Key takeaways

- Companies are increasingly concerned about the frequency of costly weather events and impacts to properties, operating assets, supply chains and insurance availability and cost.

- Business leaders are taking action to safeguard against financial costs, downtime and other business disruptions related to severe weather.

- Integrating severe weather into risk assessment and financial planning, proactively investing in equipment and site design and diversifying locations of operating assets and supply chain partners are ways companies can mitigate risk and increase resiliency.

From 2020-2024, the U.S. experienced an average of 23 severe weather events per year with losses over $1 billion each, significantly exceeding longer-term historical averages.1 Overall economic losses from natural disasters in the U.S. in 2024 reached $218 billion, twice the 2020-2024 average ($109 billion).2 While we often think of severe weather as a coastal issue, events span the U.S., impacting diverse geographies and communities. Over the past year, from Texas to Los Angeles to North Carolina, communities have endured losses that transcend mere numbers. Rebuilding livelihoods rooted in places that have long been home will take years.

For corporate clients, the need to proactively understand and plan for severe weather risk is critical. In addition to business disruption, downtime and costs, severe weather events drive increased insured losses (i.e., the portion of economic losses that are covered by insurance). Total insured losses rose 36% in 2024 to $113 billion, exceeding the average ($58 billion) and median ($45 billion) figures from 2000-2024.3 This trend is leading insurers to adjust practices, transferring more risk and cost to policyholders. When it comes to securing adequate insurance coverage to safeguard against weather-related costs, companies may face:

- Coverage gaps and fewer options for insurers

- Higher rates and deductibles

- Tighter terms and narrower coverage (such as exclusions of secondary perils)

- Property value implications

Lack of investment in resilience and risk mitigation in the short term may impact future insurability, leaving companies with fewer options for managing costs.

Banks and lenders are paying attention to these shifts, including heightened monitoring and execution of scenario analysis to better understand potential impacts on borrowers and opportunities to support.

Key actions and best practices for businesses

The transfer of risk and cost to businesses raise questions about resilience and financial stability. Severe weather impacts can lead to increased operational, credit and reputation risk due to the location of properties and supply chain partners and the lack of mitigation plans. In a recent survey conducted by Chubb, companies that have experienced a natural disaster reported moderate or significant impacts to operations (59%), brand (55%) and finances (51%), underscoring the need to take action now to mitigate key impacts.4

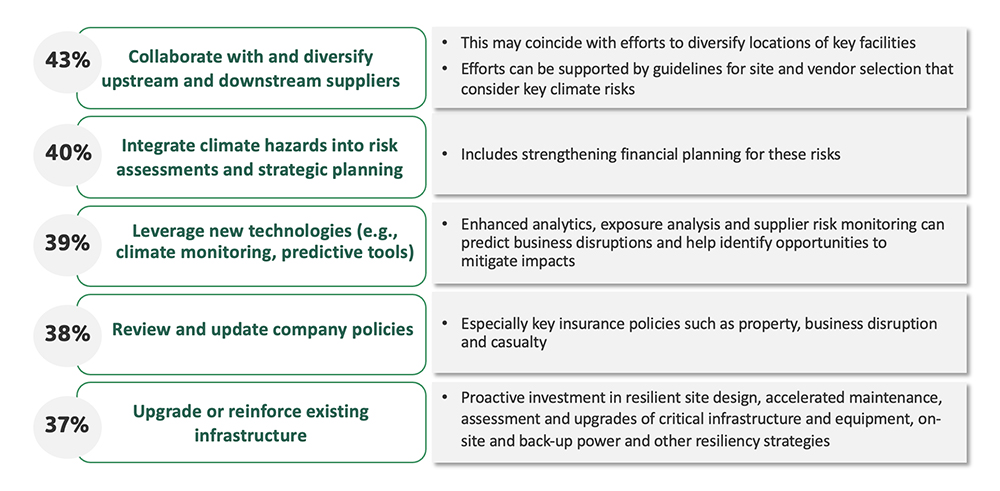

Sixty-one percent of business leaders surveyed on behalf of Citizens reported that they are increasingly concerned about severe weather risk to their business in the next 1-3 years. In the New England and tri-state area, which have experienced recent hurricanes, winter storms and flooding, that number increases to 67% and 68%, respectively.5 These leaders reported planning to take the following actions in the next 1-3 years to mitigate impacts and better position themselves to navigate financial costs, downtime and business disruption.

Finally, businesses should look for opportunities. Severe weather creates emerging market needs that companies can fill with differentiated products and solutions, such as back-up power solutions or weather resistant building materials that may generate new revenue via expansion opportunities.

Preparing your organization for severe weather risks

At Citizens, our Sustainable Finance Advisory team and platform of experts can work with clients and prospects to provide flexible, tailored financing and credit solutions that meet client needs related to severe weather. As banks monitor and seek to better understand how severe weather presents risks to companies, they are also seeking feedback on how to support their clients so they can proactively invest in mitigation and continue to thrive.

Related topics

Citizens 2026 M&A Outlook

As market conditions improve, the M&A upswing is poised to broaden in 2026. Discover what's behind this optimism in our survey of 400 company and PE firm dealmakers.

Higher fraud is the true cost of paper checks

Paper checks are fading fast. Discover how digital payments (RTP, ACH, virtual cards) offer speed, security, and cost savings.

The flow of capital into Gen AI

With significant capital flowing into AI, midsize businesses could see new opportunities for efficiency, cost reductions, and customer service. Learn more about potential implications for your business.

Ready to take the next step? Get in touch with our team.

All fields are required unless marked as "Optional".

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

1 NOAA National Centers for Environmental Information (NCEI) U.S. Billion-Dollar Weather and Climate Disasters (2025). Events tracked include droughts, floods, freeze events, severe storms, tropical cyclones, wildfires and winter storms.

2 Aon Catastrophe Institute: 2025 Climate and Catastrophe Insight

3 Aon Catastrophe Institute: 2025 Climate and Catastrophe Insight

4 Chubb Middle Market Indicator: 2025 Mid-Year Update

5 Citizens Middle Market Business Challenges Survey: C-level executives at 250 middle market U.S. businesses completed a web-based survey between January and February 2025

"Citizens" is the marketing name for the business of Citizens Financial Group, Inc. ("CFG") and its subsidiaries. "Citizens Capital Markets & Advisory" is the marketing name for the investment banking, research, sales, and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC ("CJMPS"), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS. (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

SECURITIES, INVESTMENTS AND INSURANCE PRODUCTS ARE SUBJECT TO RISK, INCLUDING PRINCIPAL AMOUNT INVESTED, AND ARE:

· NOT FDIC INSURED · NOT BANK GUARANTEED · NOT A DEPOSIT · NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY · MAY LOSE VALUE