How to save when you’re young and starting out

Key takeaways

- Learn your savings potential by subtracting all monthly bills and everyday expenses from your net monthly income.

- Organize your money into separate accounts for bills, everyday expenses, emergency funds, and individual savings goals.

- Set up automatic transfers from each paycheck so saving money is prebuilt into your budget.

A lot of young people are giving savings the cold shoulder. About 60% of folks ages 25 to 34 have less than $1,000 saved. Another 61% of 18- to 24-year-olds are in the same boat.

Student debt is certainly a factor, but there's bound to be some room in the budget for saving. Really, it comes down to accounting for every dollar coming in and out.

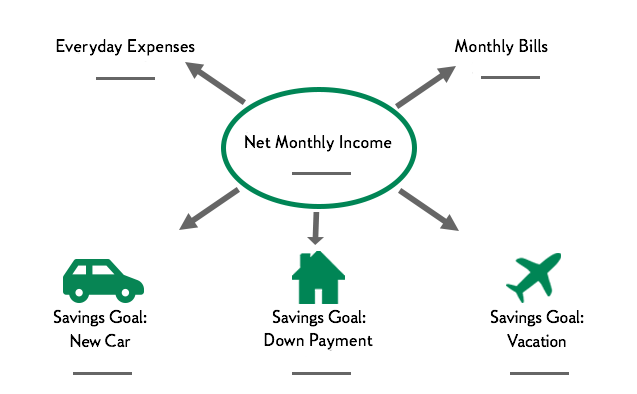

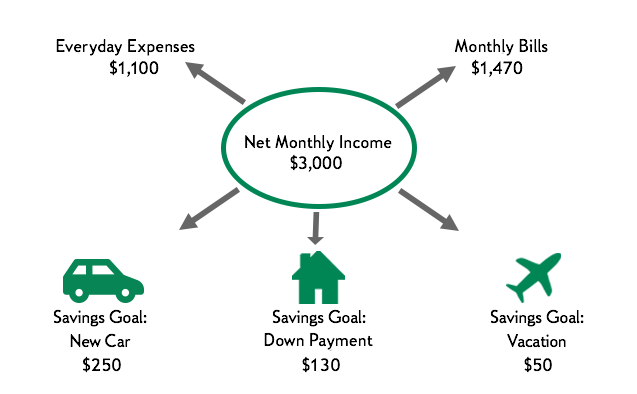

What if you could set up a system that has a separate account for everyday expenses (groceries, gas, weekend activities), another for bills, and individual savings accounts for each goal? Every paycheck could automatically transfer the appropriate amount of money to each account.

This gives every dollar a purpose. Like when you're filling up your car at the gas station, you'll know to pay for it through your everyday expenses account. When rent is due, the money is waiting for you in your bills account.

Your system could look something like this:

Nope, it's not rocket science. It's something you can set up today to reduce the stress of managing your finances.

Let's get started.

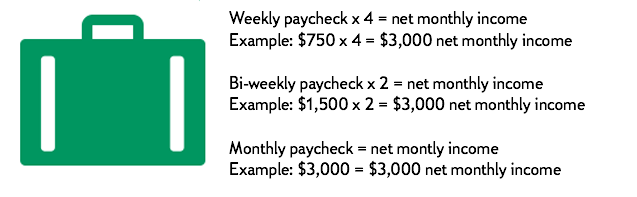

Step 1: Figure out your net monthly income

Add up all your paychecks from the past month. That's how much money you'll have to work with each month — assuming your income doesn't vary — to cover all everyday expenses, bills, and savings.

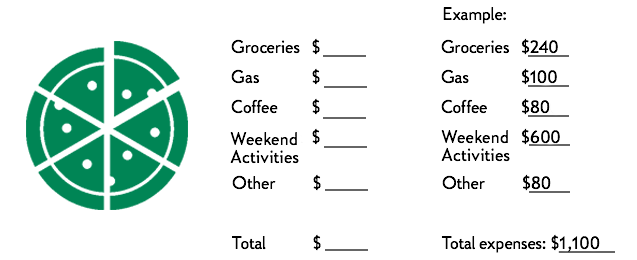

Step 2: Add up everyday expenses

How much do you spend each month on recurring everyday expenses? The price tags on these purchases can vary week to week, month to month, so they're harder to predict. But by looking back at previous months, you can get a general idea on how much you tend to spend on these recurring expenses. Then, you can set your budgeting goals based on your spending habits. Log them as seen below:

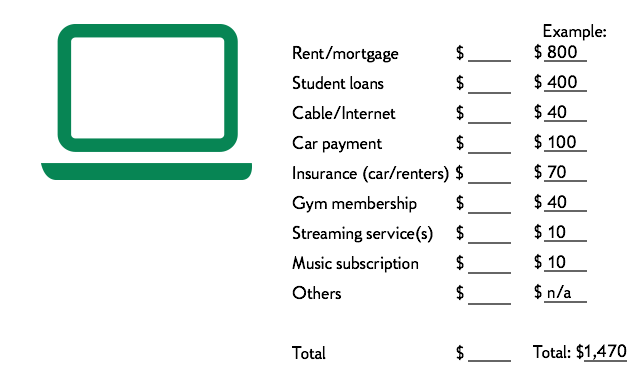

Step 3: Tally up your bills

Most bills — rent/mortgage, student loans, car payment, cable, Internet, insurance, gym memberships, subscriptions, streaming services — cost the same every month. Therefore, they're easier to account for. Add all your monthly bills together.

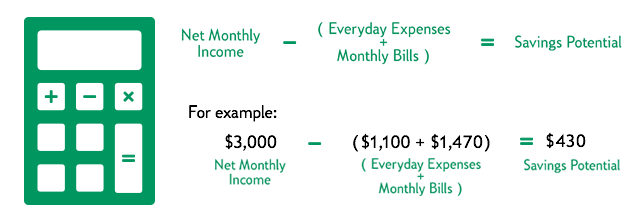

Step 4: Calculate your savings potential

OK, time to put it all together. Take your net monthly income and subtract your everyday expenses and bills from that number. What's left over? The money you can save each month, A.K.A. your savings potential.

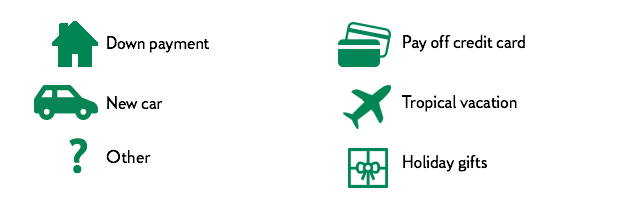

Step 5: Choose your savings goals

But first, what are those goals? What are you saving for? List out your savings goals, both short-term and long term, so you can figure out how much to distribute to each one. They could look something like this:

You'll open a savings account for each goal.

Bonus tip: leverage financial tools, like Citizens Savings Tracker™1, to help automate your savings so you can stay on top of your goals.

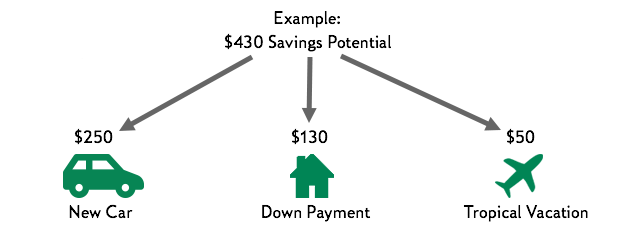

Step 6: Divvy up savings potential to your goals

How much do you want to save monthly for each goal? Distribute your savings potential across all goals. Prioritize accordingly — you might want to save more for one goal if you need to reach it sooner or if it's more expensive.

Now your savings graph should be filled up!

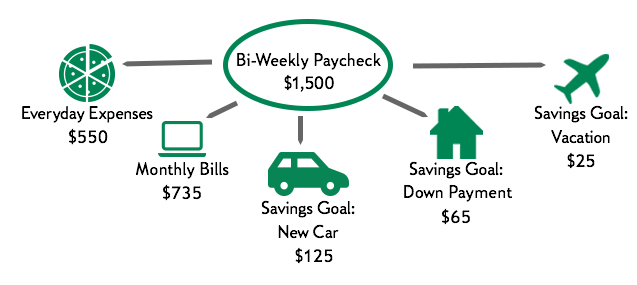

Step 7: Set up your automatic transfers

Last step! Now that you have separate accounts for each goal, set up the automatic transfers from each paycheck to cover each month's totals. So if you get paid bi-weekly, that means you'll usually have two paychecks each month to cover all everyday expenses, bills, and savings.

So your automatic transfers could look like this:

What to remember

Even the best plans need to be revisited every so often. The same goes for your savings plan. Over time, things change — your income, priorities, or perhaps you've added (or completed) another savings goal. Check your plan on a recurring basis to make any necessary changes to keep your plan up to date.

Warning: You might feel broke in the early going; that's normal. You'll feel much better about your money management a few months in. Plus, practicing these saving habits today can set you up for the rest of your life.

Ready to tackle your financial goals?

When you have multiple goals to save for, you don’t have to feel overwhelmed. Planning and prioritization can make you ready to reach them all. Citizens is here to help – with banking that stands with you and grows with you. And with automatic transfers from your checking to your savings account, you can set money aside and watch your savings add up.

Want more ways to hit your savings goal?

Related topics

What is an emergency fund?

How to create a budget

New to investing? Check out these tips

- 1 Subject to account eligibility. Only available on the Citizens Bank Mobile Banking application. Text and data rates may apply.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public, and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.