By Michael Cummins, Head of Treasury Solutions

Key insights

- Although paper check usage continues to decline, check fraud remains a significant threat for businesses, particularly small-to-medium-sized enterprises.

- Per-capita check fraud rates vary widely by state and region.

- Modern digital payment methods offer superior fraud and security features and are less costly than physical checks.

Most businesses are concerned about payment fraud. The mix of fraud threats grows increasingly complex every year, as bad actors use a blend of advanced technology and social engineering techniques to target unsuspecting individuals and organizations.

Smaller businesses seem to struggle even more with the issue. According to Citizens 2025 Payment Trends Survey, 55% of smaller businesses (those with annual revenues of $5M to $50M) reported being impacted by fraud in the last year, compared to 44% of larger businesses (revenues of $50M to $1B).

Checks are particularly prone to fraud

Vulnerability to fraud can vary widely by payment type. While digital and electronic payment channels may appear to be the most susceptible, data shows a correlation between check use and increased reports of fraud and payment theft.

When the U.S. government announced its plan to sunset paper checks in 2025, it noted that checks are 16 times more likely to be reported lost or stolen, returned undeliverable, or altered, compared to electronic fund transfers (EFTs). Meanwhile, reported check fraud continues to rise, with the U.S. Department of the Treasury reporting a 385% increase in check fraud from the start of the COVID pandemic in 2020 through the end of 2023.

Still, many consumers and businesses believe that paper checks, as physical items, are less susceptible to fraud than electronic or digital payment methods. According to the 2025 Payment Trends Survey, 51% of respondents said they use checks because of fraud or security concerns.

Despite this perception, the evidence of an association between check usage and higher rates of fraud is compelling. Our survey found an 11-point difference in the prevalence of check usage by mid-sized businesses that have experienced fraud versus those that haven't (53% vs. 42%). In contrast, although 66% of companies that experienced fraud use digital payment alternatives, nearly 3 in 4 (73%) fraud-free companies use such methods.

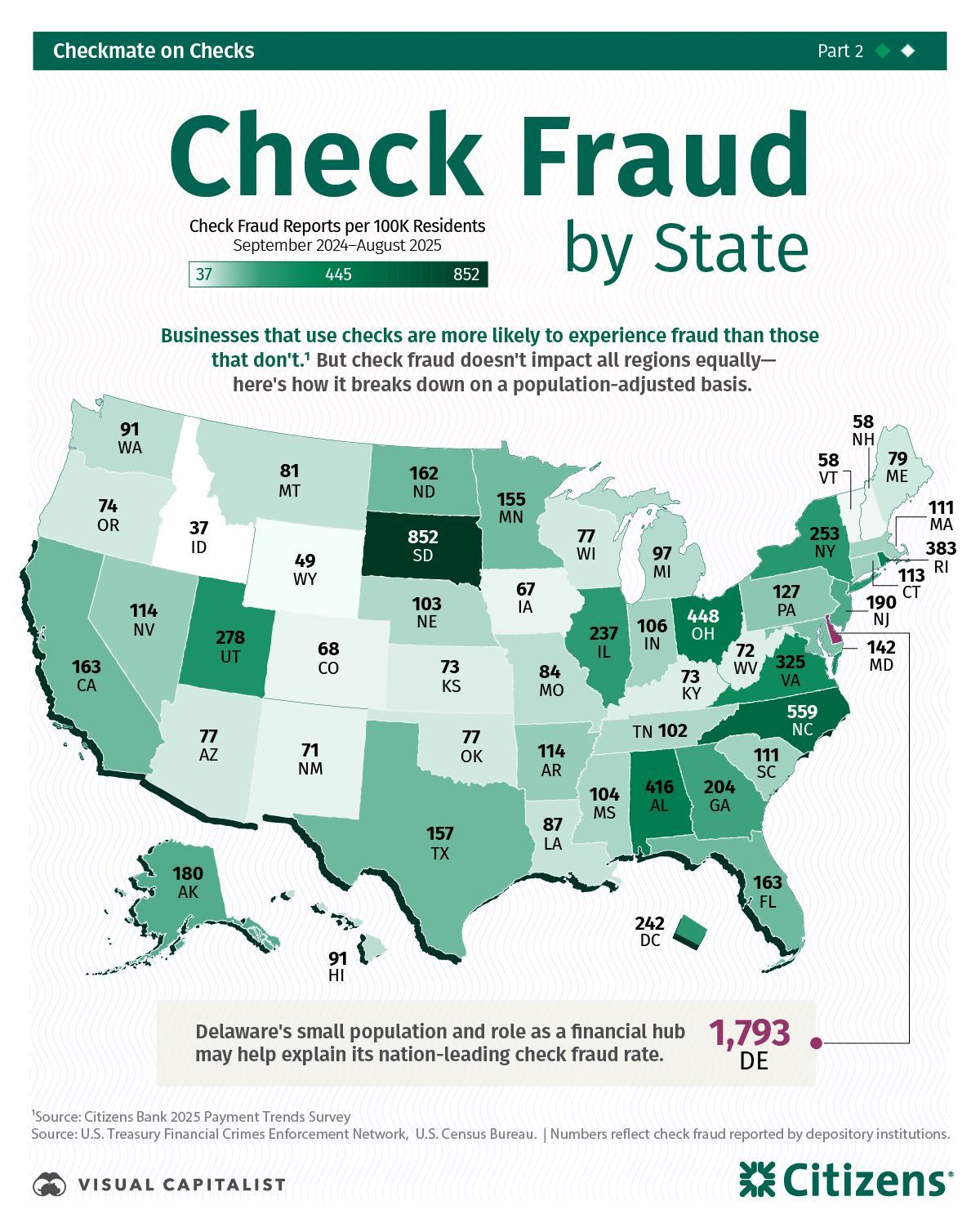

Check fraud rates vary by state and region

Check fraud varies widely by state and region within the U.S., due to characteristics unique to each location.

For example, with 1,816 check fraud reports per 100,000 residents, Delaware is by far the top U.S. state for reported check fraud on a per capita basis. Yet, there is strong evidence that Delaware's elevated rate is largely structural — not necessarily behavioral — stemming from its unique business and population characteristics.

There are several plausible reasons for Delaware's high per-capita rate of check fraud. First is the incorporation hub effect; given its business-friendly legal system and regulatory environment, Delaware has long been recognized as the premier U.S. financial hub for corporations. The state is home to over 2 million corporations — a figure twice that of its human population. Incidents of check fraud tied to these organizations are often reported under Delaware corporate or branch addresses, even when the underlying activity occurs elsewhere. This is because FinCEN assigns fraud activity at the state level based on either the subject or branch location.

Additionally, with just over a million people, Delaware ranks 45th out of the 50 states in population. Due to the small population denominator effect, even moderate increases in fraud report filings result in outsized per-capita values.

Finally, both the U.S. Postal Service's Office of the Inspector General (OIG) and FinCEN have reported strong increases nationally in "check washing," a fraud scheme where the scammer steals a check from the mail, chemically removes the payee and/or amount, and rewrites the check in their own name. With its proximity to major mail-processing hubs and high incorporation density, Delaware has higher-than-average exposure to such activity.

Check alternatives are more secure

A range of new digital payment tools can help companies mitigate fraud losses, and most companies say they intend to transition to all-digital payments at some point in the future.

Among those organizations that still use cash or checks, one third plan to shift to all-digital in the next year, while another 42% say it will be in the next two or three years. This makes sense, as transitioning to paper check alternatives will help your company meet customers' and suppliers' growing demands for security and convenience.

If you're planning to stick with checks for the immediate future, you do have several effective fraud mitigation tools at your disposal. These include using secure mailboxes or drop boxes for customer payments and implementing Positive Pay — a cash management service that matches checks presented for payment against a list of those the company has issued, flagging any discrepancies for review before payment.

Actions to consider

- Ask your vendors and suppliers how they prefer to be paid. Today, many suppliers prefer to receive payment through modern digital methods instead of paper checks. Digital payments are more convenient, faster and more secure than physical checks.

- Consider a transition to an all-digital future. More companies are exploring a migration to digital payments — and many are adopting new technologies and tools, including AI and embedded finance APIs. Assess your current payment ecosystem and decide what mix of methods makes the most sense for your organization.

- Layer your fraud-mitigation tools in a best-practices approach. Companies that report less fraud are more apt to use real-time fraud monitoring and AI for customer authentication. Keep close track of the best practices and implement them in a layered strategy to protect your organization from fraud.

Related topics

How companies can use new payment tools to optimize working capital

Virtual cards: simplifying supplier payments and strengthening partnerships

2025 Payment Trends

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

“Citizens” is the marketing name for the business of Citizens Financial Group, Inc. (“CFG”) and its subsidiaries. “Citizens Capital Markets & Advisory” is the marketing name for the investment banking, research, sales and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC (“CJMPS”), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE