Risk Management: Interest Rate, Commodity and FX

By Richard Aidala, Co-Head of Global Markets, Citizens Commercial Banking

Why it Matters

- Many companies do not understand the scope of their interest rate, foreign exchange, and commodity price risks, which can wreak havoc on their planning processes.

- Companies need to examine whether they have the right risk management and mitigation strategies in place or whether to improve them for better planning.

- Companies without the right risk management capabilities in-house could work with a partner to help set up the new risk management strategies.

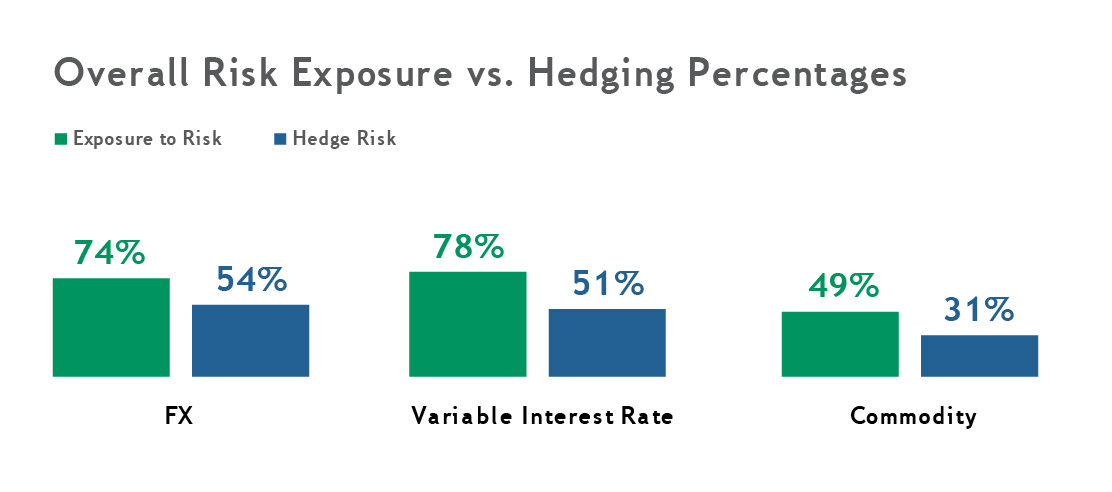

In a complex, interconnected world risks are everywhere and can wreak havoc with financial projections, budgets, and the expectations companies set with stakeholders. A recent Citizens Commercial Bank Risk Management Study of 350 U.S. publicly listed companies revealed how widespread these risks are: 78% are exposed to interest rate risk, 74% to foreign exchange risk, and just under 50% to commodity risk. Yet only about half of these companies are adequately managing their risk exposures, which hurts their planning processes.

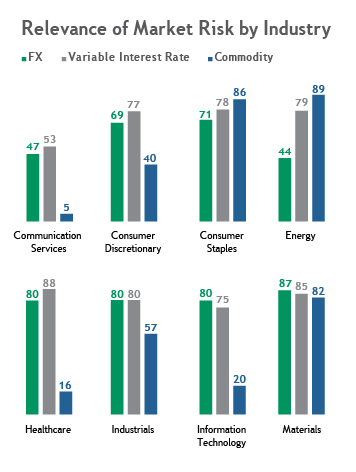

Risk exposures tend to vary by industry. For example, companies in the healthcare, industrials and materials sectors are capital-intensive, and are traditionally heavier borrowers, relatively speaking. As a result, companies in these sectors become much more exposed to changes in interest rates over time. Meanwhile, Foreign Exchange (FX) risk is generally based on how much of a company’s business is transacted overseas vs. domestically. But other factors can come into play. The energy sector is protected from FX risk because international oil and refined products, such as gasoline and diesel, are traded in U.S. dollars at the wholesale level.

Given the complexity and types of risks, it’s worth re-examining what risks a company is exposed to and some of the assumptions that have guided risk management and mitigation. Many economic assumptions ingrained over the last couple of decades, such as low inflation, low interest rates and low commodity prices, may be upended as we emerge from the Covid-19 global pandemic. If so, there will be huge risk management implications for corporate planning and performance that senior leaders must carefully consider. They will need to ensure they have the proper risk management in place for interest rate, FX and commodity risks. And if a company lacks these capabilities in-house, leadership might need to find a partner to work with to help stand up these risk mitigation strategies.

If Interest Rates Rise, Risks will Grow

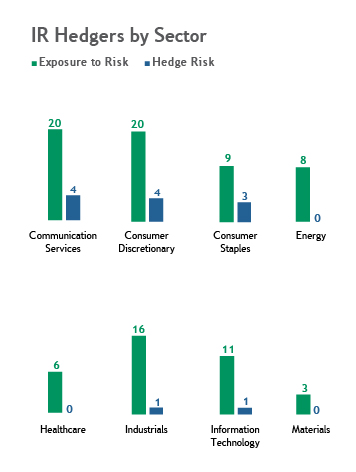

Our study found that 78% of companies are exposed to interest rate risk, for example, having floating-rate debt tied to Libor, or The London Inter-Bank Offered Rate. While only 51% are hedging that risk (i.e., converting its variable rate liability to a fixed rate liability via an interest rate swap), the exceptionally low interest rate environment of recent years makes that understandable. Among those that are hedging, Citizens found that 91% of companies use interest rate swaps, a fundamental forward hedging tool, with a smaller portion using options, such as interest rate collars (13.5%), caps or other option-based strategies.

Four Common Interest Rate Hedging Tools

Swap: A contract in which one stream of future interest payments is exchanged for another. These usually involve the exchange of a fixed interest rate for a floating rate, or vice versa, to reduce or increase exposure to fluctuations in interest rates.

Cap: Establishes a ceiling on interest payments. It is a series of call options on a floating interest rate index, usually 3- or 6-month Libor, which coincides with the rollover dates on the borrower's floating liabilities. (A call option is an option to buy assets at an agreed price on or before a particular date).

Floor: A minimum interest rate created using put options, which is an option to sell assets at an agreed price on or before a particular date.

Collar: The simultaneous purchase of an interest rate cap and sale of an interest rate floor on the same index for the same maturity and notional principal amount. These contracts protect against rising interest rates and set a floor on declining interest rates.

But the sentiment in the market is swinging toward the likelihood of rising rates, which would make unhedged positions riskier. Sentiment is shifting partly because interest rates have been at historical lows for years with little chance they could fall further. Also, inflation pressures have accumulated since the onset of the pandemic, and inflation has historically prompted the Federal Reserve to raise rates.

Another reason behind so much interest rate exposure is the uncertainty as the industry phases out Libor. Most banks will stop issuing loans tied to Libor by 2022 and Libor will cease to be quoted in 2023. This can make hedging Libor-linked loans challenging.

Many companies hedge 50% or 60% of their interest rate exposure, keeping about half the debt floating rate. This neutral approach gives them the ability to benefit if interest rates stay low. But with rates so low, and a hedged position relatively inexpensive, some companies prefer the peace of mind of having a fully hedged position. This “all-in” rate perspective brings even greater certainty to their financial planning and budgeting process.

Increased Globalization Heightens FX Risk

Foreign exchange risk is the financial exposure that companies face when they are not protected from potential changes in foreign exchange rates. This exposure can lead to decreased profitability, missed targets, or significant losses. Increasing globalization has made this an issue for businesses of all sizes. Indeed, the Citizens study found that FX risk is nearly as prevalent as interest rate risk.

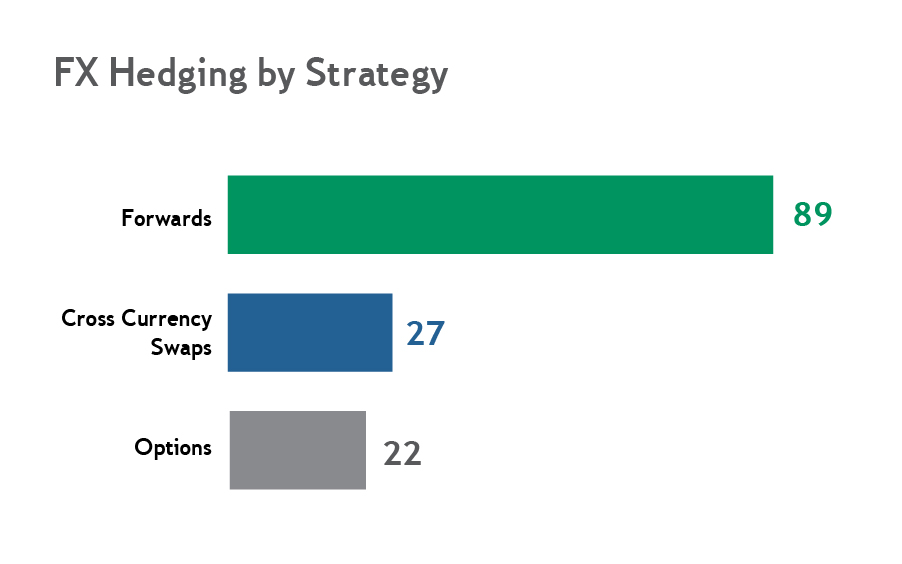

Almost three quarters of the companies analyzed have exposure to FX risk, yet just 54% are managing that risk through hedging. Among those that are hedging, forwards and swaps are the main strategies. However, more advanced strategies are also gaining traction, with 27% of companies using cross-currency swaps and 22% choosing options.

There are several possible reasons that almost half of companies with FX risk do not hedge their positions. One is that management is sometimes uncertain about the extent of the company’s FX exposure, another is a lack of familiarity with various hedging tools. But perhaps the biggest reason is that many companies simply fail to realize they have FX exposure, either because it’s crept in as the business has grown (organically or through acquisitions), or because they’re not fully aware of contractual terms that allow customers and suppliers to reprice goods and services. In other words, while interest rate risk is fairly obvious, FX risk can be more hidden.

For example, a company might start out small with only domestic suppliers, but over time, as it grows, it might tap into the global supply chain. While companies often begin by making their overseas transactions in US dollars, they may recognize the benefits of selling and buying in foreign currencies. Overseas customers often prefer to make purchases in their local currency since it reduces the complexity that comes with making purchases in a foreign currency. On the flip side, by requesting invoices and making payments in the currency of the supplier, a company has more precise information about what it’s paying suppliers and thus more control of its procurement process in general. Hedging this new risk is an important way to bring more certainty to the financial planning and budgeting process.

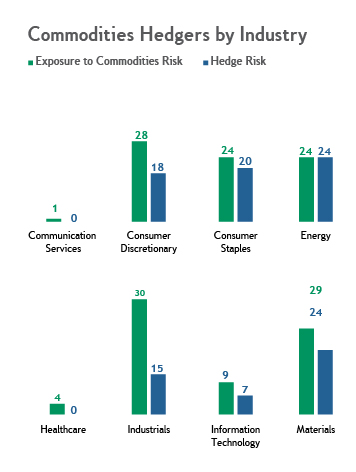

Commodity Risks are Often Difficult to Hedge

Commodity risk is the least prevalent of the risks we studied. Just 49% of companies are exposed to commodity risk (with most of that tied to energy as opposed to metals and/or agricultural products), and only 31% are hedging that risk. These findings make sense when you consider the relative decline in the share of industrial, manufacturing and other commodity-consuming sectors in the US economy. And even for companies in these industries, commodity exposures are often difficult to hedge, given the highly fragmented underlying markets.

While the percentage of companies hedging their commodity risk is relatively low, that may change if commodity prices and volatility were to spiral upward. Oil prices, for example, which briefly traded in negative territory during the pandemic, were north of $80 per barrel in the fall of 2021. At the same time, natural gas prices rose so high in Europe—in part due to high carbon prices, low wind generation and nuclear plant unavailability--that some factories shut down. If those events are any guide, the evolution from fossil fuels to green energy won’t be smooth and commodity volatility will persist.

As commodity risk becomes more acute, senior leaders are paying more attention. Unlike interest rate and FX risk, which are handled by the CFO or Treasurer, commodity risk is typically handled by the procurement department lower down in the corporate structure. But now big energy consuming companies--such as makers of cement, steel and fertilizer--are beginning to elevate these discussions to the executive suite. At the same time, many other companies—particularly those with large fleets of vehicles, or which rely on other companies for transportation--are suddenly seeing the true extent of their own energy exposure.

Now is an excellent time to examine some of the long-held assumptions that have guided risk management processes and mitigation. As part of the budgeting and financial processes, assessing the company’s risk exposures is an effective way to uncover untapped areas of opportunity or hidden areas of risk. The more risk a company can take off the table, the more likely it can achieve its financial plans, and meet the expectations of stakeholders. Engaging a partner with hedging expertise to assess these risks can be an important first step toward setting up a new risk management strategy.

Key Questions to Ask

- Do I have a full understanding of the risks my company is exposed to, whether interest rate, foreign exchange or commodity risk?

- Do we factor these risks correctly into our planning processes?

- Is my current risk management and mitigation adequate to handle the risks my company faces today and in the future?

- Do I have the right risk management capabilities in house to meet today’s challenges, or should I find a partner to help set up these capabilities?

Rich Aidala is the Co-Head of Global Markets at Citizens. Since joining the bank in 2007, Rich has held a variety of roles, including Head of Sales for Global Markets.

Related Readings

Financing for Growth and Efficiency

Life Cycle Financing with Asset-Based Lending

The public to private equity pivot continues

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE