By Michael Cummins, Head of Treasury Solutions

Key insights

- Paper check usage has been on the decline for decades, for businesses as well as consumers.

- Digital payment methods including instant payments, B2C, ACH and virtual cards are on the rise.

- Modern digital payment methods offer superior fraud and security features and are less costly than physical checks.

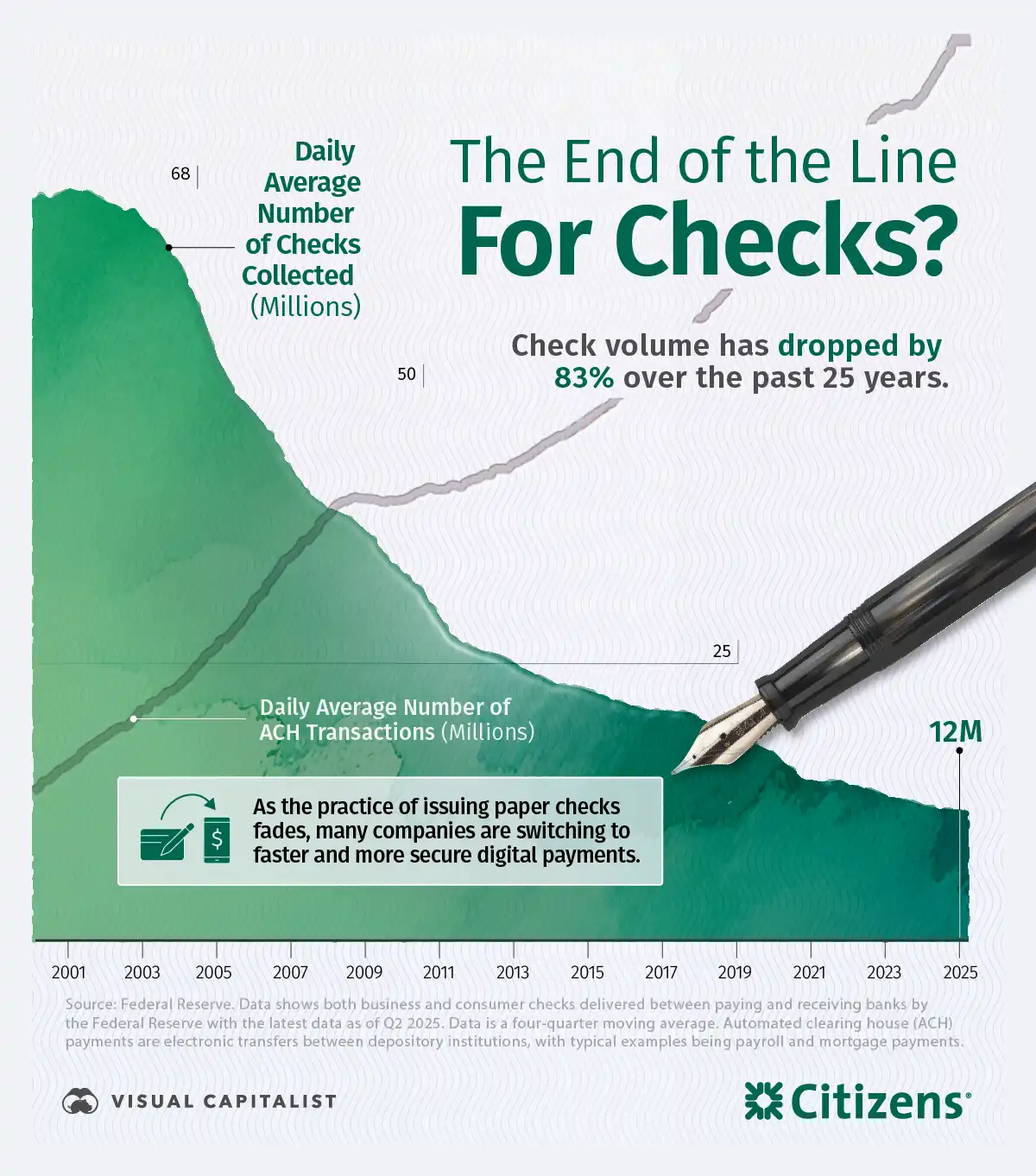

For years, business and consumer check usage has steadily declined, replaced by faster and more secure payment options. According to the Federal Reserve Bank of Atlanta, checks accounted for just 2.5% of consumer payment activity in 2024, down from 6% a decade prior. And since 2000, total check volume has dropped by 83%.

Although businesses have been slower to pivot — the Federal Reserve Payments Study (FRPS) reported that consumer check usage declined faster at 9.8% per year than business check usage (4.0% per year) between 2018 and 2021— the switch to modern, digital payment methods is intensifying. Citizens Bank's Payment Trends Survey shows an accelerating decline in business check volumes, which fell from 59% of all business payments in 2024 to below 50% in 2025.

Check alternatives on the rise

Although roughly half of midsize businesses are still using paper checks, many are rapidly adopting faster, all-digital payment options, including:

- Instant payments: Payment speed is a key priority for midsize businesses, driving interest and adoption of instant payment options. According to Citizens' 2025 Payment Trends Survey, 73% of businesses report that they use either Real Time Payments (RTP) or FedNow, the two dominant instant payment platforms.

- B2C: Also popular among business users are B2C payment platforms like Venmo, PayPal and Zelle—though the popularity of these payment types dipped slightly among midsize businesses from a peak in 2024.

- ACH and wires: ACH and wire transfers have been around for decades (and in the case of wires, centuries), and they remain mainstays of corporate payments, used by more than half of all businesses.

- Virtual credit cards: The adoption of virtual credit cards as a top business-to-business (B2B) payment method climbed for the third year in a row. Many companies are finding that core challenges including security, late, inaccurate or delayed payments, effective working capital management and spend visibility can be improved when paying with a virtual card.

"While checks and ACH are still relevant, we are clearly seeing a prioritization of faster, more efficient options–especially in B2B as businesses rethink how payments are orchestrated," says Michael Cummins, Head of Treasury Solutions at Citizens. "The symbiotic relationship between APIs and real-time payments enables instant experiences at the point of need–though integrating into legacy platforms could be a challenge and the speed of money movement raises the need for AI-based risk management tools."

The real cost of paper checks to your business

For mid-sized businesses, paper checks are a drag on the bottom line. Legacy check-writing is burdened by the “hard” costs of printing, mailing, and processing, along with “soft” costs like staff time and manual data entry errors.

But the true cost of checks becomes apparent when you factor in the increased risk of fraud. In this arena, perception is not always reality. Many people believe checks, as physical items, are less susceptible to tech-driven fraud activities. But the evidence is compelling—there is an association between check usage and incidence of fraud.

A range of new digital payment tools can help companies mitigate fraud losses, extend payables terms, capture early-payment discounts, earn revenue share on card spending, and trim administrative costs related to working capital.

Digital payments offer businesses true cost savings over paper checks, through faster, more secure processing and lower staff and administrative expense.

Modernizing payments for a new frontier

Today’s businesses are showing increasing urgency to transition from paper checks to digital payment alternatives. In 2025, 77% of surveyed businesses that still use cash or checks plan to transition to exclusively digital payments within the next 1-3 years. This is a sharp uptick from 2024, when just 63% planned to transition within the same timeframes.

AI also remains an important subject for leadership teams as they continue to adopt it for new uses and assess its benefits. Treasury executives are using AI in multiple functions, especially customer authentication and other fraud-protection tools. Automation, speed and customer service are also efforts where they are applying AI capabilities. Larger companies are especially likely to use AI to boost payment speed.

Actions to consider

- Engage with your vendors and suppliers. Ask how they prefer to be paid. Today, many suppliers types prefer to receive payment through modern digital methods instead of physical checks.

- Audit your payment partnerships. Assess your banking providers and other partners on their fraud mitigation strategies and protocols. Threat actors are becoming more sophisticated, and it’s critical that your payment methods stay one step ahead.

- Explore a pivot to digital payments. Treasury professionals at organizations ranging from businesses to governments are strongly considering an all-digital payment future—and many are adopting new technologies and tools, including AI and embedded finance APIs. Assess your unique supplier ecosystem and decide what mix of methods makes the most sense for your organization.

Related Reading

How companies can use new payment tools to optimize working capital

Working capital expenses are an increasingly pressing issue. Learn how payments tools and technologies can help companies optimize their capital.

Virtual cards: simplifying supplier payments and strengthening partnerships

Virtual cards continue to rise as a top payment method between businesses. Learn more about commercial virtual cards and their benefits.

2025 Payment Trends

The 2025 Payment Trends Survey from Citizens found faster and fraud-free payments are the priorities among leaders.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE