By Devin Ryan, Head of Financial Technology Research, Citizens

Key takeaways

- As international regulatory frameworks become clearer, it's a good time to explore how stablecoins could play a role in your diversified payments ecosystem.

- Stablecoins offer some benefits to traditional payment methods, including faster settlements and lower costs.

- But businesses should not jump into the deep end of the pool; lingering regulatory uncertainty, counterparty risk and system integration friction call for cautious due diligence.

With around $300 billion in circulating float and $33 trillion in global transaction volume in the last year alone, stablecoin is no longer a niche asset class. Instead, it represents an increasingly vital component of financial infrastructure across trading, payments and treasury management.

Citizens Equity Research projects that stablecoin float will increase by a factor of 10x to nearly $3 trillion by 2030. A key driver of this growth will be the widespread adoption of stablecoin in payments, as more businesses use the technology in cross-border transactions and digital treasury operations.

For small-to-medium-sized enterprises (SMEs), stablecoins offer several potential benefits, including faster settlements and lower costs, along with relative stability as compared with other tokenized assets. Despite some lingering challenges around regulation, integration and practicality of use, stablecoins can serve as a complementary financial tool to traditional payment methods. It’s a good time to explore how stablecoins can potentially be deployed in your business.

2026 is an inflection point for stablecoins

Stablecoin issuance is currently dominated by two players, Tether and Circle. Yet, numerous banks, fintechs, payment processors, big tech firms and central banks are exploring entry into this market in a post-regulatory "land grab."

Bigger picture, stablecoin adoption is poised to serve as a steppingstone to the broader tokenization of financial and non-financial assets, with blockchains positioned to serve as a foundational technology in an increasingly digital economy.

While 95% of current activity is linked to trading, remittances and decentralized finance (DeFi), stablecoins will likely expand into mainstream payments, B2B settlements and tokenized asset infrastructure over the next few years. Regulatory moves such as the GENIUS Act (U.S.) and MiCA (EU), along with structural changes including Ethereum Layer-2 scaling and institutional integrations are accelerating this evolution.

Stablecoins explained

A stablecoin is a tokenized digital currency pegged 1:1 to a stable asset like the U.S. dollar (USD). As such, these instruments offer the speed, lower costs and programmability of blockchain technology while retaining the reliability and trust of fiat currency.

Stablecoins have unique attributes that distinguish them from other methods of payment and asset value storage, such as bank deposits, digital payment apps and cryptocurrencies. They can move faster than traditional payment rails like ACH and Fed wires, and at a lower cost than established pay networks.

Unlike cash and deposit accounts, every transaction is recorded on an electronic ledger, creating an immutable audit trail and unassailable proof of ownership. And because they are generally pegged to reliable, stable fiat currencies like USD, stablecoins are often less volatile than other cryptocurrencies.

These characteristics make stablecoins the first blockchain-enabled payment type that can serve as a reliable building block for businesses of all sizes, with the opportunity to make banking and treasury services more efficient and cost effective. And with emerging regulatory clarity in the U.S., Europe and Asia, a slew of new entrants, including banks, fintechs and big tech firms are poised to enter the sector.

An evolving regulatory climate for stablecoins

The regulatory landscape for stablecoins has been evolving rapidly. Globally, regulatory action has been focused on three non-negotiables: full reserve backing, clear redemption rights and vetted, supervised issuers.

The European Union opened the door with its enactment of the Markets in Crypto-Assets Regulation (MiCA), which is the world's first comprehensive, fully implemented cryptocurrency regulatory regime. Passed in 2023, the regulation establishes two classes of cryptocurrency: Asset-Referenced Tokens (ARTs), which track a basket of currencies, and E-Money Tokens (EMTs), which are pegged to a single fiat currency. EMTs are the closest analogue to U.S. stablecoins. MiCA takes a restrictive and cautious approach to crypto regulation, prioritizing financial stability and consumer protection over market growth.

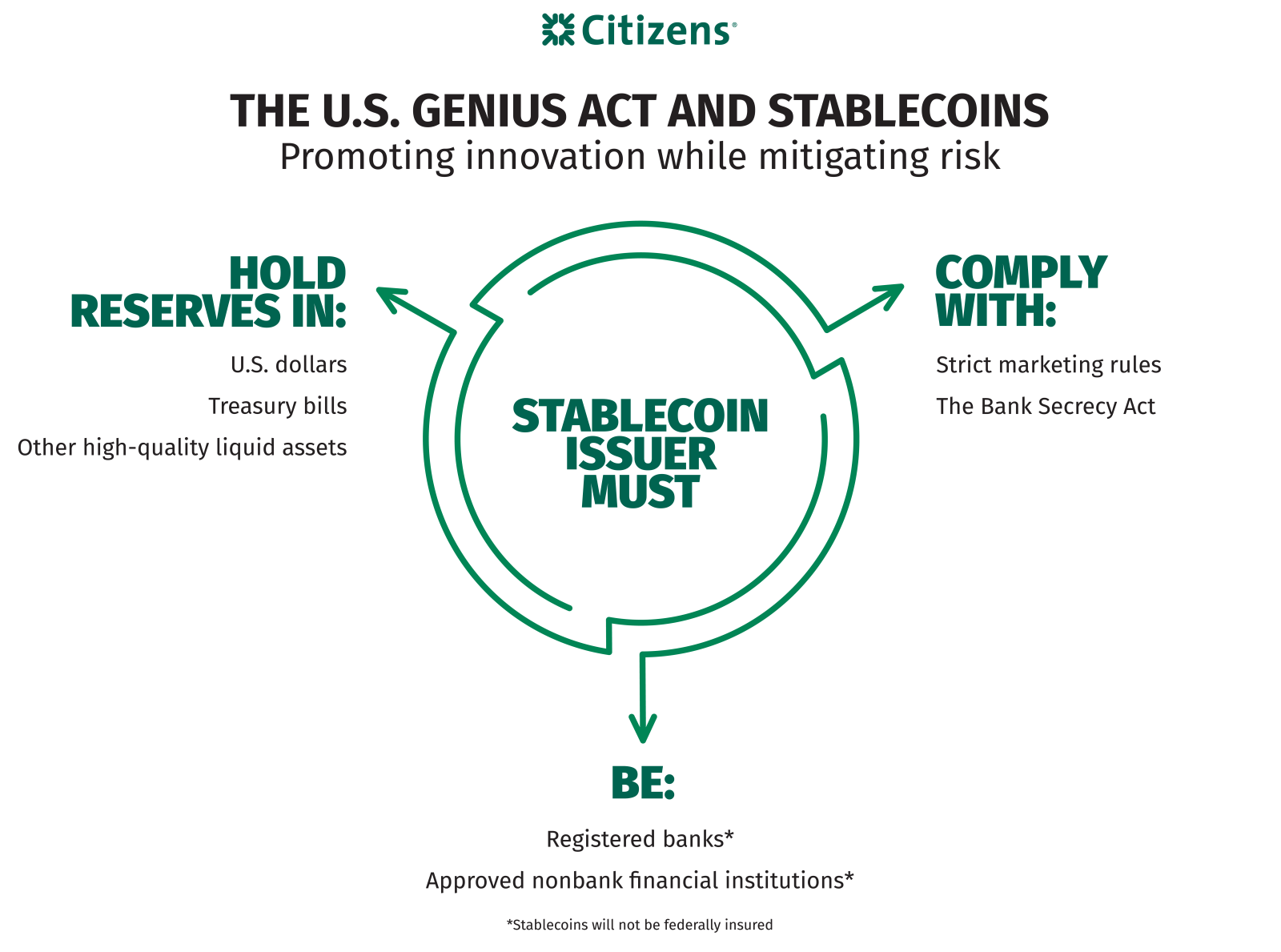

The U.S. joined the fray with the passage of the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act on July 18, 2025. As enacted, the GENIUS Act is "designed to promote innovation while mitigating risks to users and financial stability, ensuring stablecoins serve as a reliable medium of exchange." It requires stablecoin issuers to hold reserves in U.S. dollars, Treasury bills or other high-quality liquid assets, and to distribute monthly public disclosures. Only registered banks or approved nonbank financial institutions are allowed to issue stablecoins, but unlike traditional deposits, the coins will not be federally insured. The law also includes strict marketing rules and mandates compliance with the Bank Secrecy Act to combat money laundering.

The GENIUS Act will take effect on January 18, 2027, or 120 days after final regulations are issued, whichever comes first, with a July 18, 2028 deadline for full compliance with sales restrictions.

Other countries, including Singapore, Japan and the United Arab Emirates have issued their own stablecoin and/or payment token regulations. Each differs in its approach and priorities, but together they are helping to build an international regulatory framework that will reinforce the legitimacy of stablecoin and help establish a developing standard allowing them to scale across multiple geographies.

With much uncertainty surrounding the emerging regulatory regime, businesses should monitor the following over the next 12-24 months:

- Consolidation of regulatory frameworks across jurisdictions: Significant differences remain among regulations passed in the U.S., EU and Asia. It's important to keep close tabs on rule updates, especially for those businesses that operate in multiple geographies or frequently initiate cross-border payments.

- U.S. implementation of the GENIUS Act: The U.S. Treasury is engaged in active rulemaking to meet the requirements of the Act ahead of its January 2027 implementation deadline. Recent actions have included the Treasury's April 2026 proposal to implement the Act’s AML and sanctions provisions, with more to follow later this year.

- EU implementation of MiCA: In Europe, MiCA is already providing more structure around asset-referenced tokens and e-money tokens, but there is still active work on Level 2/3 measures, supervisory guidance and the interaction with PSD2 payment-services rules. For SMEs operating in Europe, this offers greater clarity than before, but the current legal framework still has holes.

- Accounting and tax treatment: In the U.S., the IRS still treats digital assets as property for federal income tax purposes. This means that paying with digital assets (including stablecoins) may trigger gain or loss recognition. Look for more clarity on this front from the Financial Accounting Standards Board (FASB) and the IRS in the near future.

The role of financial institutions in stablecoins

Under the GENIUS Act, federally insured depository institutions such as banks and credit unions will be permitted to issue stablecoins. However, they may only do so through a separate, regulated subsidiary of the institution. Such subsidiaries must be approved as a "permitted payment stablecoin issuer" (PPSI) by the institution's primary federal regulator.

Stablecoins issued by bank or credit union subsidiaries must meet certain safeguards, including:

- 1:1 reserve backing with high-quality liquid assets

- Limits on eligible reserve assets (short-duration, low-risk instruments)

- Segregation of reserves and restrictions on their use

- Regular disclosures, attestations and audits

The goal of these backstops is to minimize systematic risk and approximate the role and perceived safety of traditional deposit accounts.

It's important to note that stablecoins will not be federally insured by the FDIC or NCUA, like standard deposit accounts. Instead, they will be treated as a new category: regulated digital payment instruments.

Stablecoins as part of a diversified payment ecosystem

Stablecoins have several unique features that can benefit SMEs, most notably for use in payments and treasury management. First, compared with traditional rails like ACH or Fed wires, stablecoins' near-instant settlement capabilities can enable faster payments to suppliers. For businesses where every hour saved impacts profit margin, the improvement in cash flow and float can have a material effect.

Stablecoins also boast lower transaction costs than some traditional payment methods, particularly for cross-border transactions. Lower-margin businesses can avoid card network fees, as well as international wire transfer fees. Because they are built on the blockchain, stablecoins create an immutable transaction record, making it easier to track and verify payments, enhancing trust with vendors and suppliers. And because they are tied to a reliable currency like USD, stablecoins help preserve value and reduce price volatility for businesses with foreign dealings.

Alongside these benefits, SMEs should be cognizant of certain risks associated with stablecoin implementation. These include the aforementioned regulatory uncertainty, along with counterparty risk, and the challenge of integrating stablecoin within existing financial systems. Most SMEs today don’t operate within a crypto-native environment. Core business systems were designed for traditional payment rails, including ACH, card networks, and Fed wires. Stablecoin payment schemas require the establishment of digital wallet infrastructure, the use of middleware and APIs and the ability to quickly transfer crypto to fiat currency and vice-versa for liquidity purposes.

It's also important to note that in these early days, not all stablecoins are created equal. Before selecting a stablecoin for payments, make sure you understand the underlying currency, the issuer's reserve backing and any potential de-pegging risk. Even the most widely used stablecoins should be considered only after comprehensive due diligence.

3 Stablecoin use cases for SMEs

To help you prepare for the surge of new stablecoins coming to market, here are three practical ways SMEs can leverage these financial tools for commerce and payments:

- Enable faster, cheaper B2B payments: Despite its scale, the infrastructure supporting B2B commerce can be fragmented. Payments are often routed through correspondent banking networks, requiring multiple intermediaries and producing delays, foreign exchange (FX) friction and reconciliation complexity. Many cross-border payments still settle on T+2 or T+3 timeframes, and error resolution can add days. According to McKinsey estimates, over $100 billion in annual inefficiencies exist in global B2B payment workflows.

Stablecoins offer some enhancement through the enablement of instant settlement, programmable logic (e.g., escrow conditions, milestone payments) and unified cross-border rails. Additionally, stablecoin-based transactions can reduce traditional clearing delays and FX volatility when denominated in USD. - Protect against currency volatility: For businesses operating in jurisdictions with unstable currencies, such as those with high inflation and uncertain economies, holding funds in USD-backed stablecoins can offer comparative stability. This is especially useful for companies in sectors like import/export and international manufacturing, where stablecoins can serve as a useful hedge against disruptive swings in foreign exchange rates.

- Modernize e-commerce retail: Global e-commerce is projected to exceed $7 trillion in annual volume by 2030, and stablecoins are well-positioned to capture the fastest-growing niches within it.

Stablecoins can serve as an attractive complement to legacy card networks, because transactions settle instantly across global networks at lower cost. Merchants can reduce card processing overhead, and cross-border transactions can be settled in USD-equivalents with less FX risk. Furthermore, stablecoins enable programmable checkout logic, allowing retailers to embed loyalty, discounts, royalties or dynamic pricing directly into the transaction.

Getting started with stablecoins

For SMEs considering testing the stablecoin waters, it’s best to start with a single, well-defined use case. Conduct a strategic landscape analysis first, by asking questions like:

- Where do stablecoins intersect with our cash flow?

- Are our competitors or partners already experimenting with stablecoin?

- What benefits could we anticipate seeing by switching to stablecoin?

- What are the potential risks?

Once you've identified a practical test case, begin implementing your plan, making sure to follow these important steps:

- Choose a safe, reputable stablecoin. Certain stablecoins have been on the market for several years, providing established options. Alternatively, you can choose to wait until additional stablecoin options are introduced.

- Evaluate available networks. Choose a reliable, vetted network that offers the right mix of speed, cost and security to meet your requirements.

- Treat it like a pilot program. Limit your exposure by making a modest financial investment to start. Use a separate digital wallet or deposit account to house your stablecoins, and limit usage to a single vendor or payment channel.

- Build an internal control foundation. To ensure security, put a few practical guardrails in place. Best practices include requiring dual approval for all transactions, recording all activity in an audit-ready transaction log and using multi-factor authentication to ensure secure, authorized access.

- Expand only once the pilot proves value. Define what will constitute "success" in your stablecoin project. Only once you reach this goal should you expand into additional vendors, geographies and payment workflows.

Where stablecoins fit in the future of payments

For SMEs, the stablecoin promise is at last coming to fruition. No longer simply a niche investment asset, stablecoins present real-world advantages that can translate to faster processing, lower costs and more accurate audit tracking. As new regulations bring clarity and legitimacy to the stablecoin ecosystem, its standing as a compelling complement to existing rails for use cases including cash management, payments and cross-border settlement is being realized. The time has arrived for businesses to explore the potential of this financial tool as part of a diversified Treasury function.

Citizens is actively monitoring stablecoin and this emerging payment space. Connect with our Commercial Banking team to discuss what business leaders should be watching for next.

Glossary:

| Blockchain | A shared digital ledger that records transactions permanently and transparently, allowing payments to be tracked and verified without a central intermediary. |

| Counterparty Risk | The risk that one party in a transaction, such as a payment token issuer or service provider, fails to meet its obligations. |

| Cross-Border Payments | Cross‑border payments are financial transactions in which funds are transferred between individuals or businesses located in different countries, typically involving multiple financial institutions and currencies. |

| De-Pegging Risk | The risk that a digital payment token loses its fixed relationship to its underlying currency, causing its value to fluctuate. |

| Digital Wallet | A software-based account used to store, send and receive digital assets such as blockchain-based payment tokens. |

| GENIUS Act | The GENIUS Act is a U.S. federal law that establishes a comprehensive regulatory framework for the issuance, backing, supervision and oversight of payment stablecoins in the United States. |

| MiCA (Markets in Crypto‑Assets Regulation) | MiCA is the European Union's unified regulatory framework governing the issuance, offering, and provision of services for crypto‑assets, including stablecoins, across all EU member states. |

| Fiat Currency | Government-issued money such as the U.S. dollar that is not backed by a physical commodity but by government authority. |

| Payment Rails | Underlying networks and systems such as ACH, wire transfers and card networks that move money between parties. |

| Reserve Backing | Assets (such as cash or short-term U.S. Treasury securities) held by an issuer to ensure a digital payment token can be redeemed at its stated value. |

| Settlement | The process of completing a payment by transferring funds from payer to recipient; blockchain-based payments can settle nearly instantly. |

| Stablecoin Issuer | A stablecoin issuer is the entity responsible for creating, redeeming and maintaining a stablecoin’s value by managing the reserves or mechanisms that back it. |

| Tokenization | The process of representing a real-world asset in digital form on a blockchain so it can be transferred electronically. |

Related topics

What treasurers need to know about payment fraud in an increasingly digital world

Learn the latest digital payment fraud risks and how CFOs and treasurers can protect their organizations from ransomware, check fraud, and AI driven scams.

2026 AI trends in financial management

The rise of Agentic AI accelerates adoption and investment momentum.

Higher fraud is the true cost of paper checks

Paper checks are fading fast. Discover how digital payments (RTP, ACH, virtual cards) offer speed, security, and cost savings

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

"Citizens" is the marketing name for the business of Citizens Financial Group, Inc. ("CFG") and its subsidiaries. "Citizens Capital Markets & Advisory" is the marketing name for the investment banking, research, sales, and trading activities of our institutional broker-dealer, Citizens JMP Securities, LLC ("CJMPS"), Member FINRA and SIPC (See FINRA BrokerCheck and SIPC.org). Securities products and services are offered to institutional clients through CJMPS. (CJMPS disclosures and CJMP Form CRS). Banking products and services are offered through Citizens Bank, N.A., Member FDIC.

Securities and investment products are subject to risk, including principal amount invested and are: NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE