By Jonathan Heuser, Head of Trade and Supply Chain Finance

- Though global trade volumes have recovered, the pre-COVID trade war and post-COVID supply chain issues continue to create challenges for importers and exporters.

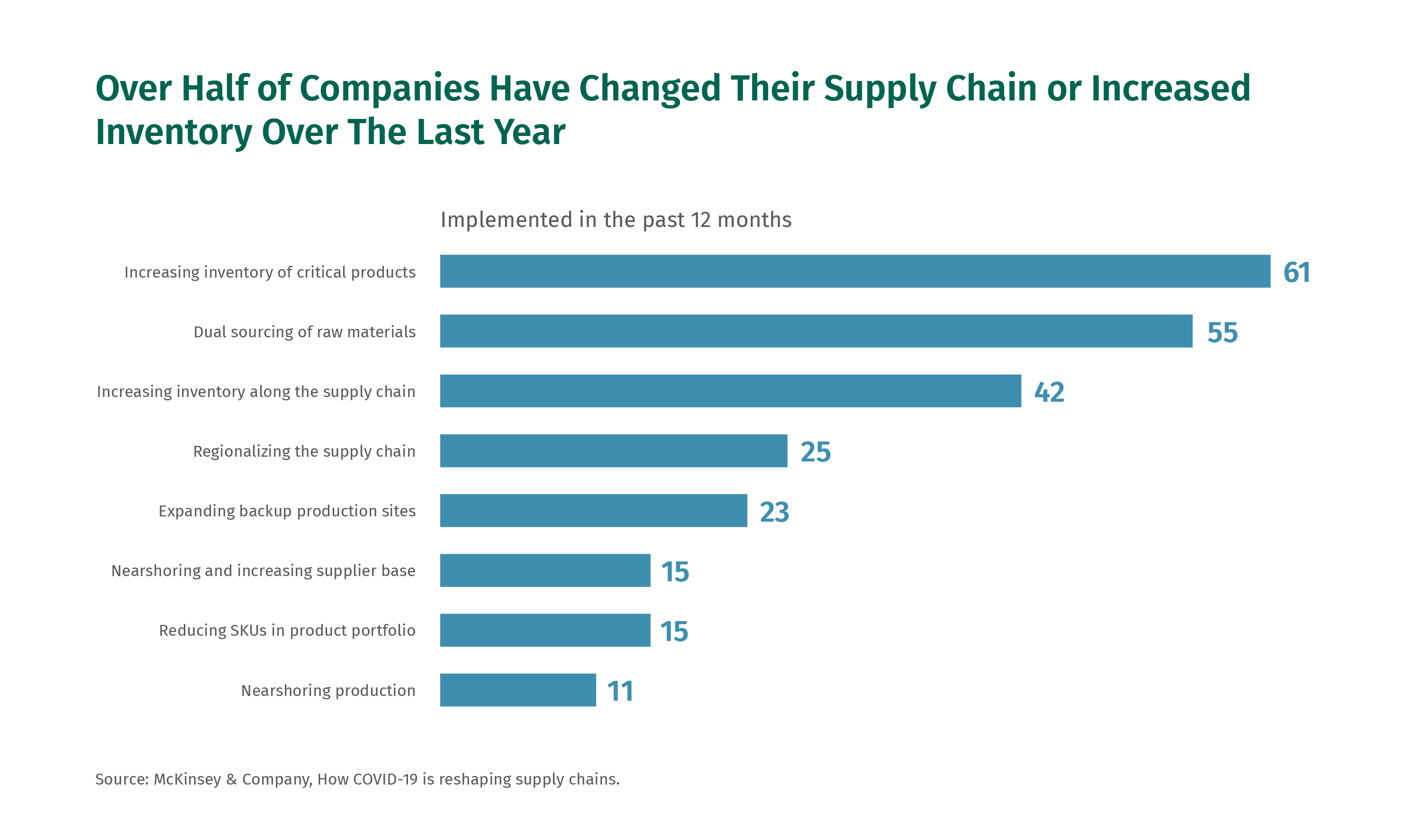

- A quarter to a half of U.S. companies did some kind of near-shoring or otherwise revised supplier strategy in response to the pandemic, while two-thirds of companies say working capital efficiency is a key issue.

- Letters of credit can be a useful tool for companies who are adding new trading counterparties to their buying or selling activity, and FX hedging programs are key to reducing the risks of foreign currency payments.

- Supply chain finance programs can optimize cash flow in supply chains, helping to lower the costs of working capital for some companies.

Global trade volumes may have recovered from the shock of COVID-19, but challenges remain for U.S. companies buying and selling across international borders. New counterparty and currency risks face companies that have pivoted to new suppliers and new markets. Meanwhile, rising interest rates and inflation continue to pressure working capital and push borrowing costs higher. Fortunately, there are financing tools available that can help companies mitigate these dual risks.

For transactions that require trust, a rough patch

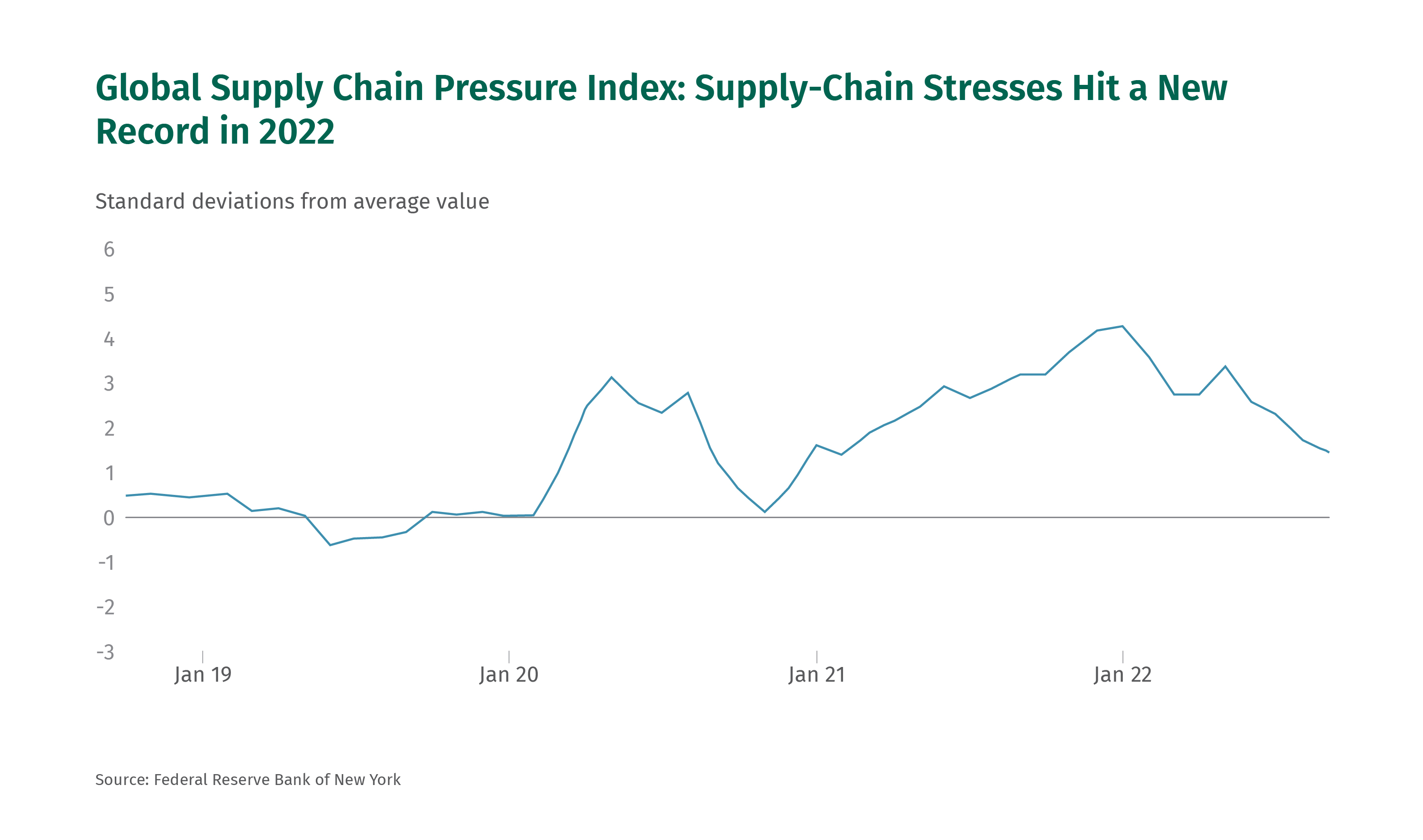

The supply-chain snarls of recent years have posed major challenges for all companies, but mid-corporate and middle-market companies have been hit particularly hard. Moreover, these stresses came on the heels of an already-disrupted period for global trade.

The Trump administration’s trade war with China reversed a long period of falling trade barriers. As the U.S. levied tariffs on Chinese imports, and China retaliated with tariffs on some U.S. exports, trade patterns shifted—including a significant trend toward Vietnam as a key U.S. supplier of goods and materials. In fact, analysis from the National Bureau of Economic Research suggests that the U.S.-China trade war increased global trade by 3% and drove significant activity toward countries beyond China.

COVID-driven supply-chain blockages added fuel to the fire. According to a National Retail Federation survey in early 2021, 98% of retailers said they had been impacted by delays at ports or other shipping delays, as labor challenges, supply shortages, and quarantines rippled through manufacturers, ports and distribution networks. These blockages caused many U.S. importers and exporters to rethink supply chains and trade relationships—changes that have imposed a considerable burden on mid-corporate and middle-market companies. Meanwhile, rising rates and inflation have delivered an added set of stressors.

Managing the risks of adding new trading partners

U.S. companies went to considerable lengths to broaden their supplier base during COVID, with up to 55% of companies saying they did some form of “nearshoring” or other supplier diversification. Others sought to broaden their customer base to diversify revenue streams. With those changes come new trading relationships—including customers or suppliers in unfamiliar markets.

Trust is a foundational element of commercial trade. Companies need certainty that they’ll be paid on time or receive delivery as promised, and that there is a functional process to resolve any disputes that may arise.

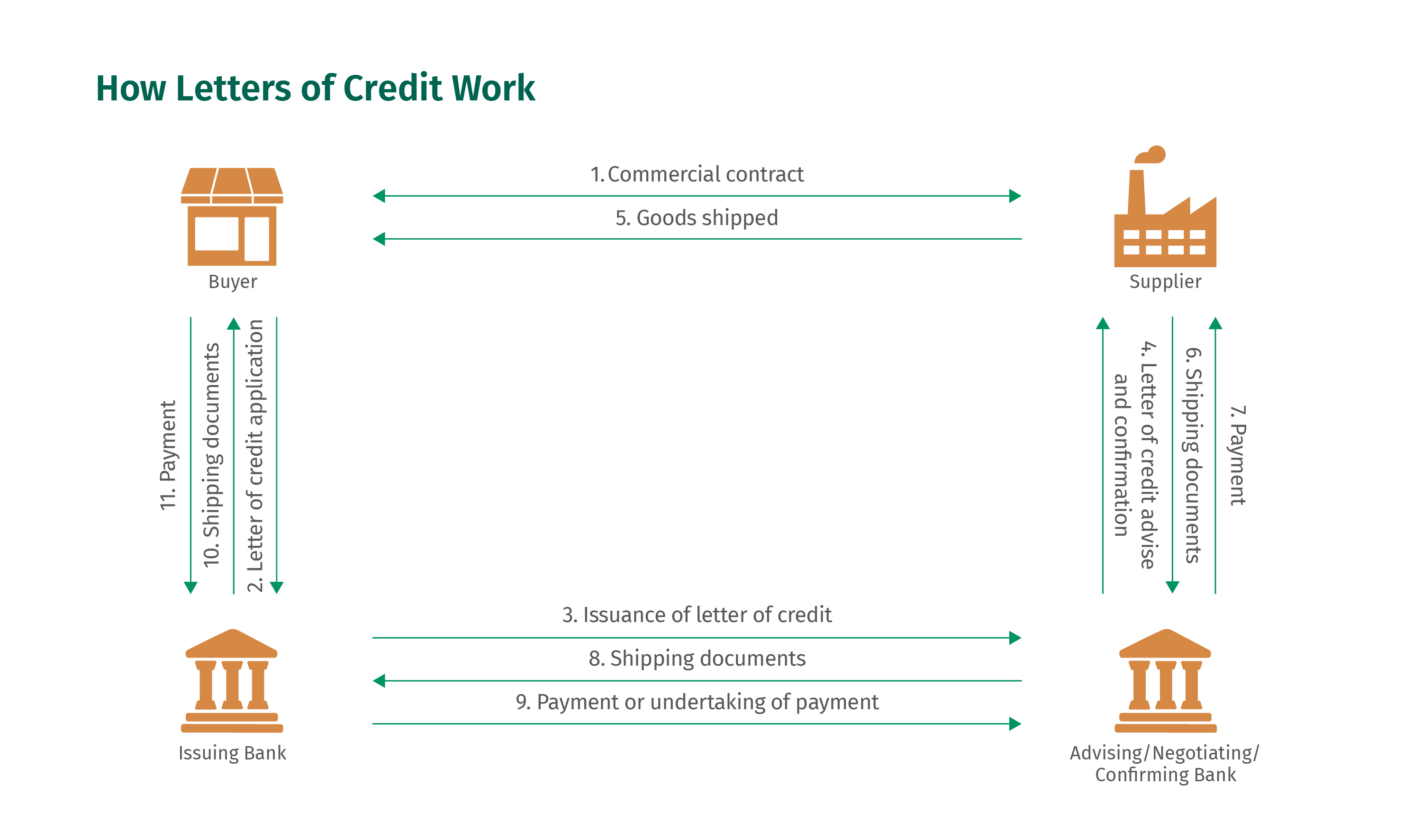

In many respects, open account trade is like an extension of credit from one company to its trading counterparty. Extending credit requires extensive due diligence, access to information, and specialized expertise, which may be difficult for resource-constrained companies to manage effectively. Compounding that challenge, trading across borders adds the complexities of legal jurisdiction and language and cultural barriers, while reducing transparency of information. This is where companies can rely on an important tool: the letter of credit (LOC).

A tool of the trade: Letters of credit

A Letter of credit (LOC) is a longstanding tool, dating back centuries—that remains relevant and useful. There are four parties to a commercial LOC: the buyer, the buyer’s bank, the supplier, and the supplier’s bank. While the commercial contract and shipping of goods takes place between the buyer and seller, the exchange of documents and funds is conducted by the two banks. Once a supplier submits evidence that it has met all the pre-determined conditions of sale, including things like quality checks and proof of shipment, the buyer’s bank is required to make payment to the supplier’s bank.

Any disputes regarding the transaction are governed by the terms of the LOC, which are standardized globally. With these mechanisms in place, an LOC offers buyers and suppliers a foundation for the trust needed to conduct business with one another.

Beyond mitigation of risk, LOCs can offer additional benefits, such as accelerated payment to an exporter selling under extended payment terms.

A tool of the trade: FX hedging programs

Companies diversifying their sales or sourcing into new countries may also find themselves contending with new currency risks. Though many trade transactions are denominated in dollars, U.S. companies may still find themselves facing volatility in exchange rates, impacting their inventory costs or revenues.

FX hedging can be like a customized insurance policy with coverage defined as narrowly or broadly as desired.

A foreign exchange (FX) hedging program is one way that companies manage currency risks. Programs are customized to a company’s specific situation, offering a way to limit exposure to currency fluctuations in a specific time period, within a specific band of currency values, to a specific quantity of currency. In this way, FX hedging can be like a customized insurance policy with coverage defined as narrowly or broadly as desired.

Managing the risks of rising rates and working capital

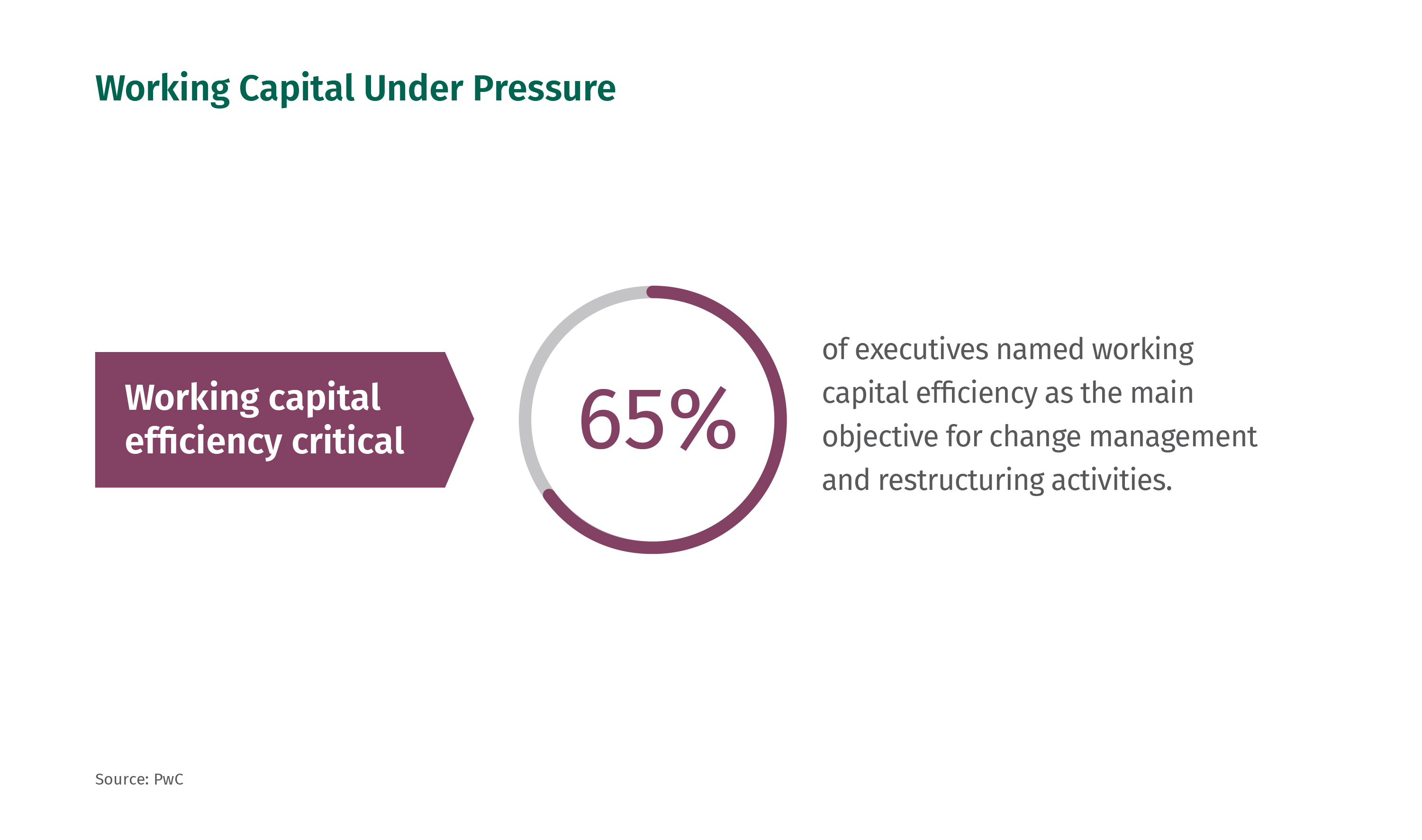

The other key issue facing companies today is rising interest rates, which put added pressure on working capital and financing costs. Two-thirds of U.S. executives said that working capital efficiency is a main objective behind their change management and restructuring activities, according to a recent report from PwC.

As rates rise, borrowing costs are climbing rapidly upward. With inflation still trending at high levels, many are expecting rate policy from the Federal Reserve to remain “higher for longer,” suggesting little relief on the horizon.

A tool of the trade: Supply chain finance programs

Supply chain finance (SCF) is a working-capital management tool that offers an attractive means for mid-corporate and middle-market companies to optimize payment flows for both domestic and international trade—allowing both buyers and sellers to benefit.

Typically, an SCF program would be offered by a large, credit-worthy buyer. Once the buyer has indicated its intent to pay a supplier’s invoice, the bank “purchases” that invoice from the seller, paying them immediately the face value minus a small discount. The bank then collects the full value of the invoice from the buyer when the invoice reaches maturity.

Because the structure of such programs is connected to the creditworthiness of the buyer, the cost of the program is based on the buyer’s credit profile—usually resulting in an attractive financing cost when compared to a seller’s other financing options.

Beyond cost, SCF can also be an appealing avenue for sellers because in effect, it gives them an additional form of liquidity—one that does not affect any of their standing lines of credit. And since it replaces a seller’s receivables with cash, it allows companies to reduce days sales outstanding (DSO) and manage client concentration concerns. Finally, SCF programs can span borders, allowing U.S. buyers to project the strength of their balance sheet even further, helping provide a layer of financial stability to key supply-chain partners, both in the U.S. and abroad.

Trade in the current economic environment

Importers and exporters are coping with changes. Cross-border complexities and working-capital pressure are ongoing challenges for mid-corporate and middle-market companies, and unfortunately show few signs of abating.

But there are options available to help. Letters of credit and FX hedging programs can enable companies to broaden their sourcing or customer relationships with confidence. Supply chain finance programs can create a win-win scenario, speeding payments to suppliers while improving working capital efficiency for both buyers and sellers. These proven tools can be customized to help companies to quantify and mitigate the growing levels of risk presented by the current economic environment.

Here are three considerations for mid-corporate and middle-market companies that are already doing business in international markets or who are evaluating the possibilities:

- Audit the resources you allocate to counterparty management. A letter of credit can be a powerful tool in terms of reducing counterparty, payment, and market risks in your trading relationships. Assess the time and energy your teams have had to devoted to counterparty evaluation, credit analysis, supplier management and the related due diligence in recent years, as well as the costs of write-offs and resolving disputes.

- Assess the currency exposure in your business. Depending on the nature of your international trading, currency exposure could be a small matter or a considerable one. Start by assessing your exposure. It can also be useful to conduct a currency simulation exercise to see how revenues or costs would be affected by an adverse currency move.

- Take stock of your working capital costs. Supply chain finance programs can be a powerful tool to improve working capital efficiency and liquidity costs. Start by reviewing your cost of capital, DSO, and DPO to see how rising rates are impacting your capital efficiency.

Jonathan Heuser is the head of Trade and Supply Chain Finance at Citizens, where he draws upon 25 years of global experience in banking, supply chain finance, and logistics to help mid-corporate and middle market companies overcome the challenges of trade.

Related Reading

With currency volatility rising, it’s time to review forex hedging policies

Currency markets are more volatile than they have been in years, so there is a need to review forex hedging strategies. Read about FX market and hedging insights to consider.

Essential strategies to optimize corporate travel financial management

Traveling for business is presenting new and renewed challenges for mid-market companies. Refresh your strategic thinking on employee travel and expense management with timely insights.

Managing risks: interest rate, commodity and FX

Find out how risk management planning can help limit risk exposure. Many companies are unaware of the scope of their interest rate, foreign exchange and other risks.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Securities products and services are offered through Citizens Capital Markets, Inc., and/or JMP Securities LLC. Members FINRA, SIPC. Citizens Bank and Citizens Commercial Banking are brand names of Citizens Bank, N.A. Citizens Capital Markets, DH Capital, Trinity Capital and JMP Securities are brand names of Citizens Financial Group, Inc. Note: Any testimonials presented are applicable to the individuals depicted and may not be representative of the experience of others. Any testimonials are not paid and are not indicative of future performance or success.