Financial aid disbursement: All your questions answered

Key takeaways

- Financial aid — including scholarships, grants and loans — is typically disbursed at least once per semester.

- Most financial aid is released to the school, not directly to the student.

- You typically need to use your financial aid disbursement for qualified educational expenses like tuition, fees, textbooks and room and board.

Receiving financial aid to help fund a college education can be an immense relief for students and their families. But how does awarded aid make its way to students so they can pay for necessary educational expenses? There's a simple answer: financial aid disbursement.

During the disbursement process, a school receives aid from various sources and credits those funds to a student's account. While the timeline can vary by school and type of aid, this guide will help demystify how and when those funds get to students, the refund process and ways students can use financial aid to cover educational expenses.

What does financial aid disbursement mean?

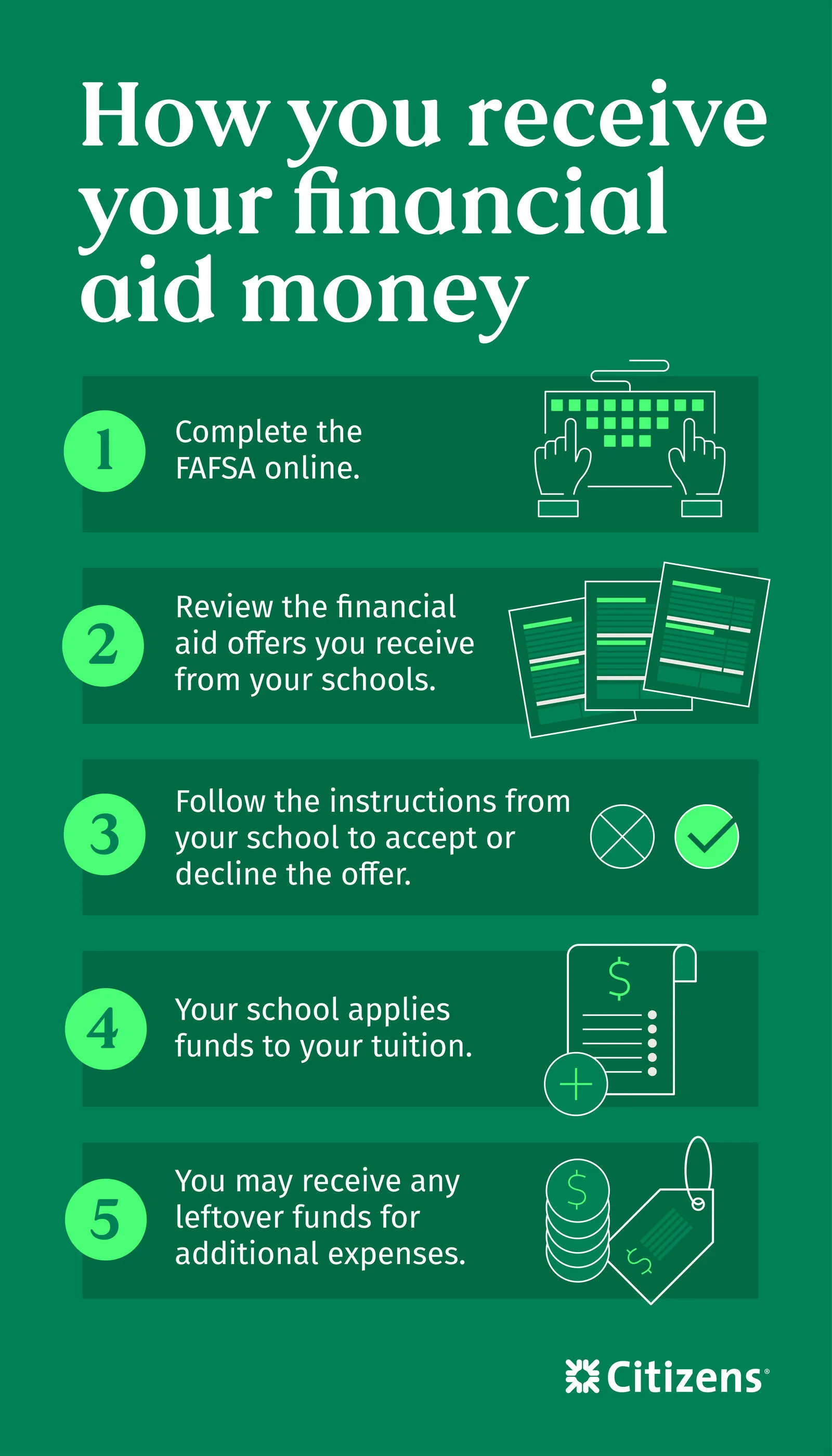

Financial aid disbursement occurs when a school applies awarded financial aid to a student's account. It often starts with completing the Department of Education's (ED) FAFSA, or Free Application for Federal Student Aid.

After students and parents complete the FAFSA, schools can access a student's estimated financial need. From there, schools create financial aid packages to help students pay for costs associated with their education.

Packages can include different types of aid, including grants, scholarships and federal student loans. Some aid, like student loans, must be repaid. However, awards like grants and scholarships typically do not require repayment, although there may be other obligations associated with them.

How do you receive financial aid and loan money?

The first step to receiving your financial aid is officially accepting your offer. Once you've done that, aid issuers send accepted funds directly to your school. Funds typically go directly to the school's financial aid or bursar's office.

In some situations, however, you might receive a check payable to your school from a private scholarship. In this case, you'll hand deliver the check to your school's financial aid or bursar’s office so they can credit the funds to your account.

With aid funds now securely in your student financial account, your school applies the money to your outstanding charges for the current term, which typically includes tuition, fees and room and board costs.

If there's money left over after those charges have been paid, your school may do one of two things: keep the extra to apply to future semesters or disburse the overage as a refund directly to the student. Policies vary by school, so ask your financial aid office how they handle excess funds.

If your school issues a refund, it will likely be paid via direct deposit to your bank account. Be sure to follow your school's instructions for linking your bank account to your bursar account to ensure funds reach you seamlessly.

When will your financial aid be disbursed?

Schools generally disburse financial aid at least once per term and before the term begins. However, in some cases, federal student loans have waiting periods. Here are a few to make note of, especially for first-time borrowers:

- First-year undergraduates may have a 30-day waiting period after classes begin before your school releases federal loan funds.

- First-time borrowers taking out Direct Loans (subsidized and unsubsidized) must complete a promissory note and entrance counseling through the ED before funds can be released.

- Graduate and professional students who are first-time borrowers of Direct PLUS Loans must complete a promissory note and entrance counseling before loan funds are released.

If you have grants and scholarships as part of your financial aid package, the issuer of those funds will let you know if there are special requirements to meet before they release your awarded aid.

For example, some scholarships may require thank-you letters, orientation sessions or publicity releases. If you have questions, the entities granting your aid can answer questions about how you'll receive funds and those timelines.

What kinds of financial aid are disbursed?

Financial aid comes in many shapes and sizes. The type of aid you're offered generally relates to your financial need (determined by your FAFSA), academic performance or affiliation with an aid-granting organization.

- Grants: Grants are typically awarded based on financial need and do not need to be repaid except under certain situations. One popular undergraduate grant program is the federal Pell Grant.

- Need-based scholarships: Eligibility for need-based scholarships is generally determined by your FAFSA. These funds usually do not need to be repaid but may come with conditions students must meet to avoid having to repay.

- Merit-based scholarships: Merit-based scholarships usually go to students demonstrating high academic achievement or community involvement. These may have GPA requirements or require that the student or parent belong to a particular organization to be eligible.

- Federal student loans: Federal loans are issued by the ED and have fixed interest rates set annually by the federal government. A student's FAFSA determines eligibility, and the amount you can borrow is subject to limits set by the ED. Federal loans may be eligible for government student loan relief programs that can decrease or forgive amounts owed.

- Private student loans: Private loans are issued by banks, credit unions and other nongovernment lenders. As part of the application process, lenders consider a variety of factors when determining eligibility, including if you're attending an eligible school, if you meet enrollment criteria, your credit quality, income and other factors. Private loans may have higher borrowing limits than federal loans, and interest rates can vary by lender. Private student loans aren't eligible for federal student loan relief programs.

How can I use my financial aid disbursement?

If you receive money back from your school after all your financial aid funds have been applied to your tuition bill, you may be able use the money to pay for other college expenses like required school supplies and textbooks.

If you use your financial aid disbursement to pay for expenses that aren't related to school, you are in violation of your FAFSA Certification Statement. With federal loans, for example, this could result in the ED canceling your loan agreement and a demand for immediate repayment.

Your best bet is to always use your financial aid disbursement for clear-cut educational expenses. Check with your financial aid office to learn more. You may also want to consult a tax advisor to determine how much of your financial aid funds are considered taxable income.

Consider private loans to help fund your education

Figuring out all the details of planning and paying for college is not an easy task. But we are here to help you at each stage of your college journey. If you find that you still need help paying for college after maximizing other financial aid sources, a private student loan could help you bridge that gap. With rate discounts and flexible repayment options, find the Citizens Student Loan™ that fits your life and budget.†

Related topics

A guide to federal financial aid

Federal financial aid can be a critical piece of paying for college. Learn the different types you could qualify for including federal grants, work-study and federal student loans.

How to build your credit in college

Building credit in college could help with life after graduation. Learn how to get started.

Private student loans: What you need to know

Private student loans could help bridge the gap between the cost of college and other sources of financial aid.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

† For additional information, please click the † symbols throughout this page to view our student lending disclosures.

Disclaimer: The information contained herein is for informational purposes only, as a service to the public, and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.