Is a vacation home a good investment? 3 reasons why you should buy a vacation home today

Key takeaways

- A vacation home offers invaluable benefits for your family's travels beyond what you could enjoy in a hotel or rental.

- Second homes may offer thousands of dollars in rental income or increased value as an investment property.

- With recent, significant increases in the average homeowner’s equity, using a home equity line of credit (HELOC) to leverage the equity in your primary residence could be a viable option for financing a vacation home of your own.

Picture this: You pull into your favorite travel destination. Everyone grabs their bags, leaps out of the car and runs excitedly into the house — your house. It's another weekend away, another summer trip or another cozy holiday at your own vacation home.

Best of all, it could be a reality. Too often, people believe that vacation homes are something only the ultra-wealthy own. However, buying a second home can be an option for the average American, particularly if they leverage the equity they've built in their existing home.

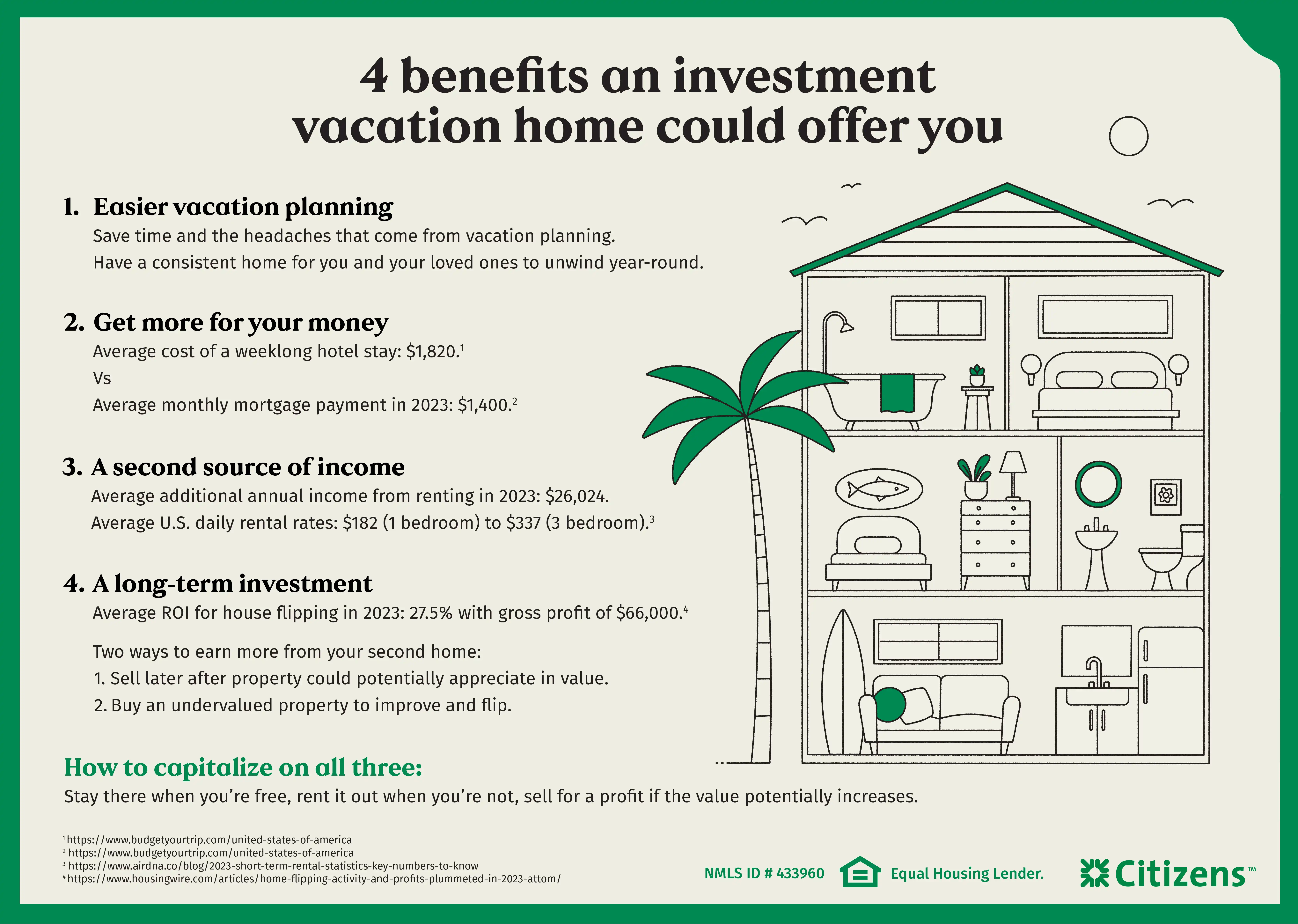

But is a vacation home a good investment? Is it worth the upfront and maintenance costs? Owning a vacation home may, in fact, offer some unexpected and valuable benefits for you and your loved ones. Let’s look at three reasons why a vacation home may be a good investment for you.

Reason #1: Easier vacations and big savings

A vacation home resolves some common travel hassles and introduces wonderful opportunities for your family. Consider these benefits of investing in a vacation home:

- Skip the stress of extreme pre-planning. High demand for popular destinations often requires reservations booked months in advance. With your own house on standby, you don't have to spend time researching places to stay ahead of time. You'll be able to take advantage of last-minute travel, knowing you'll always have somewhere to rest your head.

- Consider the savings. The cost of hotels and home rentals can skyrocket during peak travel seasons and holidays. In 2023, the average one-week vacation cost in the U.S. was $1,993 per person. But the median U.S. mortgage payment was just $1,400. This means a family of four could enjoy six months in their vacation home for the same price of a traditional weeklong vacation at a hotel.

- Make years of family memories. Gather loved ones each year for a tropical spring break, a snowy holiday season in the mountains or cool summers by the lake. Or buy a cottage in the country for relaxing weekends away. As frequent visitors, you'll enjoy the benefits of being part of your community and participating in its seasonal events too.

- Enjoy comfortable familiarity and the ability to customize the space to your family's needs. Stock up on your favorite supplies and decorate to your unique taste. Plus, minimize packing pains by storing holiday decor, beach supplies, personal items, clothing and more, so it's always there for you.

Reason #2: Establish a second source of income

When you're not using your second home yourself, it can provide an excellent source of income through renters.

Demand for vacation home rentals continues to grow year over year. In 2023, the short-term rental market expanded to $64 billion in revenue, with travelers staying 207 million nights in vacation rentals.

In fact, tourists are increasingly choosing to vacation in home rentals over hotels thanks to additional living space, privacy, home-like amenities and cost-effectiveness for large groups. And, with a surge in remote work, many people are taking advantage of short- and long-term home rentals for a change of scenery.

The price you can command for your rental depends on several factors, including location and the property itself. But the average vacation home rental produced an income of $26,024 in 2023. Average daily rates across the U.S. were $182 for one-bedroom homes, $255 for two bedrooms and $337 for three bedrooms.

Additionally, getting your home listing in front of renters is easier than ever with popular online platforms like Airbnb, Booking.com, Expedia and Vrbo. These sites simplify the process of connecting renters with homeowners, collecting payment and ensuring a smooth rental process. The features offered through these booking sites could limit your costs, save you on advertising and make renting out your home nearly passive.

Reason #3: Long-term investment opportunities

The right vacation home could be a smart way to diversify your existing portfolio. If you want to reap the benefits of your home as an investment, look first at the housing market in your desired area:

- Are current housing values inflated, or is now the time to buy?

- Is there likely to be a growing demand for properties in the future?

- How do the area and type of home impact that demand?

- Would people want to buy or rent your property during a limited season or year-round?

As you build equity in your second home, favorable market conditions can translate to increasing property values over time.

Of course, you'll want to consider the financial and time costs of any vacation home in calculating whether it makes sense as a wise investment. Remember expenses like mortgage and interest, property taxes, insurance, maintenance and repairs, property management and bookkeeping. Additionally, you'll have additional financial considerations if you plan to buy and flip an undervalued home instead of owning the house for years.

With the right property, you could achieve three goals:

- Enjoy the home yourself when you're able.

- Rent out the home when it would otherwise be vacant.

- Earn a return on your investment if property values increase and you decide to sell.

How to pay for your dream vacation home

The 2023 list of the most popular places to buy vacation homes offers unique insight. Among the top 10, the median vacation home sale price ranged from $340,000 to $928,900. Likewise, the prices you'll see will depend on the home's location, the type of property, the housing market and your budget.

Keep in mind that second homes require a down payment of at least 10% for a mortgage. So, amassing a lump sum of cash upfront is essential. But what are your options for getting that down payment ready?

Financial experts typically recommend saving your target amount over time before buying. You might also sell investments from your portfolio or other valuable assets you own.

You could consider a home equity line of credit (HELOC) to leverage the equity in your primary residence to either make up the difference of your down payment or cover it fully. A HELOC offers you the long-term ability to withdraw funds as needed for almost any purpose. The maximum amount you can borrow is based on your available home equity .

In general, untapped home equity has increased significantly in recent years. As of 2024, the average American homeowner holds $299,000 in home equity, a significant increase since just 2020, when that average was just $182,000 .

You may not even realize how much equity you have in your home or that you can use it to fund almost any financial goal that you have with a HELOC. If you're sitting on sizable equity in your family's primary home, consider tapping some of that value to purchase a vacation home.

Get ready for vacation!

So, is a vacation home a good investment? It could be!

Buying a vacation home could be an adventure. And owning that special place could afford your family years of happy memories — and some extra income.

Are you ready to kickstart the purchase process? Do you want to see what you qualify for in a HELOC? Citizens FastLine® could get you an offer in minutes with no commitment or impact to your credit score. And Citizens, ranked best in customer service by Money.com, will partner with you as you close on that dream vacation home.

Curious how a HELOC could help you reach your financial goals? Learn more about our easy HELOC process through Citizens FastLine®.

What is a home equity line of credit? (HELOC)

A HELOC offers unique benefits. But is it right for you? Learn how HELOCs work, when they're typically used and when you should consider other options.

Senior Living: Use your home equity to finance a renovation

Consider remodeling to help you better prepare for your own future or make your loved one's home more accommodating.

How to use home equity: 5 smart things to do with a HELOC

Thinking about a HELOC? Consider these five popular ways to use a HELOC to improve your quality of life.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Home Equity Lines of Credit are offered and originated by Citizens Bank, N.A. (NMLS ID #433960) Citizens Corporate Headquarters: One Citizens Plaza, Providence, RI 02903

Disclaimer: The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.