How much money do you need to retire?

By Jason R. Friday, CFP®, MPAS®, RICP®, CMFC, Head of Financial Planning | Citizens Wealth Management

Key takeaways

- There's no one-size-fits-all answer to how much you'll need to retire, but common benchmarks can help guide your retirement planning.

- Some strategies suggest saving 10 to 12 times your final working year's salary or using age-based multiples to track progress over time.

- Estimating how much you need to retire depends on various personal factors, including your current income, desired lifestyle and planned retirement age.

Retirement is one of life's most anticipated milestones. Whether your goals are traveling the world, spending more time with loved ones or exploring new hobbies, retirement offers the opportunity to shape your days around what matters most to you.

However, planning for retirement also means answering a crucial, and sometimes daunting, financial question: How much money do you need to retire? The answer depends on your lifestyle, goals and financial situation. With the right tools and guidance, you can identify that number and build a plan designed to help you reach it.

Methods to estimate how much you need to retire

There's no single retirement number that works for everyone. However, a couple of methods can help you get started:

Method 1: age-based benchmarks

A general rule of thumb is to have at least 10 to 12 times your annual income saved by age 67 if you plan to retire at this traditional retirement age. For instance, if you earn $150,000 per year, the retirement savings target would be between $1.5 and $1.8 million.

To help track your progress, consider these age-based benchmarks:

- By age 30: save 1x your annual income

- By age 40: save 3x your annual income

- By age 50: save 6x your annual income

- By age 60: save 8x your annual income

These benchmarks offer a quick way to assess whether you're on track, but they are just a starting point.

Method 2: the 25x rule

Following the 25x rule, you multiply your anticipated first-year retirement spending by 25. For example, if you plan to spend $60,000 in your first year of retirement, you should aim to save $1.5 million.

This method is based on the 4% rule, which suggests that you can withdraw 4% of your retirement portfolio in your first year of retirement. That amount can then be adjusted annually for inflation with a low probability of running out of money over a 30-year period. While the 4% rule provides a basic retirement income guideline, the 25x rule helps turn projected income needs into a retirement savings goal.

Limitations of retirement guidelines

Following any of these suggestions can help you get a quick estimate of your retirement goals. However, they don't take into consideration any of your personal circumstances. To create a more accurate retirement plan, you'll need to account for your personal details, such as your anticipated retirement age, expenses and sources of income.

What affects how much you'll need to retire?

Consider the following key factors to help determine how much you need to save for retirement:

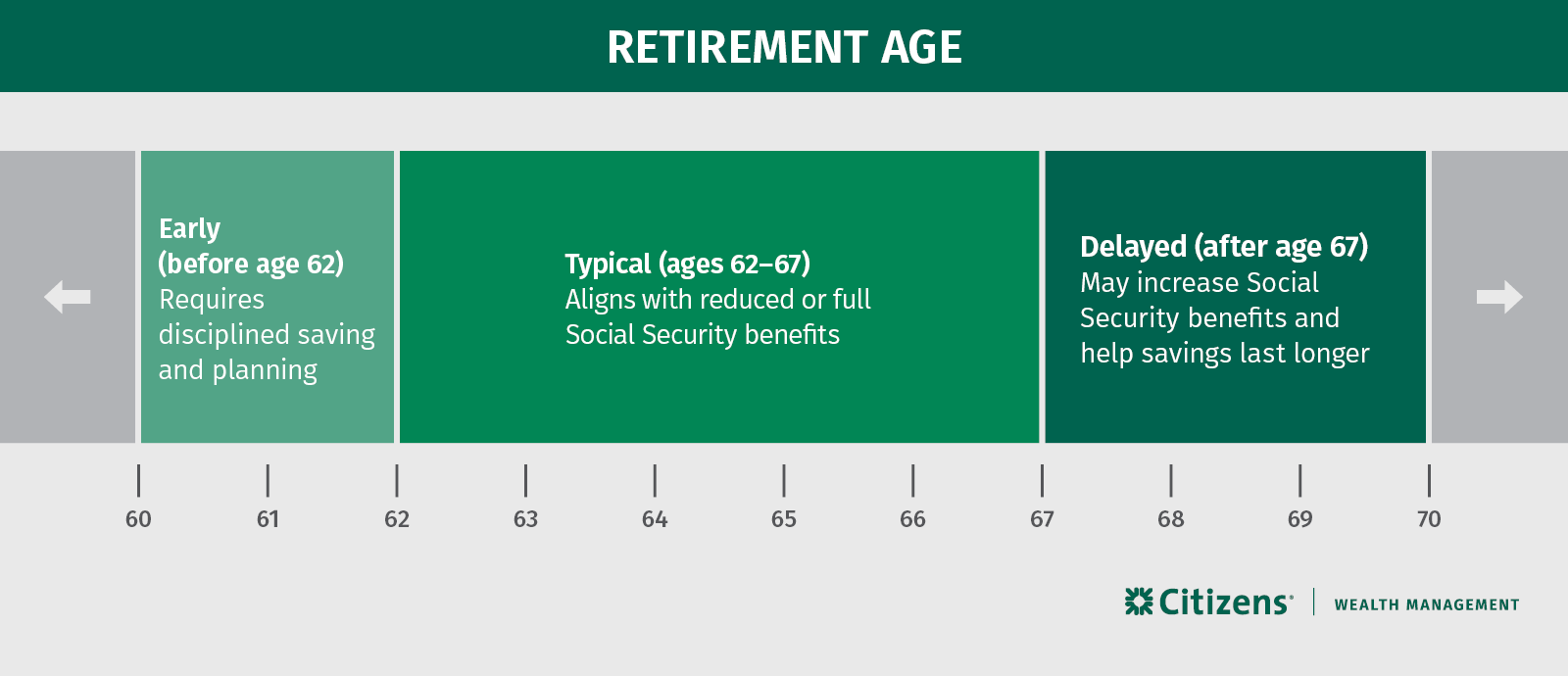

When do you plan to retire?

Your retirement age plays a key role in two important areas: your time horizon to be able to save for retirement and how long your savings need to last.

The life expectancy for a 65-year-old male is age 82. For a 65-year-old female, it's 85.1 However, these are averages. Half of retirees will live longer with many reaching their 90s or beyond. From a planning perspective, it's important to account for the possibility of a longer-than-expected retirement to ensure your savings last as long as you do.

In most cases, the earlier you retire, the more savings you'll need. What's considered an early retirement? A recent report found that while most workers plan to retire at age 65, the actual median retirement age is 62.2 Some even step away from their careers to retire in their 50s or earlier, a common desire for younger generations. In a recent Citizens' Next Gen survey, 39% of respondents said retiring early or comfortably represents financial success.3

On the other hand, delaying retirement can offer several financial advantages. Working longer could give you more time to save and may lead to larger Social Security benefits, especially if you are able to delay claiming until age 70. Postponing the start of retirement also may shorten the number of years you'll rely on your savings, which could reduce the total amount you'll need to fund retirement.

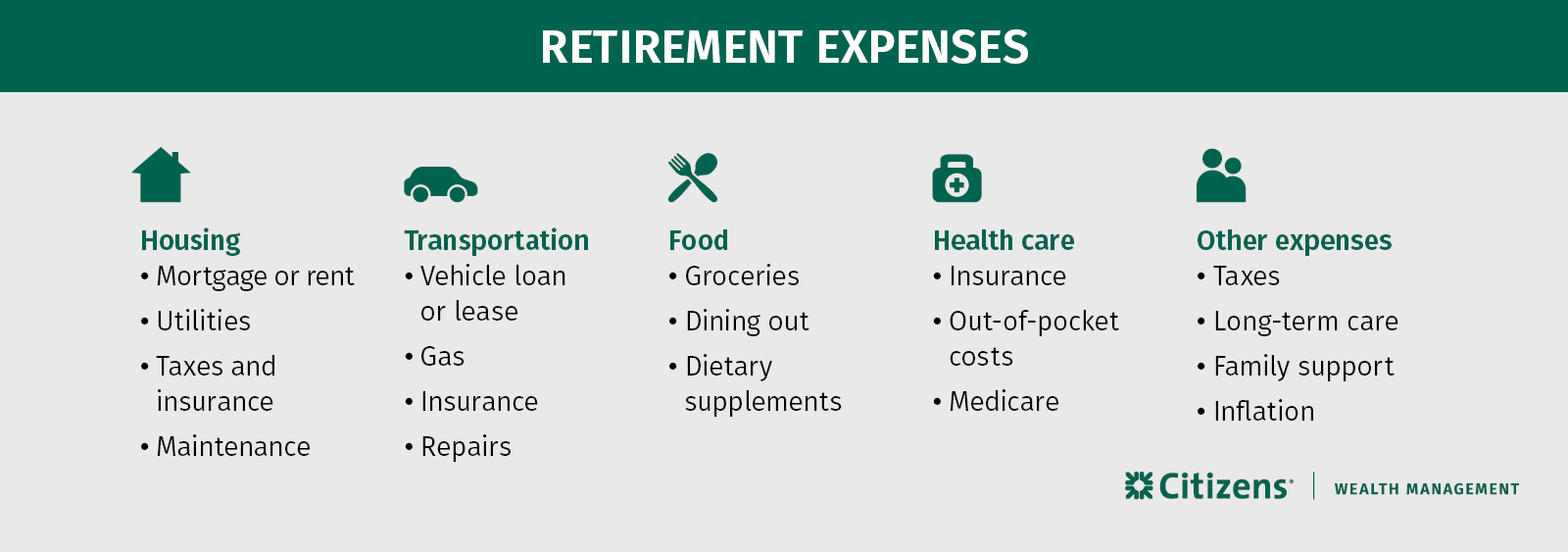

What expenses will you have in retirement?

A common starting point is to estimate that you'll need about 70% to 80% of your pre-retirement income to maintain your standard of living in retirement. For example, if you earn $150,000 annually while working, you might need between $105,000 to $120,000 as a starting point in retirement.

While this rule of thumb provides a quick estimate, the actual amount will vary based on your lifestyle and needs. To build a more accurate retirement budget, consider your unique expenses. Here are five categories to consider:

- Housing: This is the largest expense category for adults aged 65 and older. Even if your mortgage is paid off, property taxes, insurance, utilities and ongoing maintenance or repairs can still take up a meaningful portion of your budget.

- Transportation: At an average of $9,033 per year, transportation ranks as the second-largest expense for adults aged 65 and older.4 This includes fuel, insurance, maintenance, repairs and potential monthly payments on a new vehicle.

- Health care: Medicare helps, but it doesn't cover everything. Health care is another large annual expense at an average of $8,027 per year.5

- Food: Groceries and dining out typically cost around $7,714 per year for those 65 and older.6

- Other expenses: Think about discretionary spending like travel, entertainment and hobbies. You'll also want to account for insurance premiums, taxes on retirement income and the impact of inflation.

A solid retirement plan will consider all your current expenses and how they might change over time. By outlining these details, you can get a more accurate projection of your annual retirement costs and ensure your savings are aligned with your goals.

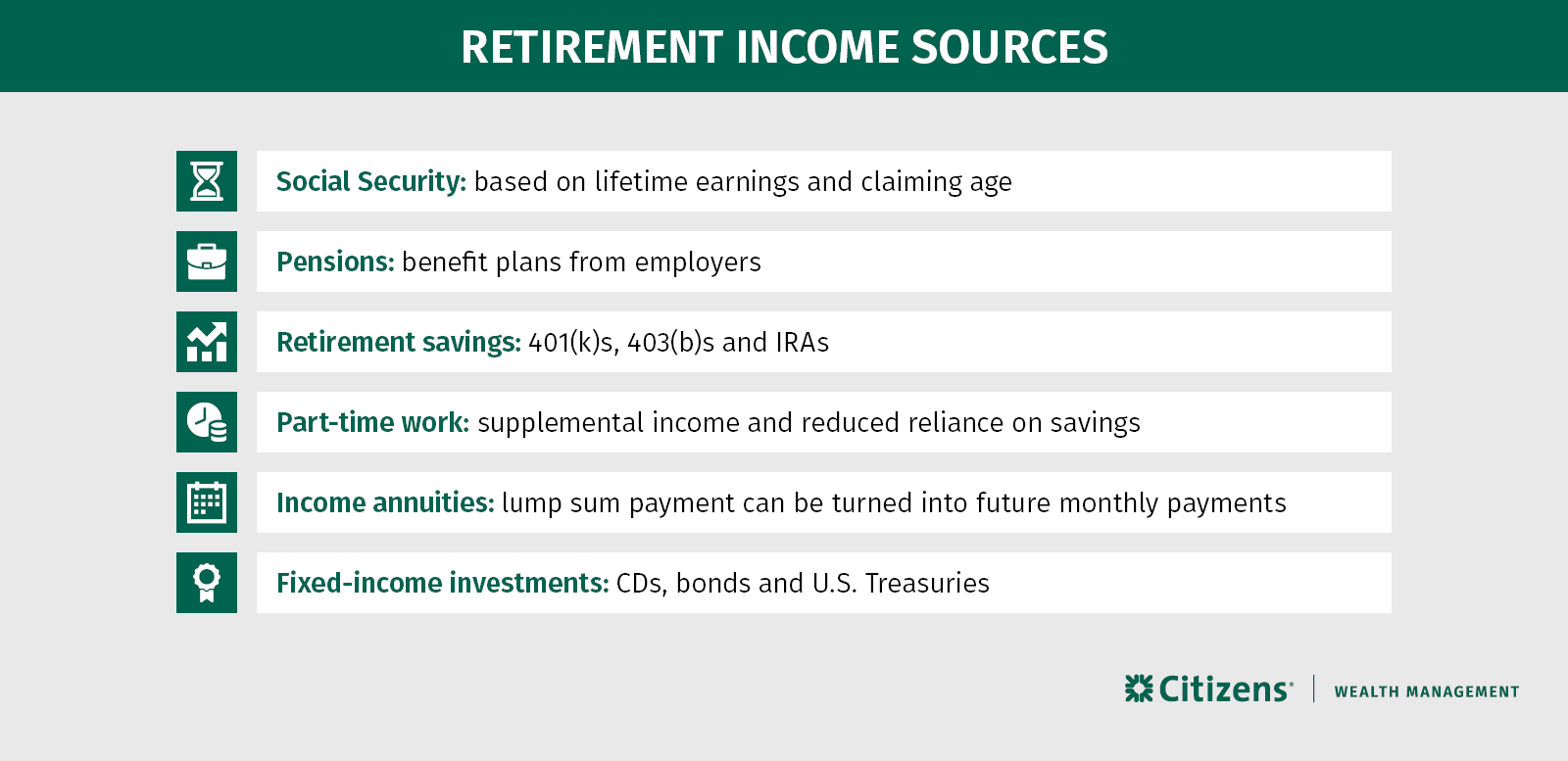

What income sources will you have in retirement?

Your retirement income will likely come from a mix of sources such as Social Security, pensions, retirement savings, income annuities and part-time work.

Understanding where your money will come from in retirement is key to knowing whether you're on track or if you need to increase your contributions to your retirement accounts. Ultimately, the more income you have from other sources, the less you'll need to withdraw from your retirement savings each year.

For example, if you estimate needing $100,000 per year in retirement income, and $36,000 will come from Social Security, the amount you'd need to withdraw from your savings is reduced to $64,000. Identifying all potential income sources now gives you a clearer picture of what you'll need to save and helps you make more informed decisions as retirement approaches.

How much should you be saving now?

As a starting point, consider a general benchmark of saving between 10% to 15% of your pre-tax income. The earlier you begin investing for retirement, the more time your accounts have to potentially grow through compounding returns. If you start later in your career, you may need to contribute more to stay on track with your goals.

A personalized retirement savings plan can be developed by considering factors such as your age, income, retirement goals and how much you've already set aside. Using this information, retirement calculators can provide a way to better understand what's needed to reach your goals. Here are two examples to help illustrate how they work.

Note that the following scenarios are for illustration purposes only and not representative of actual people or outcomes.

Example 1: on track for retirement goals

Monica, age 40, aims to retire at 65 and currently earns $125,000 per year, of which she consistently sets 15% aside for retirement. So far, she has accumulated $375,000. She estimates she will spend 75% of her final working year's salary while retired.

Using assumptions about average annual raises (3%), investment performance before and after retirement (7% and 4%, respectively), inflation (3%), Social Security (starting at age 65) and retirement length (30 years), our retirement calculator estimates that Monica could retire at 65 and her retirement savings would not run out until age 99.

Example 2: adjusting for a longer retirement

Steve is 30, earns $80,000 per year and has followed the suggestion of accumulating $80,000 for retirement to date. He has made similar assumptions as Monica, except he saves 10% per year for retirement, wants to retire at 62 and thinks he'll spend 80% of his final year's salary while retired.

Unlike Monica, however, Steve's current plan runs out of retirement savings at age 82. Since Steve wants his retirement savings to last for a minimum of 30 years, he'll need to change his plan if he wants to get there with some funds left over. One simple change Steve can make is to continue working until 66. Under this scenario, his retirement savings would last until age 94.

Create your personalized retirement plan

So how much money do you need to retire? The answer starts with creating a clear vision of what retirement looks like for you. Once you've defined your goals, you can begin to calculate the amount you'll need to reach them and build a strategy to help you progress toward it.

However, keep in mind that retirement planning can be complex. From navigating the transition into retirement to managing risks like sequence of returns, withdrawal rates, and longevity, there are many moving parts that can impact your retirement. While it can feel overwhelming, you don't have to navigate it alone.

A Citizens Wealth Advisor* can help you create a personalized retirement plan tailored to your financial situation and long-term goals. With thoughtful planning and professional guidance, you can move toward retirement with greater clarity and confidence.

Related topics

Top retirement risks and how to prepare for them

Learn how to prepare for common retirement risks to help secure your financial future.

Hidden retirement costs: 6 unexpected expenses for retirees

A strong retirement plan addresses both the obvious and often overlooked expenses that can cut into your retirement budget.

IRA vs. 401(k): What's the difference and how to choose one

Are you interested in saving for retirement but don't know where to get started? Learn the differences between IRAs and 401(k)s to help you choose the right path.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

1 Social Security Administration, "Period Life Table, 2022, as used in the 2025 Trustees Report"

2 Employee Benefit Research Institute/Greenwald Research, "2025 EBRI/Greenwald Retirement Confidence Survey Summary Report," April 2025

3 Citizens' Next Gen: The Future of Success Survey was conducted by Researchscape among 2,309 U.S. adults aged 18-34. The survey was fielded from August 29 to September 11, 2025, using an online survey. Data has been weighted. Weighting data is a statistical technique used to adjust survey data after it has been collected in order to improve the accuracy of survey estimates.

4 - 6 BLS, "Consumer Expenditure Surveys, Age of reference person," 2023

* Securities, Insurance Products and Investment Advisory Services offered through Citizens Wealth Management.

Disclaimer: Citizens Securities, Inc. and Clarfeld Financial Advisors, LLC do not provide legal or tax advice. The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.

Banking products are offered through Citizens Bank, N.A. ("CBNA"). For deposit products, Member FDIC.

Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the United States to Certified Financial Planner Board of Standards, Inc., which authorizes individuals who successfully complete the organization's initial and ongoing certification requirements to use the certification marks.

All investing involves risk, including the risk of loss of principal. Investment risk exists with equity, fixed income, and other marketable securities. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

Citizens Wealth Management (in certain instances DBA Citizens Private Wealth) is a division of Citizens Bank, N.A. ("Citizens"). Securities, insurance, brokerage services, and investment advisory services offered by Citizens Securities, Inc. ("CSI"), a registered broker-dealer and SEC registered investment adviser - Member FINRA/SIPC. Investment advisory services may also be offered by Clarfeld Financial Advisors, LLC ("CFA"), an SEC registered investment adviser, or by unaffiliated members of FINRA and SIPC providing brokerage and custody services to CFA clients (see Form ADV for details). Insurance products may also be offered by Estate Preservation Services, LLC ("EPS") or an unaffiliated party. CSI, CFA and EPS are affiliates of Citizens. Banking products and trust services offered by Citizens.

SECURITIES, INVESTMENTS AND INSURANCE PRODUCTS ARE SUBJECT TO RISK, INCLUDING PRINCIPAL AMOUNT INVESTED, AND ARE:

· NOT FDIC INSURED · NOT BANK GUARANTEED · NOT A DEPOSIT · NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY · MAY LOSE VALUE