Should you make student loan payments while in college? Understanding repayment options

Key takeaways

- Lenders may offer different student loan repayment plan options, such as deferred, interest-only, immediate, or fixed repayment.

- Making payments on your student loans while you're in school could help decrease the amount of total interest you end up paying on the loan.

- It's important to choose the repayment plan that works best for you and your family based on your unique financial situation.

With the rising cost of college, minimizing student loan debt has become a priority for college-bound students. While student loans are a reality for many students, it's important to plan carefully and understand how much you'll owe and what your finances will look like after graduation.

One way you can try to minimize your post-graduation debt is by making student loan payments while you're in school. When you make your payments on time, it could also help build up your credit during college. Read on to go over repayment options, how repayment works, and the impact of making payments on your loans sooner rather than later.

What are your student loan repayment options?

Depending on the type of loan and the lender, you may have several repayment options that you can choose from. While every lender is unique and will have their own repayment plans, here are some common ones:

- Deferred repayment: No loan payments while in school or during the grace period (typically six months after you graduate, leave school, or drop below half-time enrollment). After the grace period, you make full (principal and interest) monthly payments.

- Interest-only repayment: Pay only the interest each month while you're still in school and during the grace period, followed by full monthly payments.

- Immediate repayment: Make full monthly payments which begin while you're in school.

- Fixed repayment: Choose a fixed amount to pay while you're in school and during the grace period, followed by full monthly payments.

What impact can in-school payments have on student loans?

Deferred repayment may sound great because you don't need to pay while you're in college, but making payments while you're in school could help you lower your total loan cost in the long run.

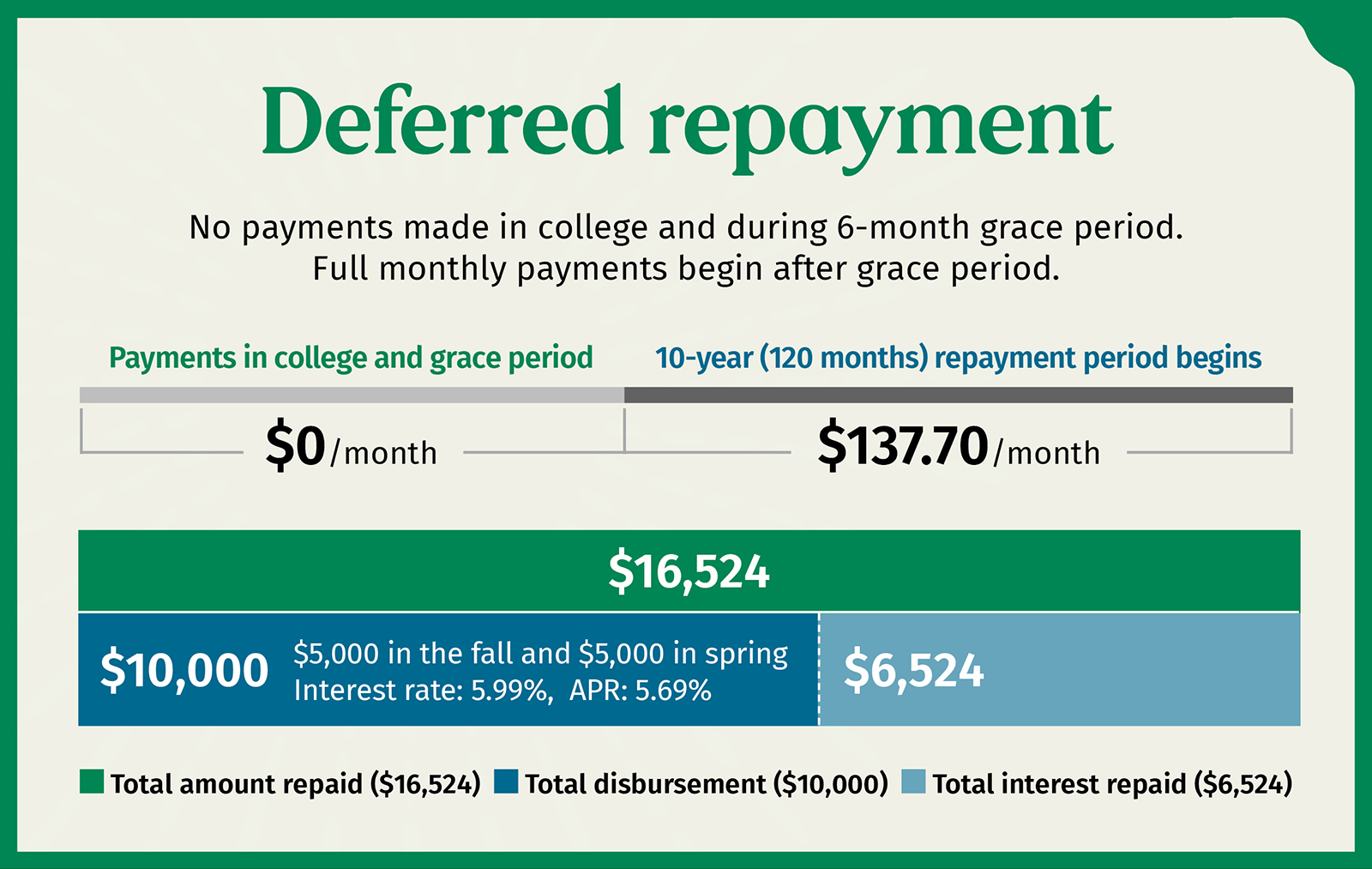

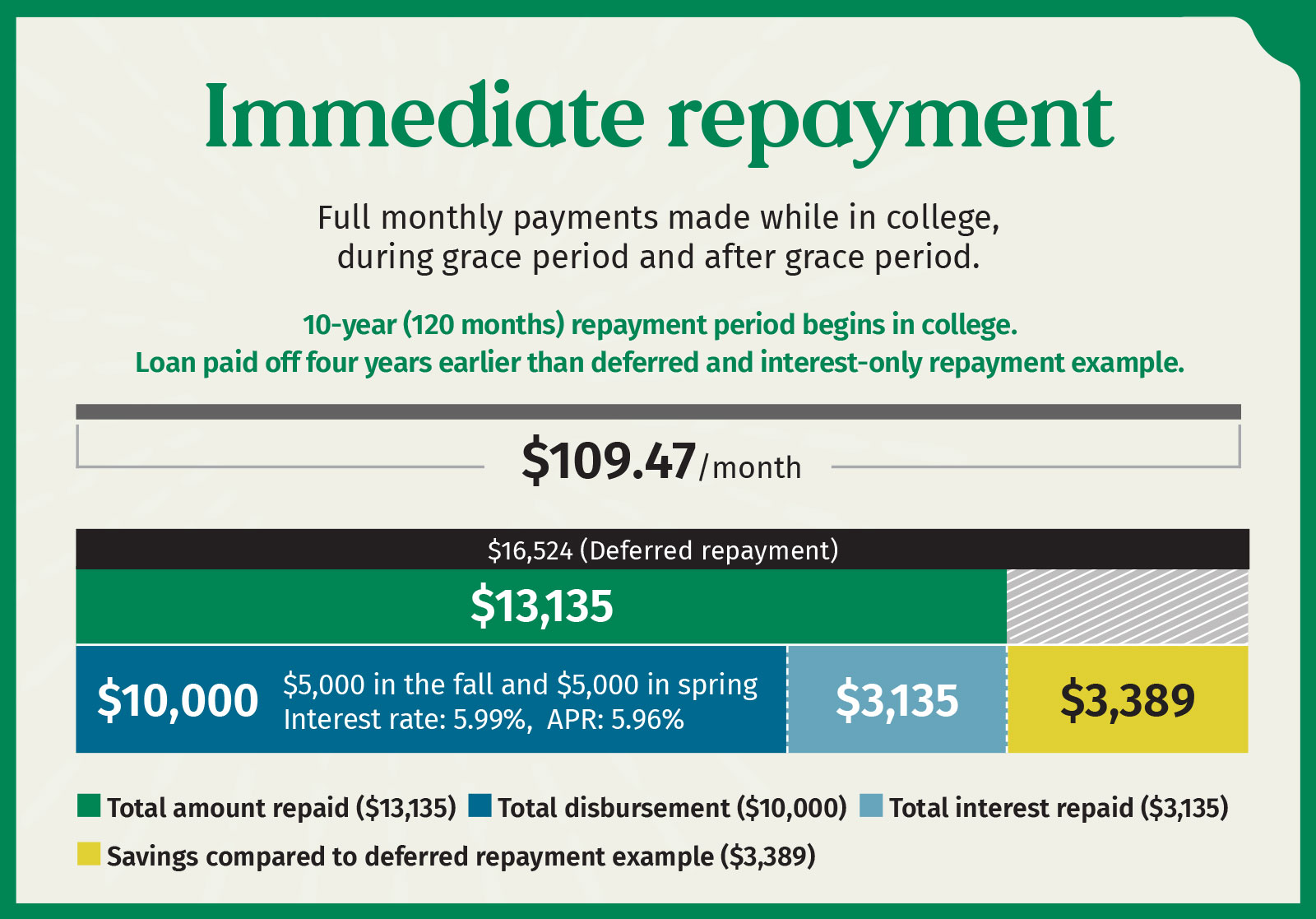

For example, let's say you have a $10,000 undergraduate private student loan with a 10-year (120 month) repayment period. The loan has a 5.99% interest rate, and you graduate college in 4 years. Here are some different repayment scenarios:

Disclaimer: The figures used on this page are for illustrative purposes only and do not constitute the rates the borrower may receive and the results may not be typical results the borrower will receive.

In these repayment examples, if you chose deferred repayment, you don't make any payments while in school or during the grace period. However, you end up with the highest total amount repaid of all three options and $6,524 in total interest repaid.

In the interest-only repayment example, you'd make payments on the interest while you're still in school and during the grace period. While the payments may fluctuate, they'd be approximately $50 per month during that time. After you graduate and the grace period ends the full monthly payment (principal and interest) would be $110.99. That means you'll end up with $5,725 in total interest repaid — $799 less than the deferred repayment option.

In the immediate repayment example, you'd start making full monthly payments of $109.47 while in school. You'll pay a total of $3,135 in interest — $3,389 less than the deferred repayment option.

You may end up needing multiple student loans throughout each academic year in college. While you might be able to make immediate repayment on some student loans, you might have to opt for deferred repayment on others to keep your in-school monthly payments manageable. It's important to look at your student loan debt holistically and choose the options that will work best for you.

Is there any penalty to paying off student loans early?

Typically, you can prepay all or part of your federal and private student loans off early without any penalties (although you should always double check with your lender). It's also important not to be late on payments — you could get hit with late fees, as well as impact your credit score. If it remains unpaid long enough, it can eventually go into default and then be transferred to a collection agency.

If you choose a deferred repayment option but make payments here and there while you're in school and during the grace period, it won't help your credit score at all, because the loan technically isn't in the repayment period yet.

What are some ways to help pay for in-school payments?

Money is usually tight for college students. That being said, it might be necessary to come up with some creative ways to help fund your student loan payments while you're in school. If you have a summer job, you could try to save the amount you'll need throughout the school year for those payments.

Besides a summer job, you can search for on-campus jobs, look into tutoring middle or high school kids who live near your college campus, put out ads for dog walking or house sitting, babysit, or even search the web for freelance positions. Every little bit could help make the payments easier to manage.

Other tips and tricks

Some other things that might help with paying student loans while you're in school is first, set up autopay so you don't have to worry about missing a monthly payment. If there's a day that's better for your payment to come out on (like pay day), you could check with your lender to see if it's possible to set that up.

Learning how to create and stick to a budget is also something that could be beneficial not only for paying on your student loans, but for managing your finances in general. The more in-tune you are with where your money is going, the better off you'll be.

The importance of understanding repayment options

This time in your life is full of big decisions, including what student loans and repayment plans are right for you. It's important to choose the repayment plan that works best for you and your family based on your unique financial situation.

If you still have questions or need help, we're here for you. With rate discounts and flexible repayment options, you can find a Citizens Student Loan™ that fits your life and budget.† Want a quote? You can get a rate quote from Citizens in about two minutes with no impact to your credit score.†

Related topics

Private student loans: What you need to know

Private student loans could help bridge the gap between the cost of college and what is available from financial aid.

Comparing financial aid offers: How to choose the right college

Learn how to compare financial aid offers from multiple colleges to choose which one is right for you.

8 tips for optimizing your college scholarship search

Consider these tips to help you get the most out of your scholarship search.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

† For additional information, please click the † symbols throughout this page to view our student lending disclosures.

Disclaimer: The information contained herein is for informational purposes only, as a service to the public, and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.