With Currency Volatility Rising, it’s Time to Review Forex Hedging Policies

By Eric Merlis, Co-Head of Global Markets

With Currency Volatility Rising, it's Time to Review Forex Hedging Policies

By Eric Merlis, Co-Head of Global Markets

Download a print-friendly version of this article.

Why this Matters

- With currency markets more volatile than they have been in years, companies need to adopt a holistic approach to their forex hedge programs. For some companies it may make sense to incorporate the firm’s interest rate and/or commodity risk.

- By designing a “risk-based” approach to forex hedging that fits the goals of the business, companies can keep currency volatility within a predictable range so they can make plans and run their businesses.

- To design an effective hedge program, a company should enact a four-part framework: (1) Articulate Corporate Goals & Objectives, (2) Identify & Analyze FX Exposures, (3) Design & Implement a Hedging Strategy, and (4) Review & Monitor the Hedge Program.

Currency markets are more volatile than they have been in years. The U.S. dollar is at a 20-year high and there is enormous geopolitical and economic uncertainty. In response, U.S. companies of all sizes need to reevaluate their foreign exchange (forex) risk and hedging policies. These hedging policies must fit the goals of the business by keeping currency volatility within a predictable, tolerable range so companies can run their businesses with more operational certainty.

Despite the urgency to act, this review must be done methodically. Before you design a hedging strategy, some important homework and self-reflection must occur regarding the company’s goals and risk tolerance. Otherwise, the hedging program won’t work effectively. To manage this review process, consider using a four-part framework: Articulate Corporate Goals & Objectives, Identify & Analyze FX Exposures, Design & Implement a Hedging Strategy, and Review & Monitor the Hedge Program (see figure 1). Once in place, this framework should guide an iterative, ongoing process to continually refine the hedging program.

Articulate Corporate Goals & Objectives

The primary objectives for companies when hedging forecasted transactions can be broadly similar, such as smoothing the impact of FX rates over time on financial performance, assisting senior management’s ability to forecast financial performance, protecting budgeted results, improving pricing of goods/services, and managing FX risks related to capital projects.

But when setting more specific goals for a company, you first need to identify the firm’s priorities and consider various tradeoffs among those priorities. Priorities and tradeoffs may hinge on how and where the company conducts its business. If most of a company’s sales occur overseas, a stronger dollar will negatively impact its financials since bringing those revenues onshore will result in fewer dollars. On the other hand, companies that sell in the U.S. but buy raw materials from overseas benefit from a strong dollar since those raw materials are cheaper to purchase in dollar terms. In either case, forex risk exposes the companies to ongoing operational uncertainty, but their differing business footprints and exposures may result in different risk management objectives.

You must also decide what financial performance measures you want to focus on. For example, some companies focus on how forex risk will impact the balance sheet. Currency fluctuations have a direct impact on recorded assets and liabilities, payables and receivables, cash, etc. These are visible items that must be explained to shareholders. Thus, hedging to reduce volatility in the balance sheet is often a goal. Another reason to hedge is to reduce risks related to forecasted revenue and expectations. In this case, management wants to protect the viability of its business plan and reduce quarter-over-quarter, and year-over-year volatility. Different hedge programs may be used to address balance sheet risk and FX risk related to forecasted revenues and expenses.

To achieve their goals, companies should take a risk-based approach to hedging as opposed to a market-based approach. The goal of a risk-based approach is to lower operational risk by keeping currency fluctuations within certain tolerable bounds. This approach demands a holistic view across all of a company’s different types of risk and an understanding of how they fit together (i.e., how they might magnify risk or offset each other).

By comparison, a market-based approach is more about trying to time the currency markets. The problem with this approach is that if a company only hedges when it predicts an adverse FX move, it’s exposed to significant FX risk at other times. For example, a large U.S. company with significant overseas sales hedged every fall using a market-based approach. In 2021, it decided not to hedge against foreign revenues, reasoning that the dollar was overvalued. But the dollar continued to strengthen causing the company significant financial pain that could have been avoided. By taking this market-based approach, the company did not properly account for other risks within the enterprise or consider how much forex risk is acceptable.

Identify & Analyze FX Exposures

A company with limited international operations might have good intuition about its currency exposures. But once a company begins to expand operations abroad--to build out its supply chain for example--complexities quickly snowball, making it harder and harder to understand the scope of the risk and mitigate it. Thus, it is critical to conduct a data-driven analysis regularly to understand how certain currency moves over the next six, 12, and even 24 months would impact the company’s balance sheet exposure, forecasted cash flows, or a specific event such as a planned acquisition. The key question for executives is what level adverse outcome can the company tolerate?

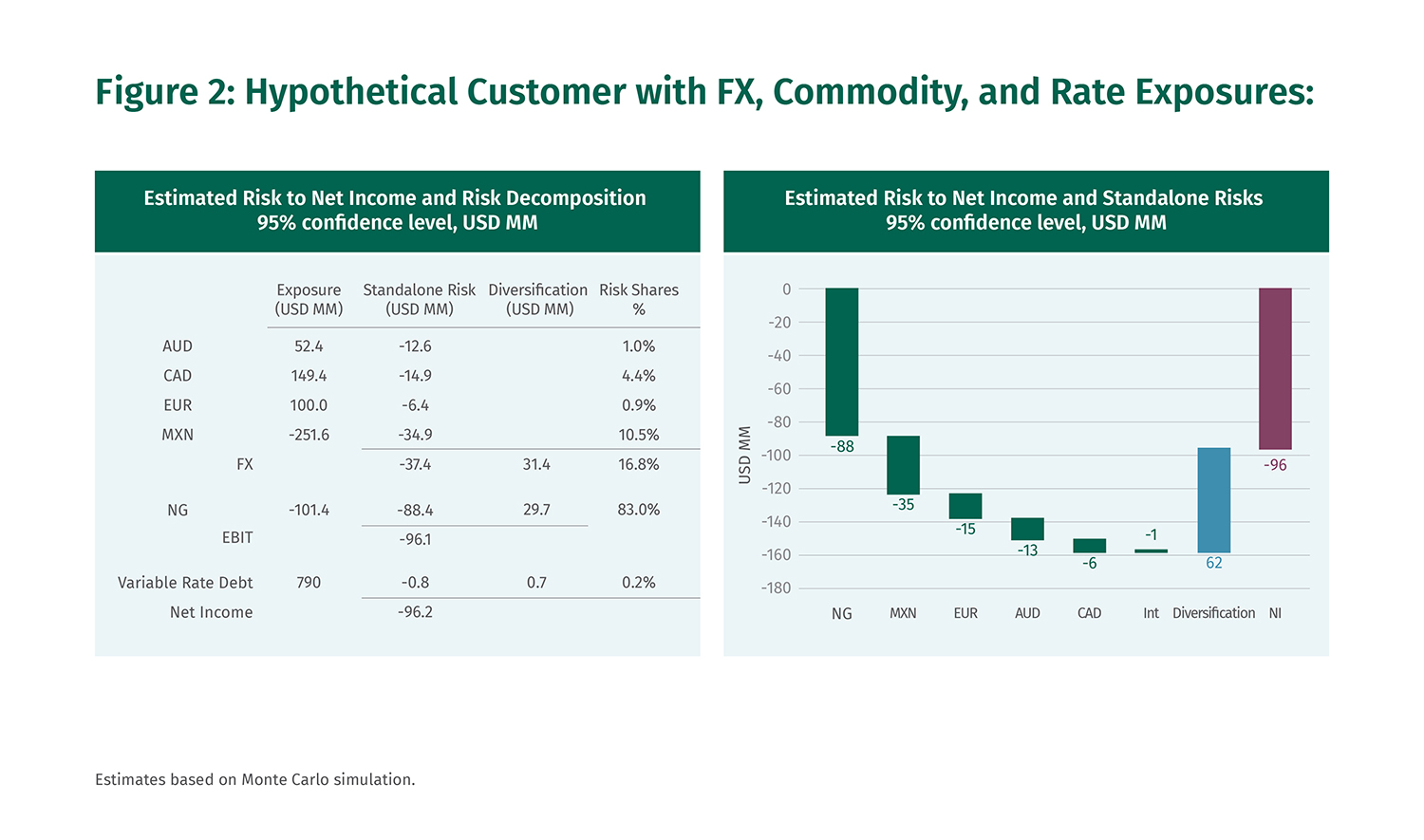

As noted, taking a risk-based approach requires a holistic view to understand how all of a company’s risks fit together. For example, a company’s risk exposures may partially interact can partially offset each other and create “natural” hedges. Consider the following hypothetical example of a U.S.-based company with significant global sales (see figure 2). If you add up the individual currency risk exposures (Australian dollar, -12.6 MM; Canadian dollar, -14.9 MM; Euro, -6.4 MM; and Mexican peso, -34.9 MM), along with natural gas (-88.4 MM) and interest rate risk (-0.8 MM) exposures, the sum suggests that total net income could be almost $160 million less than forecast (with 95 percent confidence). But these different risks don’t move in lockstep, so simply adding them up doesn’t give you a true understanding of the company’s exposure and hedging requirements. Based on historical correlations in this example, the diversification benefit reduces the risk by roughly $60 million, so the company’s exposure on a portfolio basis is estimated to be $96 million.

Design & Implement a Hedging Strategy

After doing the homework to understand your goals and analyze your currency exposures, it’s time to design the hedging strategy. So, in figure 2, a well-designed FX hedging strategy may not involve a 100% hedge on each of the four currencies, as that may nullify some of the natural hedge between currency and natural gas risks. Better to construct a hedging strategy that leverages any free diversification benefit; in the example above, maybe only portions of the individual currency transactions should be hedged. The art and science of designing a hedging strategy is determining the minimal amount of hedging necessary to achieve a target risk level, while keeping costs down and reducing operational complexity, and understanding the trade-off between targeted risk level and the cost and complexity of hedging. Identifying strategies that are efficient with respect to risk and cost/complexity, what’s known as the “efficient hedge frontier,” is often not obvious without deep analysis.

All this hard work articulating goals, assessing currency exposure and designing a hedging strategy will not work if the company does not implement the FX hedge program systematically over the long term. That means writing down the hedge policy, outlining specifically how the company will carry it out going forward, including executing new hedges every month and every quarter.

Review & Monitor the Hedge Program

A company should not root for or against the forex hedges it puts in place. It’s not appropriate to say, “we were out of the money on this hedge, so we shouldn’t have done it.” Instead, a company should judge the hedging strategy on whether it kept the currency volatility within an expected, tolerable range to run the business over a six, 12, or 24 month period.

Companies should regularly evaluate their FX exposures and the effects of their hedge programs, incorporating new data whenever possible in an agile manner.

With currency markets more volatile than they have been in years, it’s important for companies to reevaluate their forex hedging programs in the current environment. It’s a complex task, but the four-part framework can help companies tackle the challenges systematically and ensure that the program remains effective for years to come.

Key Takeaways

- To design a hedging program that controls forex exposure on an ongoing basis, companies need to enact a “risk-based” strategy in four steps.

- Set the goals of the hedging program by identifying the firm’s business priorities and consider various tradeoffs among those priorities.

- Assess currency exposure by conducting a data-driven analysis regularly to understand how certain hypothetical currency moves over the next 6, 12, and 24 months would impact the company.

- Design a hedging strategy that fits the goals of the business by considering how different forex exposures—and other types of risks-- offset one another. This will allow the company to enact the minimal amount of hedging necessary to achieve goals, keeping costs down and reducing operational complexity.

- Invest upfront in technology, systems and processes that are scalable—as well as workforce capabilities—to put the right monitoring and reporting infrastructure in place to operationalize the strategy.

Eric Merlis, Managing Director and Co-Head of the Global Markets team, has responsibility for the Interest Rate Derivatives, Foreign Exchange and Commodity Sales and Trading groups. He holds an MBA in finance from Southern Illinois University at Carbondale and a BA in Philosophy from Siena College.

Related Reading

Managing Risks: Interest Rate, Commodity and FX

Learn how risk management planning can help limit risk exposure. Many companies are unaware of the scope of their interest rate, foreign exchange and other risks.

Financing for Growth and Efficiency

Successful capital planning starts with setting your business strategy and pursuing the right financing to drive objectives.

Why it Could be Time to ‘Go Private’

Now could be the time to “go-private” for many public companies. Learn about the basics and benefits associated with companies who choose to go private.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE