Understanding retirement account tax benefits: Roth vs. traditional

By Jason R. Friday, CFP®, MPAS®, RICP®, CMFC, Head of Financial Planning | Citizens Wealth Management

Key takeaways

- Retirement accounts help you save and invest for the future while offering important tax advantages.

- These tax benefits can apply to contributions, growth or withdrawals in retirement.

- Traditional and Roth accounts differ in how and when taxes apply, allowing you to compare what aligns best with your goals.

While consistent contributions are essential to building your retirement savings, choosing the right type of account can help ensure you're approaching your goals in a tax-efficient way.

The tax benefits of retirement accounts vary depending on the type of account. Understanding the differences, particularly between traditional and Roth accounts, can help you make more efficient progress toward your long-term goals.

This overview breaks down how taxes apply to retirement accounts, how traditional and Roth options compare, and the key factors to consider as you decide which approach aligns best with your income, timeline and retirement plans.

What are retirement accounts?

Retirement accounts are specialized investment accounts designed to help you meet long-term retirement goals. While these accounts include rules around contributions and withdrawals, they also offer tax benefits that could help accelerate your progress.

Retirement accounts typically fall into a few categories:

- Employer-sponsored plans: 401(k), 403(b) and 457(b) plans

- Individual retirement accounts: IRAs, SEP IRAs and SIMPLE IRAs

- Self-employed retirement accounts: Solo 401(k), as well as SEP IRAs and SIMPLE IRAs

Most of these accounts come in traditional and Roth versions, each with its own tax treatment. For example, there is a traditional IRA and a Roth IRA, and your employer may offer traditional and/or Roth 401(k) plan options. Before comparing these options, it's helpful to understand how taxes affect your retirement savings at different stages.

Three key tax considerations for retirement accounts

Retirement accounts can influence your taxes in three primary areas:

- Contributions: Some accounts allow you to contribute pre-tax dollars, reducing your taxable income for the year. Others require after-tax dollars, which means no upfront tax break.

- Growth: Investment earnings such as interest, dividends or capital gains are not taxed while the money remains in the account. On the other hand, investment earnings in a regular brokerage account are taxable each year, even if the funds remain in the account.

- Withdrawals: Some accounts require you to pay taxes when you take money out in retirement, while others allow for tax-free withdrawals if certain rules are met.

Most retirement accounts are tax-advantaged in two of these three areas. That trade-off is what distinguishes traditional and Roth accounts.

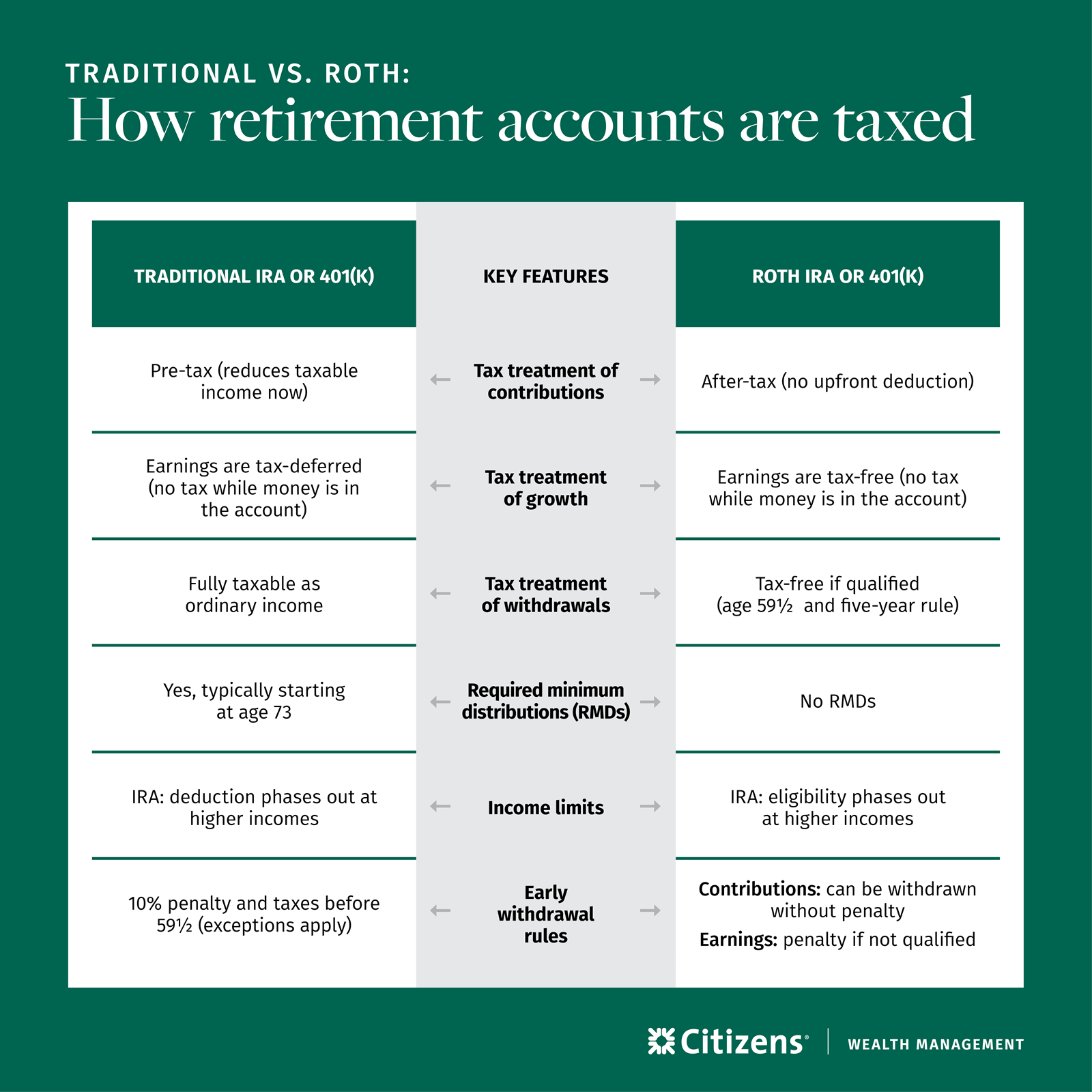

Traditional vs. Roth tax timing

The main difference between traditional and Roth retirement accounts is when you pay taxes.

Traditional retirement accounts

Traditional accounts offer an upfront tax benefit. Contributions are made with pre-tax dollars, lowering your taxable income today. In retirement, withdrawals are taxed as ordinary income, including both contributions and any investment gains.

Roth retirement accounts

Roth accounts work the opposite way. Contributions are made with after-tax dollars, so there's no immediate deduction. However, your contributions can be withdrawn tax-free and penalty-free at any time.

Withdrawals of earnings are tax-free once you reach age 59½ and meet the five-year rule. The five-year rule requires that at least five years pass between January 1 of the tax year of your first Roth IRA contribution and any withdrawal of earnings. Withdrawals of earnings that don't meet these requirements are considered nonqualified and may be subject to taxes or penalties.

Tax-deferred and tax-free treatment of growth

Both traditional and Roth retirement accounts allow for the opportunity for investments to grow without being taxed while the money stays in the account. Traditional accounts provide tax-deferred treatment of growth since taxes apply later when you withdraw from the account. Roth accounts offer tax-free treatment of growth since eligible withdrawals are not taxed.

How traditional and Roth options apply across account types

Most savers encounter traditional and Roth options through employer-sponsored plans or IRAs. While the tax treatment is consistent, each account type has its own rules, limits and benefits.

Employer-sponsored retirement plans (401(k), 403(b) and 457(b))

If you have access to a workplace retirement plan, you can set up automatic contributions to come out of your paycheck. Many plans offer traditional and Roth options, allowing you to choose the approach that best fits your goals.

Contribution limits

In 2026, the contribution limits1 for these plans are:

- Under 50: $24,500

- 50 or older catch-up: Additional $8,000 (total $32,500)

- Ages 60 to 63 "super" catch-up: Additional $11,250 (total $35,750)

Matching contributions

Many employers offer matching contributions for workplace retirement plans. For example, an employer might match your contributions up to 4% of your annual pay.

New Roth catch-up rule

For workplace retirement plans, there's a new rule for catch-up contributions starting in 2026.2 Those who earned more than $150,000 in 2025 will be required to make any catch-up contributions on a Roth basis, meaning you pay taxes now but may have tax-free withdrawals in retirement. However, you can still make standard pre-tax contributions before reaching the catch-up limits.

Individual retirement accounts

You can open an IRA through a financial institution or brokerage firm, whether or not you have a workplace plan. IRAs offer additional investment flexibility because you're not limited to an employer's menu of investment options.

Contribution limits

For 2026, IRA contribution limits are:

- Under 50: $7,500

- 50 or older catch-up: Additional $1,100 (total $8,600)

Income limits

For Roth IRAs, eligibility to contribute phases out if your income is between $153,000 and $168,000 (single) or between $242,000 and $252,000 (married filing jointly).

There's no income limit to contribute to a traditional IRA. However, your ability to deduct contributions may phase out if you or your spouse is covered by a workplace plan and your income exceeds certain thresholds.

Tax advantages of health savings accounts

A health savings account (HSA) is primarily used to save for medical expenses, but it can also support your retirement planning with its three-fold tax benefit:

- Tax-deductible contributions

- Tax-deferred treatment of any growth

- Tax-free withdrawals for qualified health care expenses

Before age 65, nonqualified withdrawals are subject to income taxes plus a 20% penalty. After age 65, you can use HSA funds for any expense without the penalty, though it is still subject to income taxes.3 Restrictions and other rules do apply for using an HSA. For example, you must be enrolled in a high-deductible health plan to contribute to an HSA.

Make the most of your retirement accounts

Maximizing the benefits of retirement accounts begins with selecting the options that best fit your income, timeline and long-term goals. Factors like your age, current tax bracket and retirement income needs can guide your decision. Using a mix of Roth and traditional accounts may also help build flexibility for your future.

A Citizens Wealth Advisor* can help you evaluate your options and determine how they fit into your broader financial plan. Together, you can build a clear strategy that supports your needs today and helps you prepare for the years ahead.

Related topics

What is the 4% rule in retirement?

How much can you withdraw in retirement? Learn a simple benchmark for estimating annual income withdrawals.

Hidden costs in retirement: 6 unexpected expenses for retirees

A strong retirement plan addresses both the obvious and often overlooked expenses that can cut into your retirement budget.

Investing tax returns: smart strategies for making the most of your refund

Think you can maximize your tax refund this year? Consider these 5 helpful ideas for investing your tax return.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

1 IRS, "401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500," Nov. 2025

2 IRS, "Treasury, IRS issue final regulations on new Roth catch-up rule, other SECURE 2.0 Act provisions" and "IRS Notice 2025-67"

3 Congress.gov, "Health Savings Accounts (HSAs)," Feb. 2025

* Securities, Insurance Products and Investment Advisory Services offered through Citizens Wealth Management.

Disclaimer: Citizens Securities, Inc. and Clarfeld Financial Advisors, LLC do not provide legal or tax advice. The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.

Banking products are offered through Citizens Bank, N.A. ("CBNA"). For deposit products, Member FDIC.

Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the United States to Certified Financial Planner Board of Standards, Inc., which authorizes individuals who successfully complete the organization’s initial and ongoing certification requirements to use the certification marks.

All investing involves risk, including the risk of loss of principal. Investment risk exists with equity, fixed income, and other marketable securities. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

Citizens Wealth Management (in certain instances DBA Citizens Private Wealth) is a division of Citizens Bank, N.A. ("Citizens"). Securities, insurance, brokerage services, and investment advisory services offered by Citizens Securities, Inc. ("CSI"), a registered broker-dealer and SEC registered investment adviser - Member FINRA/SIPC. Investment advisory services may also be offered by Clarfeld Financial Advisors, LLC ("CFA"), an SEC registered investment adviser, or by unaffiliated members of FINRA and SIPC providing brokerage and custody services to CFA clients (see Form ADV for details). Insurance products may also be offered by Estate Preservation Services, LLC ("EPS") or an unaffiliated party. CSI, CFA and EPS are affiliates of Citizens. Banking products and trust services offered by Citizens.

SECURITIES, INVESTMENTS AND INSURANCE PRODUCTS ARE SUBJECT TO RISK, INCLUDING PRINCIPAL AMOUNT INVESTED, AND ARE:

· NOT FDIC INSURED · NOT BANK GUARANTEED · NOT A DEPOSIT · NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY · MAY LOSE VALUE