How to save money when using a HELOC for debt consolidation

Key takeaways

- A home equity line of credit (HELOC) is a type loan that allows you to borrow against the equity you have in your home.

- Consider the pros and cons of a HELOC before determining if it makes sense for you.

- You could save money by consolidating credit card debt, personal loans and medical debt with a HELOC.

If you are currently trying to pay off debt, you're not alone. Nearly 54 million adults in the U.S. have been in debt for a year or longer. With inflation and high interest rates, you may find it difficult to keep up with monthly payments alongside groceries, utilities, insurance and other necessities.

Taking advantage of the equity in your home might be a solution. Using a home equity line of credit (HELOC) to pay off high-interest credit cards and personal loans could help you save on interest, lower your monthly payments and simplify your finances.

What is a HELOC?

A home equity line of credit (HELOC) is a highly flexible loan that allows you to borrow against the equity you have in your home. Unlike a personal loan or home equity loan where you receive a lump sum and then are required to make monthly payments on the full amount, HELOCs are more like credit cards in how they work. They are revolving lines of credit, based on the available equity in your home, that allow you to borrow money when you need it and only pay interest on the money you draw from the line.

You can draw available credit from the line during the HELOC draw period: which is typically 10 years. You have the option of making interest-only payments during this period, or you can make payments toward both the principal and interest.

At the end of the draw period, the repayment period begins. During this time, you're no longer able to draw on the line and you're required to pay both principal and interest on the amount borrowed. The repayment period typically lasts 15 years, which could lend itself to more manageable monthly payments than shorter-term loans.

HELOCs typically have variable interest rates, which means the annual percentage rate (APR) goes down as interest rates drop, and increases should interest rates rise. Some HELOC lenders pass along closing costs to the borrower, which can range from a few hundred dollars to 2-5% of the borrowed amount. However, when applying for a HELOC from Citizens through our Citizens FastLine process, there are no origination fees or closing costs.†

Pros of using a HELOC for debt consolidation

With a HELOC, you could leverage the equity in your home to tackle your debts, possibly at a more favorable interest rate. You can also use a HELOC to streamline your finances into one monthly payment to help you avoid missed payments on your other bills.

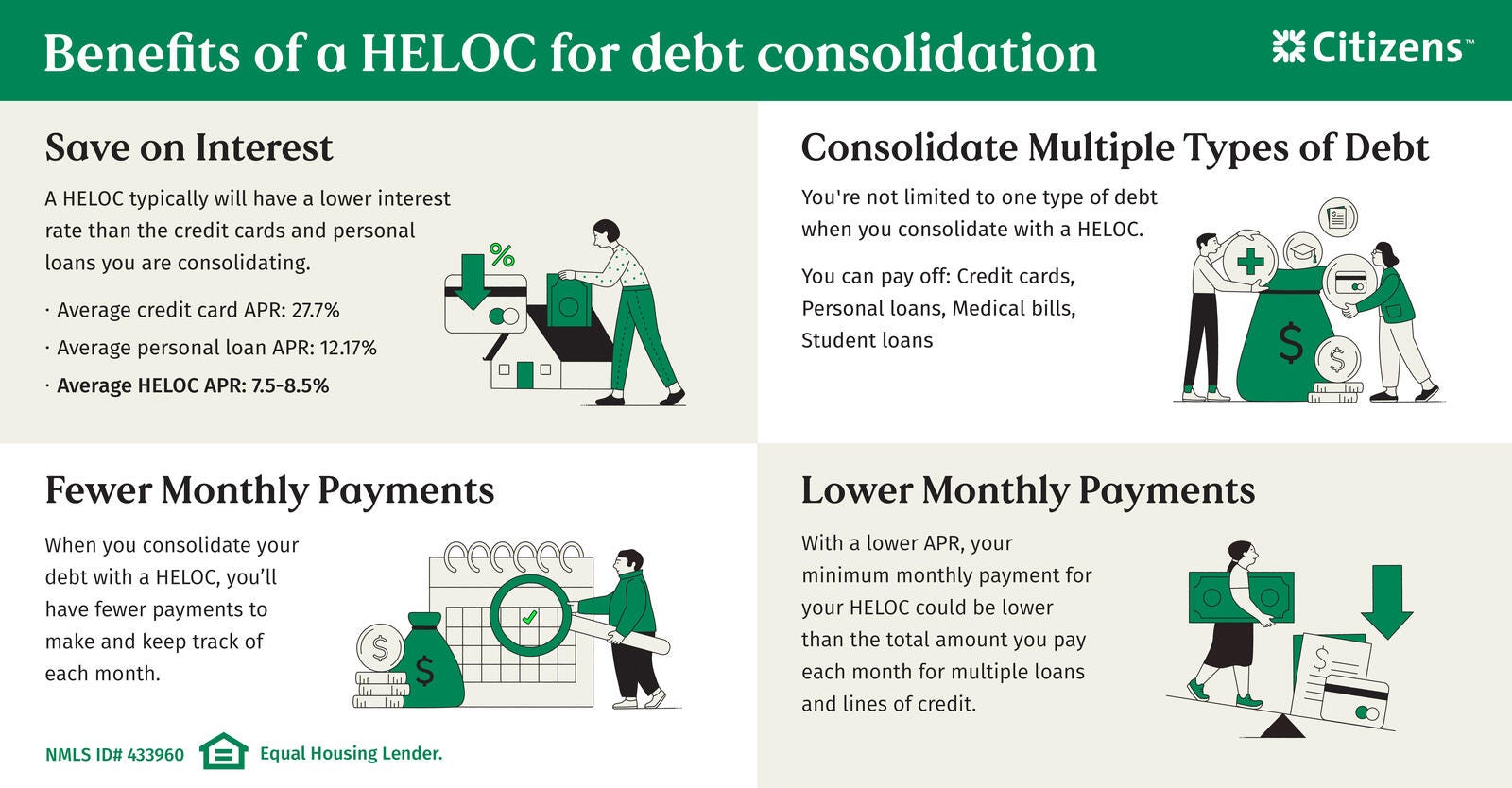

Save on interest

Credit cards typically have high interest rates, which make it hard for many to repay their debts. The average credit card debt in the U.S. is $6,500 per person with an average APR of 27.70%.

High interest is also a problem with personal loans. The average personal loan debt in the U.S. is $11,458, with an average APR of 12.17%. Although personal loans have lower interest rates than credit cards, their rates are higher than HELOCs because they are unsecured.

Compared to credit cards and personal loans, HELOCs have more favorable interest rates. The average HELOC rate is only 7.50-8.50% APR. They have such low rates because they are backed by the equity in your home.

Streamline monthly payments

Having multiple debts mean keeping up with multiple due dates each month. The more bills you have, the easier it is to accidentally miss a payment. If you consolidate your debt with a HELOC, you could have one convenient payment each month.

Lower monthly payments

With a lower APR, consolidating your debts with a HELOC can translate to lower monthly payments. Or, if you budget the same amount toward paying bills every month, you could pay down your principal balance more quickly.

Cons of using a HELOC for debt consolidation

- You must be a homeowner to take out a HELOC, which means they won't work for renters.

- You must have sufficient equity in your home to qualify. Most lenders require that all combined loans against the property do not exceed 80-85% of the property's current value.

- The closing costs will affect how much you can save by consolidating. For smaller debts, the closing costs may be more than the potential savings. This isn’t a factor with a HELOC from Citizens because there are no closing costs.†

- Your home is used as collateral. If you are unable to repay your HELOC, it could result in a home foreclosure. Also, if you need to sell, you will be required to immediately pay off the HELOC in full.

As of 8/15/2025

As of 8/15/2025

An example of using a HELOC for debt consolidation

To get an idea of how much you could save by consolidating your debts with a HELOC, consider the following example:

Henry has $15,500 of credit card debt with a 28% APR and personal loan debt of $25,525 with a 14% APR.

Assuming the principal remains unchanged, and Henry makes monthly credit card payments covering interest plus 3% of the $15,500 balance, his monthly credit card payments would be approximately $465. Assuming the term of Henry's personal loan is 5 years, he could expect monthly payments of about $594. Meaning every month, Henry's paying $1,059 towards his credit card and personal loan debt.

If he transfers the $41,025 debt to a HELOC with a variable APR of 8.00%, his minimum monthly payment (i.e. interest-only) would be $273.50 a month. This potential $785.50 savings in monthly payments can be attributed to both the lower interest rate of the HELOC as well as the ability to stretch the payments out over a longer period of time compared to the 5 year term of the personal loan.

If you're curious to see how much you personally can save each month with a HELOC, check out Citizens' HELOC Debt Consolidation Calculator.

What kind of debt can you consolidate with a HELOC?

HELOCs can be used to consolidate different kinds of debt. Some of the most common include credit cards, personal loans and medical bills.

Credit cards

If you consolidate your credit card debts with a HELOC, you could have a single monthly payment instead of having to keep up with multiple payments. A HELOC offers a lower interest rate, which could lower your monthly payment.

Personal loans

Taking out multiple personal loans for different expenses can be difficult to keep up with. Because they typically don't require collateral, personal loans often have higher interest rates than home equity loans or HELOCs.

Consolidating two or more personal loans with a single HELOC could help you save on interest, give you more time to repay your debt, and allow you to borrow more for the things you need. It helps you simplify your finances, which makes budgeting easier.

What to know when applying for a HELOC

If you're planning to apply for a HELOC, make sure you're prepared. Here's what you'll need to consider as you begin the process:

- Know your borrowing power: Most lenders prefer borrowers to maintain 20% of their home equity. To estimate the line size that may be available to you, multiply your home's current value by 80% (this is the maximum combined loan-to-value, or CLTV, most lenders allow), then subtract your current mortgage balance from that number. The result is your available equity. Lenders will also consider your income and overall debt-to-income (DTI) ratio to determine how much you can borrow.

- Understand any closing costs or fees: Not all lenders require closing costs, and annual fees differ from lender to lender. Consider shopping for lenders who waive these costs or those who offer relationship benefits to existing customers.

- Ready the information you'll need to share: To present you with a HELOC offer, lenders will need to run a credit check, understand your annual income, and whether you plan to apply on your own or with a co-applicant, among other details.

Simplify debt repayment

Are you ready to consolidate your high-interest debt with a HELOC? Citizens is here to help.

With Citizens FastLine® get your HELOC rate in minutes with no commitment and no impact to your credit score.

Don't let high-interest debt hold you back — apply for a HELOC with Citizens today and take the first step toward simplifying your finances.

Related topics

What is a home equity line of credit? (HELOC)

What is a home equity line of credit? Learn all the ins and outs of a HELOC and what you can use one for.

9 ideas for eco-friendly home improvements using a HELOC

Discover our top 9 eco-friendly home renovation projects and the benefits of using a HELOC to finance your upgrades.

How to use home equity: Five smart things to do with a home equity line of credit (HELOC)

What can you do with the equity in your home? Discover what you can use a HELOC to pay for.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Home Equity Lines of Credit are offered and originated by Citizens Bank, N.A. (NMLS ID# 433960). All loans are subject to approval.

† For additional information, please click the † symbols throughout this page to view our home equity line of credit disclosures.

Disclaimer: The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.