Money market vs. CD

Key takeaways

- Money market accounts are more accessible than CDs, allowing you to withdraw money when needed.

- With a CD, your money is locked away for a set term, but you'll typically earn more interest.

- Money market accounts and CDs typically have higher interest rates than traditional savings accounts. Mutual funds are considered riskier than both but may pay higher returns.

When looking for a bank account to tuck away savings and see your money grow, you have options beyond a savings account. Money market accounts (MMAs) and certificates of deposit (CDs) offer the stability of traditional types of savings accounts with higher interest rates. While both can help you boost your savings, there are distinct differences between a money market account and a CD.

Let's compare these two types of savings accounts to see which one may be right for your financial goals.

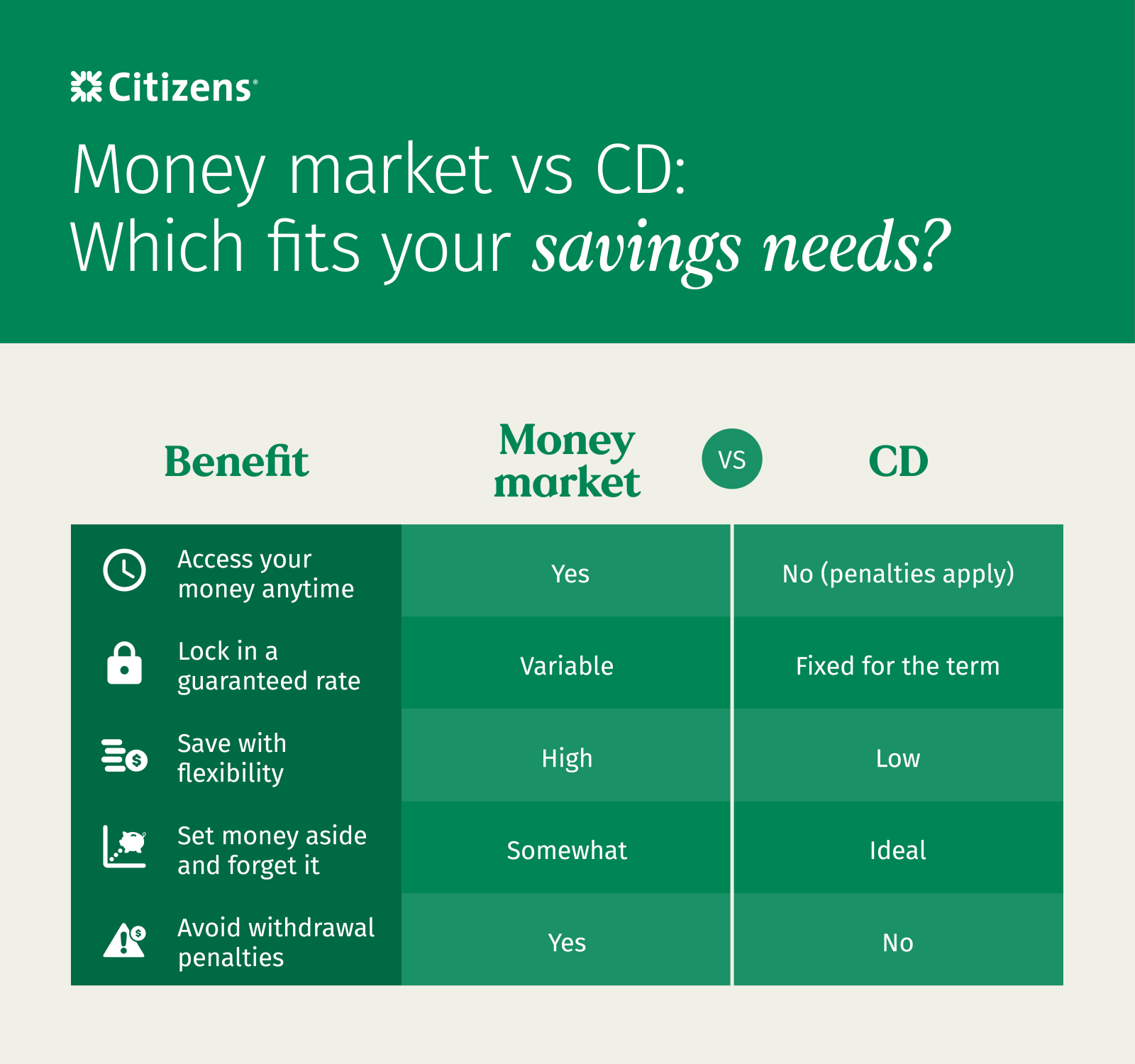

Money market account vs. CD: What’s the difference?

A money market account and a CD can help you with saving money for future goals, such as building an emergency fund or saving for a down payment. Both accounts earn interest. But CDs limit access to your money during the term and money market accounts don't.

A CD is a type of timed deposit account. When you open a CD, you choose the term length, or set time period, for how long you'll leave a set amount of money in the account. CD terms can range from three or six months to longer than five years. Often, the longer the CD term, the higher the interest rate. If you need to take money from your CD before the term ends, you pay a penalty, often in the form of a few months' interest.

A money market account doesn't have fixed term lengths. It operates similarly to a savings account with a few features you'd commonly see in a checking account, such as a debit card or checks. If you need to withdraw from your money market account, you can do so, typically without a penalty.

What are the pros and cons of money market accounts and CDs?

When deciding where to park your savings, both CDs and money market accounts offer advantages and drawbacks. Understanding them can help you choose the best option based on your financial goals and need for flexibility.

| Money market account | CDs | |

| Pros |

|

|

| Cons |

|

|

How much money can you make with a money market vs. CD?

The interest you earn with a CD or money market account depends on several factors, like your balance and the annual percentage yield (APY), which is the annual rate of return that includes compound interest. Compound interest is the interest you earn not just on your original deposit, but also on the interest that accumulates over time.

Here are two examples to show how your earnings can differ:

Example 1

You have $10,000, and no intention to touch the money for at least three years. You lock in a 3.25% APY with a 36-month CD. After 3 years at 3.25% APY, your $10,000 would earn about $1,007.54 in interest.

Example 2

You have $100,000 in a money market account earning a 0.5% APY. After one year, your $100,000 would earn about $500.63 in interest — assuming you don't make any additional deposits, interest stays at 0.5% and compounds monthly.

How do you choose between a money market account and a CD?

Choosing between a money market account and a CD depends on your savings goals, timeline and need for access to your funds. A money market account may be an ideal choice if you want flexibility and easier access to your funds for short-term savings. A CD might be better if you know you won’t need the money for a while and want to lock in a fixed interest rate. Here's a breakdown to help you decide.

When to choose a money market account:

- You want the option to withdraw or transfer money more easily (often via checks or debit card).

- You’re saving for a short- to medium-term goal, like a vacation or emergency fund.

- You prefer an account that earns interest but doesn’t lock your money away.

- You want the flexibility to add funds at any time.

When to choose a CD:

- You have a specific savings goal with a clear timeline (e.g., buying a car in 12 months).

- You can leave the money untouched for the full term.

- You want to lock in a fixed CD rate, potentially higher than a traditional savings or money market account.

- You're comfortable with early withdrawal penalties if you access the funds before maturity.

Money market account vs. CD vs. mutual fund

Another way to grow your savings is through a mutual fund. When you invest in a mutual fund, you're buying into a portfolio of securities that can include stocks and bonds. A company or individual manages the fund and chooses the securities, with the goal of outperforming the market benchmark. Ideally, a mutual fund will give you a return on your investment. It's best for long-term goals that are several years away, like retirement, and can handle some risk in exchange for potentially higher returns.

But unlike a money market account or CD — which earns interest no matter what — the return on a mutual fund isn't guaranteed. If market conditions decline or the securities in the fund underperform, you can lose money. Mutual funds aren't FDIC-insured and are considered riskier than CDs or money market accounts.

Mutual funds also charge fees, which eat into the amount you earn. The fees vary based on the fund but can include a management fee, account fee, purchase fee and redemption fee.

| Money market account | CD | Mutual fund | |

| FDIC-insured | Yes | Yes | No |

| Fees | Sometimes | No | Yes |

| Penalties | None | Early withdrawal penalty, usually the equivalent of several months' interest | Varies depending on the account. If you invest in a mutual fund in a retirement account, you may pay an early withdrawal penalty. |

| Access | Withdrawals allowed, check-writing privileges and/or debit cards provided | Funds are available without a penalty at the CD's maturity date | Limited, you need to sell your share of the fund to get your money |

FAQs about money market accounts and CDs

Want to learn more about a CD or money market account? Here are a few answers to FAQs

A CD can be a good investment if you're saving for a medium- or long-term goal, want to earn a fixed interest rate and value the assurance that your money is safe. If you need access to your money, a money market account would be more fitting as it offers greater liquidity.

The Federal Deposit Insurance Corporation (FDIC) insures both money market accounts and CDs in the rare case a bank fails. FDIC insurance covers up to $250,000 per depositor, per ownership category, per financial institution.

Brokerages allow you to purchase CDs from multiple institutions and manage them in a single account. You can often redeem a brokered CD before the term ends, usually by selling it.

A callable CD is a type of CD that a bank or financial institution can "call" or redeem before its maturity date. If you invest in a callable CD with a high interest rate and the market drops, your bank may redeem it early because they now have the option of borrowing money at a lower rate. Callable CDs often have higher rates than other CD types — the trade-off is that you can lose access to that interest rate.

You pay income tax on the interest a money market account or CD earns.

A money market account may limit the number of transactions you perform during a statement period, which is usually a month. For example, you may only be allowed six withdrawals in a single month.

Ready to grow your savings?

Ultimately, both money market accounts and CDs offer secure ways to grow your savings, but the best choice depends on your financial goals and need for flexibility. Learn more about CDs and money market accounts at Citizens.

Related topics

8 tips to achieve multiple savings goals

Achieving multiple savings goals over time takes planning. Use these tips to help you save what you need.

How to save money: 9 ways to start today

Need to save money fast? Get actionable tips to cut costs, boost your income, and make faster progress toward your financial goals.

How to save $10,000 in a year

You can save $10,000 a year by , adjusting your budget and choosing the right savings account for your goals.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.