How much does a credit card cost to use?

Credit cards provide valuable payment flexibility when they're used responsibly. That means making full, on-time payments each month when your bill is due rather than paying for your purchases right away with a debit card.

When they're not used responsibly, credit cards can come with unwanted interest charges that could snowball in a hurry.

Not sure what we mean? Consider this: You want to buy a new couch that costs $1,000. When it comes time to check out, you decide to use a credit card - which offers 1.5% cash back on all purchases - instead of your debit card so you can pay off that $1,000 purchase over time rather than right away.

Will that charge cost you anything? It depends on how you pay off your balance.

Note: The examples below are for illustrative purposes only. They assume that the $1,000 purchase is the only transaction made on the credit card and that all monthly payments referenced are made on time. They do not consider potential additional fees and penalties associated with the credit card.

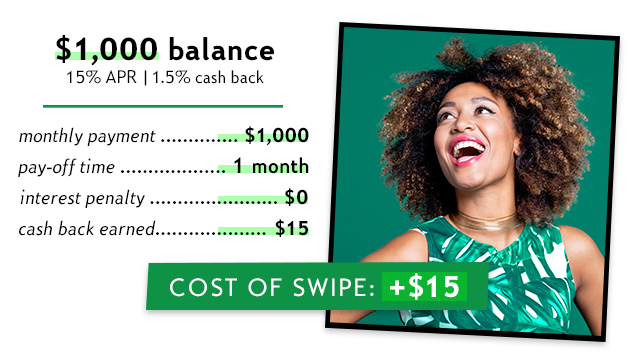

In this option, there is no cost of using a credit card. In fact, there's a gain! Using a cash-back card and paying off your balance in full actually makes your purchase less expensive.

Paying off your purchase in close to three equal increments seems like a good compromise between making the minimum payment and paying off your purchase in full. But there is a cost to use your credit card in this scenario of about three coffees.

In this scenario, your original purchase is getting noticeably more expensive, and the cost of using your credit card has added $60 to the purchase price of your couch.

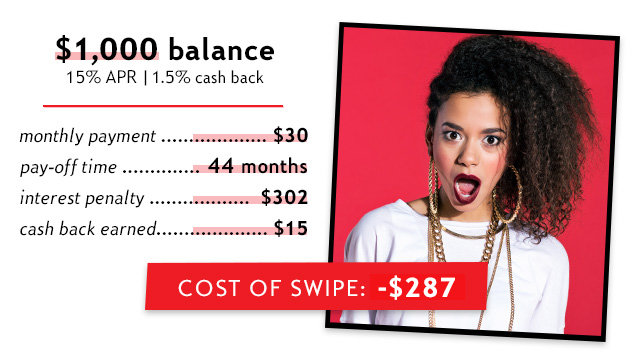

For this example, let's say your minimum payment each month is $30. Buying the couch might have officially entered "bad idea" territory, as the cost of using your card has skyrocketed to nearly $300.

As you can see from the first example, using a credit card - a cash-back card, not a travel rewards one - could make you money on the purchase if you pay your bill in full. That's why lots of people like to put large purchases on their credit card - yes, there's the flexibility to pay it off in a few weeks' time, but there's also the cash back.

Here's another example: You and a group of friends want to go to a concert. You find the tickets online and volunteer to buy everyone's using your credit card. Then, your friends send you the money for the cost of their ticket. A nice gesture, right? Yes, for sure, but it's also a smart financial move on your part. That's because you'll earn cash back on the entire purchase, not just your individual ticket. That cash-back bonus will help offset the cost of your ticket!

The important thing to remember is to pay off your bill in full each month. When you don't - particularly after a large purchase - that's when you can slip into credit card debt. In those cases, there's a cost of using a credit card.

The interest charges get applied to your next billing cycle. That might not be a big deal if you paid off a good portion of the bill. However, making only minimum payments or other smaller payments can make credit card debt difficult to manage.

What to remember

If you pay your credit card bills in full each month, there's no cost of swiping. In fact, you can earn money if the credit card offers cash back on your purchase.

If you don't pay off your balance in full, then the cost of using your credit card will be the amount of interest you pay. That number can range from a minor amount - $20 or less - to a more significant amount.

Ready to get more from your credit card?

Explore our four distinct cards, tailored to where you are and where you're going.

Related topics

How your credit score is calculated

How do cash-back credit cards work?

What does APR mean?

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public, and is not legal advice or a substitute for legal counsel, nor does it constitute advertising or a solicitation. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.

Mastercard and the circles design are registered trademarks of Mastercard International Incorporated.

Credit Cards are issued by Citizens Bank, N.A. pursuant to license by Mastercard International Incorporated.