Life Cycle Financing with Asset-Based Lending

By Brent Hazzard | Head of Asset-Based Lending and Asset Finance, Citizens Corporate Finance

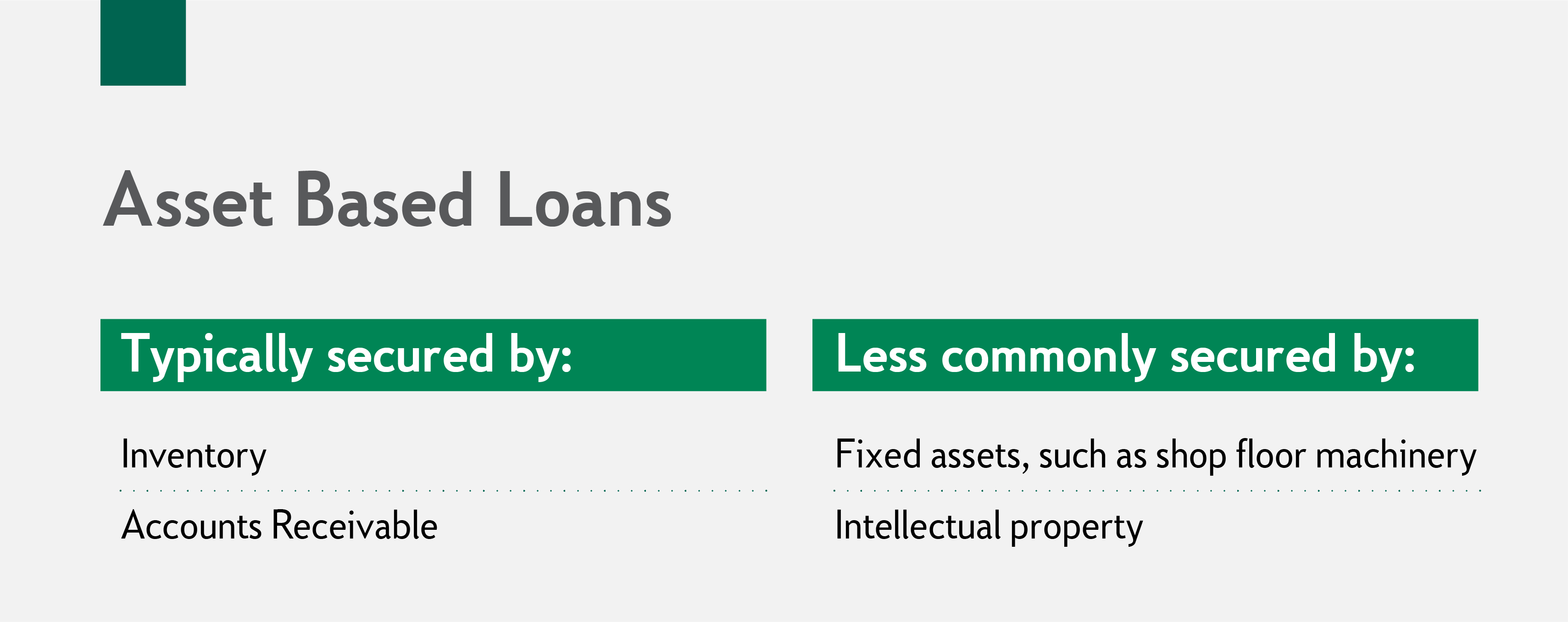

Asset-based lending at a glance

- As the economy improves, asset-based lending (ABL) is an efficient way to access funding for growth and acquisitions

- These loans have a more flexible structure than cash-flow business loans and are more competitively priced

- An asset-based loan is a suitable lifecycle lending option for many companies, including retailers, manufacturers, wholesalers, staffing, distribution, transportation, and logistics companies

- Finding the right lender is key to unlocking ABL benefits

Many companies rely on asset-based lending (ABL) to manage the ups and downs of the economic cycle, and the COVID-19 pandemic has shown once again how flexible and valuable this source of funding is. As economies shut down and corporate cash flows dried up, businesses could still turn to ABL for much needed working capital, whether it was to keep the lights on, or make other more strategic moves. Now, with economies starting to rev up again, businesses can use these same ABL facilities to respond to increasing customer demand, ramp up operations, and take advantage of better economic times.

While ABL activity continued during the pandemic, the market definitely took a hit. In 2020, ABL volume totaled $72.4 billion in the U.S., the lowest since 2010, according to data from Refinitiv. But the rebound is already under way. In the first quarter of 2021, volume totaled $26.7 billion, up 67% from the first quarter of 2020. In light of this turnaround, and ABL’s potential to help companies capture near-term growth opportunities, it’s worth reviewing the nuts and bolts of these credit facilities.

How asset-based lending works and typical borrowers

ABL entails lending against the value of a company’s assets. Usually that’s inventory and accounts receivables (AR), and, less commonly, intellectual property (e.g., a company’s brand) or a company’s fixed assets (e.g., the machinery on a shop floor). The more confident lenders are in a company’s underlying value, the greater advance rate a lender will be willing to provide – often as high as 85% to 90% of the net orderly liquidation value (NOLV) of the assets.

ABL lenders monitor the value of the assets over time, since the value will vary depending on a company’s sales, collections and production. As the asset values expand, the borrowing capacity on the secured facility increases. Likewise, as the asset values decrease, additional monitoring may be necessary, especially when pre-defined thresholds are broken.

Therein lies the flexibility of asset-based lending facilities – the lending parameters are set at the outset, while the value of the assets determines the maximum borrowing capacity and reporting requirements. This structure makes asset-based lending attractive to companies with rapid growth, inconsistent earnings, seasonality, and cyclicality – a good choice for lifecycle lending. ABL loans are particularly popular among companies with lots of inventory, such as retailers, manufacturers, wholesalers and distribution companies.

Common asset-based lending uses

The most common use of ABL is for working capital. A seasonal business might use the funds to build up inventory, while another may use it to buy new equipment or launch a new product line. Some companies choose to put an ABL loan in place and have the money easily accessible in the event of an unexpected opportunity.

ABL is also utilized for more sophisticated financing purposes. Besides working capital, ABL can also be used as part of acquisition financing. If a company already has business cash-flow loans in place, but needs more capital for a purchase, it can use ABL to ratchet up the borrowing and gain additional leverage. As long as the ABL lender is confident in the borrower’s underlying assets, it is not overly concerned about leverage. Banks are already seeing an uptick in customers lining up ABL for acquisition financing — a trend that’s likely to continue in 2021 as the economy starts to heat up.

The third major use for ABL is for a dividend recapitalization. Companies use these funds to make a special payment to an owner, or shareholder, who is retiring or cashing out of the business. Since, in this case, the cash is leaving the business and not being reinvested, a lender may be especially vigilant to ensure that plenty of excess liquidity remains — at least 15%-20% — for the company to continue to provide sufficient working capital.

Benefits of asset-based lending

To understand the benefits of ABL, it’s helpful to contrast these loans with traditional cash-flow business loans. A big difference is that cash-flow loans typically come with various covenants that require the borrower to fulfill certain financial conditions, or limit the borrower from taking certain actions. Some examples of financial covenants include maintaining a certain leverage ratio, interest-coverage ratio, or minimum free cash flow. Meanwhile, the covenants might restrict a dividend recap, or force the company to seek a waiver, or amendment, to make an acquisition.

ABL loans, on the other hand, typically have only one covenant triggered by the borrower’s liquidity (normally, to keep excess liquidity at 10 to 15%). While operating within that covenant, borrowers are generally free to use the capital as they see fit. This flexibility comes with an additional requirement, however. ABL reporting is a bit more rigorous in terms of its frequency. The company needs to report on its collateral on a monthly basis to the bank. This means that in order to qualify for an ABL loan, a company needs the systems and processes in place to keep a close accounting of its inventory or AR.

As noted earlier, ABL is also a way to gain additional leverage. Companies and private equity sponsors often use this additional leverage for acquisitions, or simply as a way to access more working capital easily, and as needed, to grow the business.

Last, but not least, ABLs are competitively priced. In today’s environment, an ABL loan could easily be priced up to 200 basis points below a comparable cash-flow loan.

Finding an asset-based lender

First and foremost, a company wants a lender that understands their business, and, ideally, the specific products it offers. This knowledge helps to properly value the inventory and AR, and also means the lender can act as an advisor to help grow the business. For example, a bank with sector expertise might have insights on possible acquisition candidates.

A company should also look for lenders with experience in ABL. Banks will typically hold asset-based loans starting at approximately $5 million. However, when the size of the ABL loan approaches $75 million or more, the loan is often syndicated among several banks. This is when ABL experience is critical, since the lead bank must organize the syndicate financing. Through this process, an experienced ABL lender can assemble and scale the bank group necessary to assist with the company’s borrowing needs. This will enable the lender to fund the operations, grow the business, or finance an acquisition.

ABL is widely recognized as a good option for lifecycle lending, given its ability to fund companies through the peaks and troughs of the economic cycle, for everything from operations to acquisitions. Indeed, even though ABL slowed in the darkest days of the pandemic, activity quickly began to rebound by the end of 2020. Now, as the economy comes back to life, these companies are in an excellent position to seize new opportunities.

Key takeaways:

- With the economy improving, companies looking to access growth capital for operations, or to make acquisitions, should consider ABL

- An asset-based loan is a senior secured loan with a borrowing limit based on a percentage of the net orderly liquidation value (NOLV) of the company’s assets, usually AR and inventory

- Asset-based loans have a flexible structure, typically with only one covenant tied to liquidity, and are an efficient way to increase leverage.

- Companies with rapid growth, inconsistent earnings, seasonality, cyclicality, and lots of inventory, should consider ABL

- It’s important for a company to choose a lender familiar with its industry and product(s), and use a lead bank with syndication experience for ABL facilities that exceed $75 million

Brent Hazzard heads Citizens Asset Based Lending, Asset Finance, and Transitional finance teams. He has over 30 years of experience as a lender. Learn more at citizensbank.com/corporate-finance/financing/asset-based-lending.aspx

Related Reading

5 Steps to Succession Planning

By taking steps to evaluate your business and prepare it for a transition, you can maximize value and bolster the company's position.

The public to private equity pivot continues

As the private capital ecosystem has expanded over the last 25 years, the private equity-backed company count has climbed, while the number of public companies has fallen sharply. Explore what these trends mean for midsized companies.

Decreasing Greenhouse Gas Emissions

Why reducing the climate impact of your business could be easier than you might expect.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE