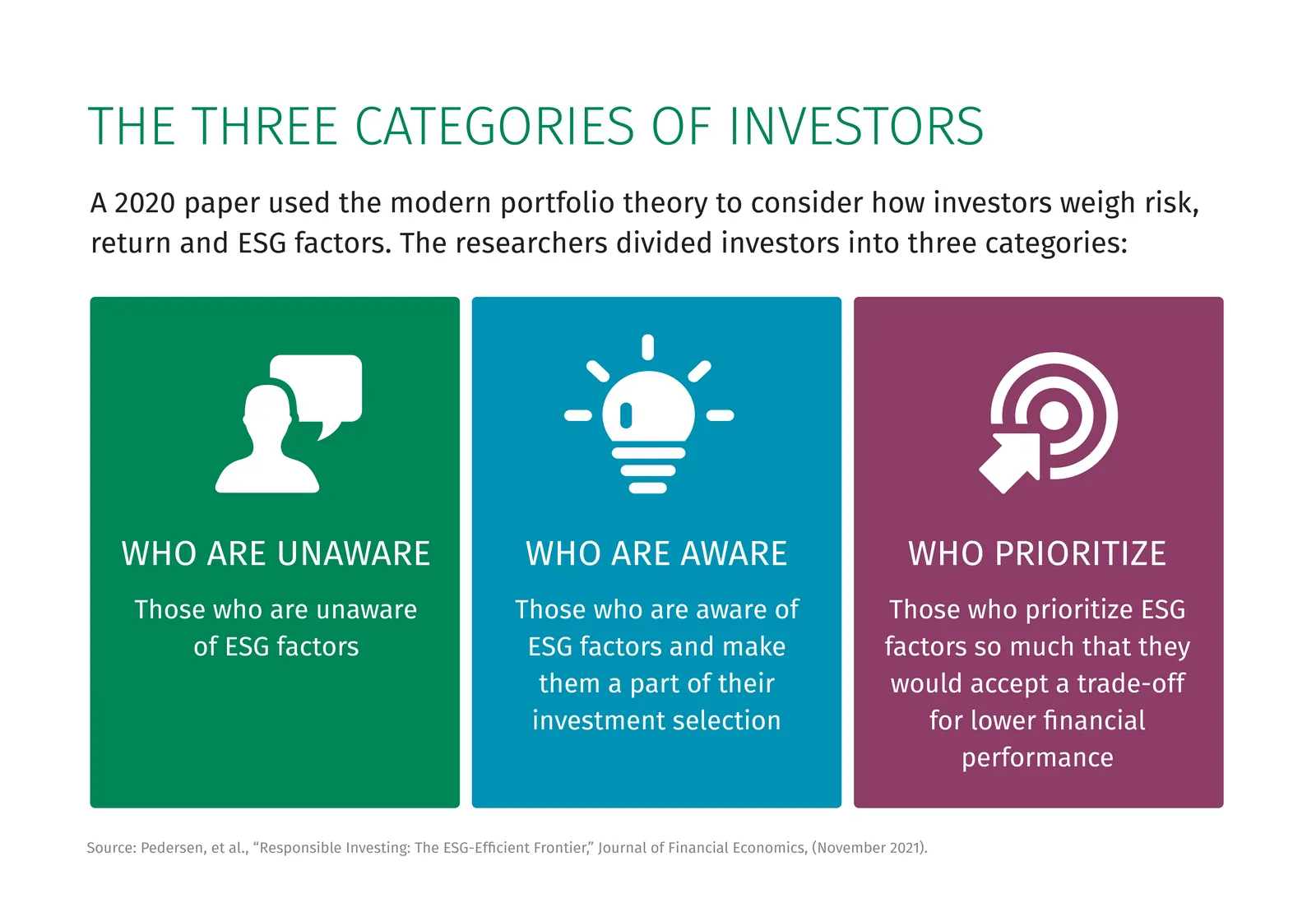

A 2020 paper used the modern portfolio theory (MPT) to consider how investors weigh risk, return and ESG factors.4 MPT is a method for selecting investments to maximize their overall returns within an acceptable level of risk. The mathematical framework employs building a portfolio of investments that maximize the amount of expected return for the collective level of risk. The researchers divided investors into three categories:

Given the size of the ESG market, the researchers predicted that a sizable share must be in the final category, meaning some investors are willing to pay a premium for quality ESG investments. These investor preferences should lead to higher demand and, through that, higher prices and lower required returns for ESG relative to non-ESG companies.

The ESG category of investments also made a difference based on empirical evidence. For example, higher scores for governance factors connected with higher returns on net operating assets while environmental and social factors did not.

Risk premiums

A 2018 study considered the correlation between the ESG related cost of capital risk premium compared to other established risk premiums, such as size risk, investment risk and market risk.5 The researchers found no correlation between ESG factors and other risk premiums, indicating that ESG factors can lead to a discount or premium on a company's cost of capital independent of these other variables. An ESG risk premium should be considered because ESG risk characteristics won't be represented within the other categories.

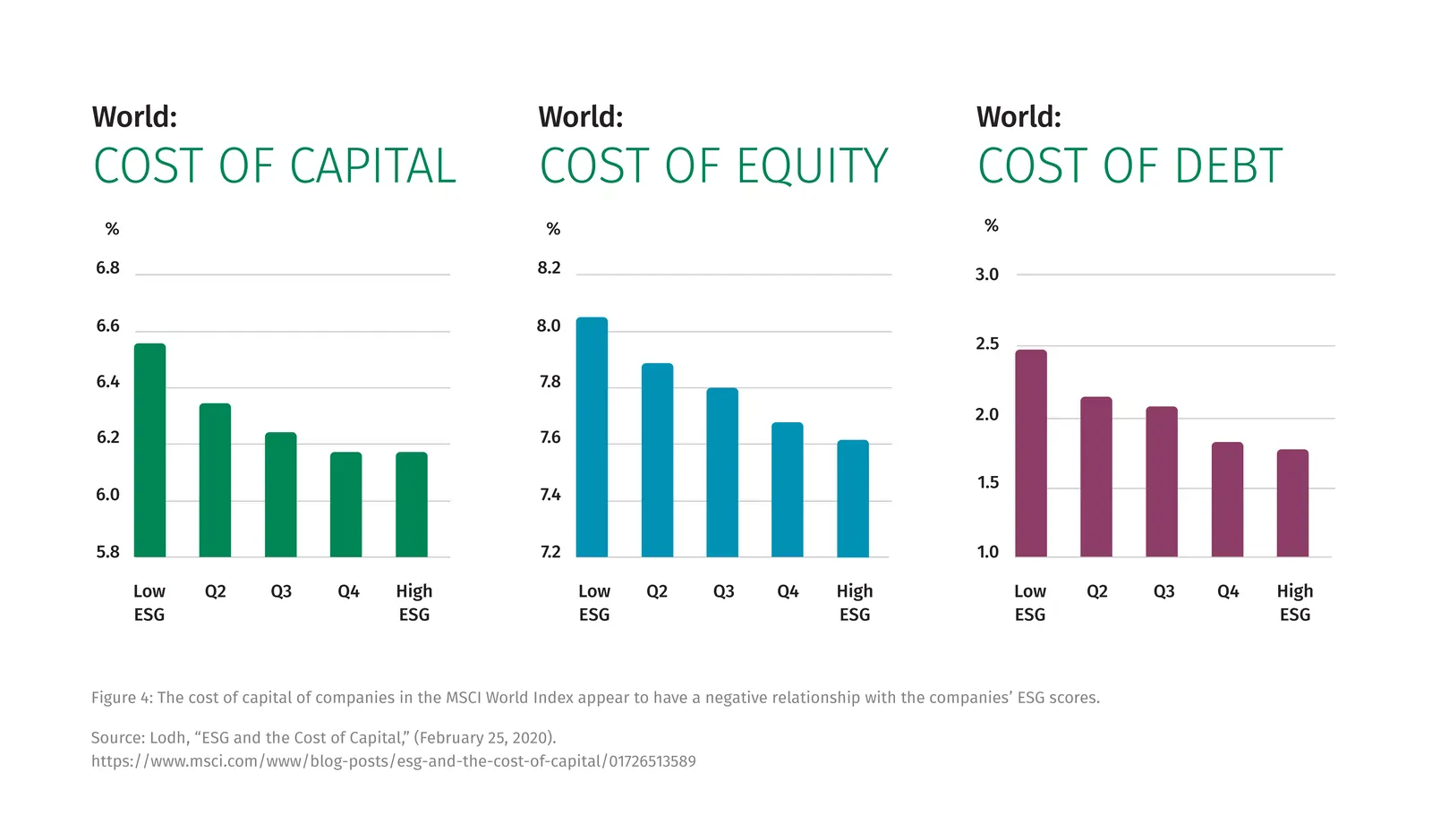

Cost of capital

In 2020, Ashish Lodh, an MSCI Research executive director with the equity solutions research team, studied the relationship between ESG factors and the cost of capital for companies and found a negative correlation consistent with the portfolio theory approach.6 Positive ESG factors lowered the cost of capital for equity and debt financing. Lodh also found variations in the ESG cost of capital between different international regions.

Risk and tail dependence

The final study, a white paper from 2021, compared ESG performance versus ESG risk scenarios. The authors tracked daily logarithmic return and yearly ESG data of over 330 companies in the S&P 500 across three periods — 2006-2010, 2011-2015 and 2016-2018. They considered the first period to be an ESG crisis period due to the 2008 financial crash versus the calm stretches afterward.7

They found that ESG factors mitigated risk during crisis periods but only up to a certain point. Risk magnitude was highest for companies in the worst and best quartiles for ESG factors. Being middle of the pack for ESG was better for risk magnitude. It's possible that investors overweighted top ESG equities believing they would immunize against downside risk during periods of uncertainty.

The future of ESG and equity valuations

ESG risk and return is a rich area of study that will continue to mature to meet growing investor demand. While recent studies have created some new insights into how ESG factors matter for valuations, there is still no clear roadmap on how to precisely apply these findings to a subject valuation.

Measuring ESG risk is complex and depends on factors such as (1) changing investor demand over time, (2) whether an asset specializes in E, S or G factors, (3) the international region of an asset and (4) cyclical macroeconomic conditions. However, tracking the latest research can help analysts better estimate the ESG risk premium or discount for their models.

By incorporating these findings, finance leaders can feel more confident setting valuations under these new investment conditions.

Key takeaways

- ESG risk factors will have a growing impact on equity valuations going forward and should be part of financial models.

- Rating systems can help identify ESG vs. non-ESG investments, especially with companies that blur the line by scoring highly in one category and poorly in another.

- Investor preferences have led to some positives for ESG investments, such as lower required returns and reduced cost of capital.

- The impact of ESG on valuations is not always obvious, and there is no clear roadmap for these new factors. Finance leaders should keep tracking the latest research as they incorporate these trends into their analyses.

Related Readings

Supporting our clients’ sustainability journeys with solutions and tailored advice

Citizens is working to create a stronger and more sustainable future by reducing emissions at Citizens, investing in renewable energy and counseling clients on their sustainability journeys.

Deleverage or invest? Achieving financial flexibility in a mixed market

A mindset of financial flexibility can help companies align its capital with strategic plans in murky market conditions. Find out the mix of priorities companies are balancing and strategies to consider to help find the right balance between investing and deleveraging.

2023 M&A Outlook: Second Half Perspectives

While economic uncertainty remains, green shoots of optimism are beginning to appear. Citizens Capital Markets & Advisory experts preview what they expect could be in store for the rest of 2023.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

1 "Report on U.S. Sustainable and Impact Investing Trends 2022," US SIF Foundation: 1, Home | US SIF. Sustainable investments are defined as investments with ESG criteria incorporated.

2 "Global Sustainable Investment Review 2020," Global Sustainable Investment Alliance: 9, http://www.gsi-alliance.org/wp-content/uploads/2021/08/GSIR-20201.pdf. Sustainable investments are defined as investments that consider ESG factors in portfolio selection and management. The GSI Alliance uses a more inclusive definition of sustainable investments than the US SIF Foundation does.

3 "The ESG Premium: New Perspectives on Value and Performance," McKinsey & Company, (February 12, 2020).

4 Lasse Heje Pedersen, Shaun Fitzgibbons and Lukasz Pomorski, "Responsible Investing: The ESG-Efficient Frontier," Journal of Financial Economics 142, No. 2, (November 2021).

5 Julia L. Pollard, Matthew W. Sherwood and Ryan Grad Klobus, "Establishing ESG as Risk Premia," Journal of Investment Management 16, No. 1, (2018). Pollard et al. based their five risk factors on the Fama and French five factor asset pricing model.

6 Ashish Lodh, "ESG and the Cost of Capital", MSCI, (February 25, 2020), https://www.msci.com/www/blog-posts/esg-and-the-cost-of-capital/01726513589.

7 Karoline Bax, Ozge Sahin, Claudia Czado and Sandra Paterlini, "ESG, Risk and (Tail) Dependence" (whitepaper), (November 10, 2021).

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE