Wealth strategies in PE/VC: Planning across the career arc

By Rick Gordon, Managing Director, BG Wealth Advisors, a part of Citizens Private Wealth

Key takeaways

- Wealth strategies for PE/VC professionals must evolve along their career arc to address shifting liquidity, tax exposure, and risk profiles.

- Early-career partners benefit from resilience-focused planning such as cash flow modeling, risk management, and foundational tax strategies. Established partners prioritize complexity management and legacy design.

- Dynamic, stage-specific liquidity solutions and tax timing strategies are essential to optimize balance sheets and align wealth planning with long-term goals.

From the first capital call to the final distribution, every partner's career in PE/VC is unique. A junior partner rising in skill but hampered by liquidity constraints and lifestyle shifts faces very different planning considerations than a senior partner who has ample liquidity and is more focused on the appropriate steps for succession planning and generational wealth transfer.

While wealth planning conversations often aim to be personalized, planning for PE/VC clients can benefit from a more explicit recognition of these career-stage distinctions. Tailoring advice to the evolving risks, capital call commitments, tax strategies, and liquidity needs at each career phase ensures that planning and investment recommendations meet PE/VC professionals where they are in their career arc.

Why the career arc matters in PE/VC planning

Private equity and venture capital careers rarely follow a straight path. Compensation structures change, liquidity comes and goes unpredictably, and exposure to concentrated risk shifts as partners advance. A wealth strategy that works early in a career may become outdated as priorities shift.

Static planning frameworks can lead to mismatches between cash flow and commitments, and may cause professionals to miss key opportunities, such as capturing early tax advantages, managing lifestyle risk mid-career, or building effective legacy structures later on.

The increasing complexity of the tax return is usually a clear indicator of a change in career stages, and planning and execution must adapt as exposures to funds grow and K-1s accumulate. Early-career partners often face real pressures, both cultural and economic, to commit to larger funds, participate in no-fee or no-carry opportunities, and secure meaningful carry allocations. These commitments build economic exposure but frequently outpace liquidity, limiting access to optimization strategies.

Later in the career, tax exposure typically grows substantially, but a more robust balance sheet opens the door to planning resources and techniques such as mortgage interest tracing, charitable planning, and Pass-through entity tax (PTET) elections.

Because of these shifts, wealth strategies need to evolve alongside the partner’s career. To illustrate why stage-specific planning is critical, we’ll explore how the needs of an early-career partner facing liquidity pressure differ from those of a seasoned general partnership preparing for succession.

Two planning profiles: Illustrating the divergence

Placing two career stages side by side, early-career and established, reveals just how sharply planning considerations diverge. Each stage presents its own set of constraints, priorities, and opportunities, requiring distinct approaches to wealth management and personalized private banking strategies.

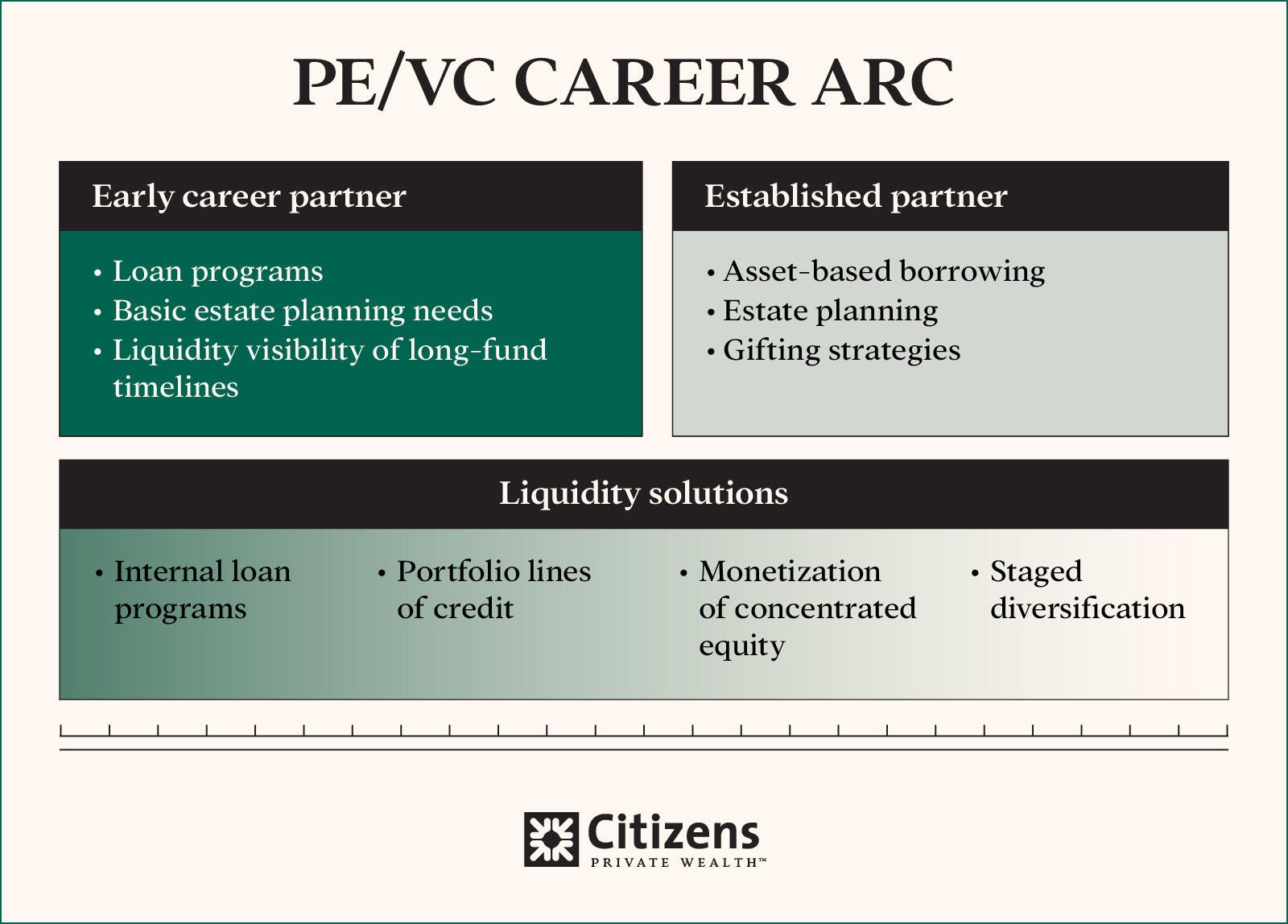

Early-career partner: Building resilience amid constraints

At the outset, partners often face a paradoxical mix of high earnings potential and limited financial flexibility. Compensation is typically skewed toward long-dated equity, while cash flow is stretched thin by increased fund capital commitments and rising lifestyle costs (buying a first home, building a family, etc.). Internal loan programs may help bridge the gap, but they also introduce leverage risk at a time when liquidity is scarce.

For these professionals, planning often touches on optimizing accumulated wealth, but the emphasis should be on protecting against downside and building a resilient foundation. Thoughtful cash flow modeling can prevent commitments from outpacing capacity, while risk management must address both portfolio concentration and behavioral tendencies that can lead to overextension. Early-stage tax mitigation strategies, such as use of municipal bonds, tax loss harvesting strategies, or leveraging Qualified Small Business Stock (QSBS) rules, can lay the groundwork for future efficiency. At the same time, basic but durable estate and insurance structures provide essential protection while wealth is still fragile.

Established partner: Managing complexity and designing legacy

By contrast, the established partner has moved beyond the cash flow juggling act into an environment defined by abundance and complexity. Years of distributions and carried interest may have created significant wealth, often in the form of concentrated holdings tied to funds or portfolio companies. While tax obligations can feel like a persistent drag, primarily due to the size and timing of quarterly estimated payments, they do not reflect inefficiency in the investment portfolio. In fact, PE/VC investors often enjoy structural advantages that make them highly tax-efficient compared to executives compensated primarily through W-2 income and stock options. Preferential treatment of carried interest, access to QSBS exclusions, PTET elections, and the ability to build large municipal bond portfolios all help offset the burden.

At this stage, planning shifts toward protecting what you’ve built and preparing for what’s next. Sophisticated estate planning strategies can help ensure efficient multigenerational wealth transfer. Strategic diversification — thoughtfully balancing legacy holdings with more liquid assets — can mitigate risk without undermining conviction in core investments.

For many, giving back becomes more meaningful and can also help with planning, while family governance and succession structures position the next generation to steward wealth responsibly.

Liquidity solutions across the arc

If career stage defines the context for planning, liquidity is often the lever that determines what’s possible at each point along the arc. For PE/VC professionals, access to liquidity is uneven and highly situational, shaped by capital calls, fund performance, tax obligations, and broader market cycles. Tailoring liquidity strategies to the stage of the career helps ensure that planning objectives remain relevant and actionable.

- Internal loan programs and accessing credit: For early-career partners, internal financing through the firm can provide critical breathing room when cash flow is tight but commitments are non-negotiable. These programs, while useful, require careful modeling to avoid leverage that outpaces realistic repayment capacity. A private banking and wealth management team can guide the merits of how to compare/combine partner loans, home loans, portfolio lines of credit, or other credit facilities to ensure considerations are personalized to each partner’s situation.

- Monetization of concentrated equity: As wealth accumulates, the challenge often shifts from scarcity to concentration. Monetization strategies, ranging from structured credit facilities to hedging arrangements, can unlock liquidity without forcing premature sales. This allows professionals to preserve upside potential while funding lifestyle needs, diversification, or philanthropic goals.

- Timing-based tax strategies: Across all career stages, liquidity decisions are deeply intertwined with tax exposure. Whether it’s harvesting capital losses early, bunching charitable contributions for tax efficiency, or using QSBS exclusions, careful sequencing can reduce drag and preserve more wealth for reinvestment or transfer.

- Staged diversification: Diversification need not be abrupt. A disciplined, staged approach — gradually rebalancing from concentrated positions into liquid and tax-efficient vehicles — can smooth transitions, mitigate market timing risk, and support long-term goals without disrupting professional identity tied to the firm.

The right liquidity solutions are rarely off-the-shelf. They demand customization that reflects the balance sheet, career stage, risk tolerance, and personal aspirations. Citizens Private Bank offers a range of liquidity solutions that can dovetail with firm-level liquidity timing, helping PE/VC professionals see the full picture and stay on track with their wealth plan.

Mindful through the arc: Cross-stage insight

The most effective planning recognizes that no stage exists in isolation. Each phase of the PE/VC career carries lessons for the next and exposes blind spots that can ripple forward if left unaddressed.

- Early-career foresight: Building with future complexity in mind helps ensure that today’s foundational decisions will hold up as wealth, family, and commitments expand.

- Established partner reflection: Revisiting early structures and choices can identify gaps or misalignments that have grown more consequential over time.

- Dynamic planning: Wealth strategy is an iterative process. It must evolve with the partner's professional priorities, personal goals, and market realities.

Wherever you are in the partner lifecycle, it's beneficial to check in and test whether your current strategy is allowing for true balance sheet optimization (i.e. tax offsets, leveraged gifting to heirs, etc.) while still reflecting your stage-specific needs. Engaging with a Citizens Private Wealth advisor can provide the perspective and solutions needed to align planning with the opportunities and risks inherent in a PE/VC career. Explore tailored strategies for private equity and venture capital professionals by visiting our PE/VC solutions page.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Citizens Private Wealth does not provide legal or tax advice. The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.

Citizens Wealth Management (in certain instances DBA Citizens Private Wealth) is a division of Citizens Bank, N.A. ("Citizens"). Securities, insurance, brokerage services, and investment advisory services offered by Citizens Securities, Inc. ("CSI"), a registered broker-dealer and SEC registered investment adviser - Member FINRA/SIPC. Investment advisory services may also be offered by Clarfeld Financial Advisors, LLC ("CFA"), an SEC registered investment adviser, or by unaffiliated members of FINRA and SIPC providing brokerage and custody services to CFA clients (see Form ADV for details). Insurance products may also be offered by Estate Preservation Services, LLC ("EPS") or an unaffiliated party. CSI, CFA and EPS are affiliates of Citizens. Banking products and trust services offered by Citizens.

SECURITIES, INVESTMENTS AND INSURANCE PRODUCTS ARE SUBJECT TO RISK, INCLUDING PRINCIPAL AMOUNT INVESTED, AND ARE:

· NOT FDIC INSURED · NOT BANK GUARANTEED · NOT A DEPOSIT · NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY · MAY LOSE VALUE