What is a balance transfer on a credit card and how does it work?

Key takeaways

- Balance transfer credit cards offer promotional interest rates on balances that you move to the credit card.

- Transferring balances to a card with a low or 0% introductory rate can help you save money on interest payments and make managing your monthly bills easier.

- Consider the balance transfer fee and drawbacks before you apply for a new credit card or move balances between accounts.

A balance transfer credit card isn't a specific type of credit card. Instead, the name refers to various credit cards that offer a promotional annual percentage rate (APR) on balances you transfer to the card.

Balance transfer offers often give you a low or 0% APR for a temporary promotional period. If you transfer credit card or loan balances to the card, you can pay down the debt without accruing additional interest. It can be a helpful strategy for paying off debt faster and paying less interest overall.

However, there are also limitations and fees to consider, and it's important to read the fine print of different balance transfer offers and compare your options before applying for a new credit card.

Understanding introductory APR

The key feature of a balance transfer credit card is the introductory balance transfer APR, but some balance transfer cards also offer an introductory APR on purchases. Here's how they differ:

- Introductory balance transfer APR: A lower or 0% APR that applies to eligible balances you transfer to the card for a promotional period.

- Introductory purchase APR: A lower or 0% APR that applies to eligible purchases you make with the credit card during the promotional period.

It's important to review the card's introductory offers to understand what happens if you make purchases with the card.

Generally, credit cards offer a grace period, and you won't pay interest on credit card purchases if you pay your balance in full each month. However, with some cards, a balance transfer will void the grace period even if it's part of an introductory offer. As a result, your purchases could start to accrue interest immediately if the card doesn't also have a 0% APR offer on purchases.

What to know before you transfer a balance

Additionally, you should review the introductory balance transfer offer to make sure you understand how it works. Three main points you want to look for are:

- The balance transfer APR: The interest rate that applies to balances you transfer to the credit card. Many credit cards offer an introductory 0% APR on balance transfers.

- The initial balance transfer requirements: In some cases, only the balance transfers you request or complete during a limited initial period will receive the introductory APR. If you request a balance transfer later, the transferred balance may accrue interest based on the card's standard balance transfer APR.

- The promotional period: The introductory APR only applies for a limited promotional period. Once the promotional period ends, any remaining transferred balance will start accruing interest based on your card's standard APR.

Some credit card issuers offer existing cardholders promotional balance transfer and purchase APRs. Although these technically aren't introductory APR offers, you can review the same key features and fine print to understand how they work and if taking advantage of the offer makes sense for you.

Who should consider a balance transfer?

Balance transfers can be a helpful and strategic part of managing debt, but they're not a great fit for every person or situation.

You may want to use a balance transfer if:

- You're paying off high-interest credit card debt: Moving high-interest credit debt to a card with a promotional 0% APR offer could save you money on interest payments. You could use these savings to pay off the debt faster or cover other monthly expenses.

- You have a high-interest loan: Some credit card issuers let you transfer balances from loans. Or you might be able to "transfer a balance" to your bank account and then use the money to pay down a loan. Generally, loans have a lower APR than credit cards, but a balance transfer could be a good idea if you're certain you can pay off the debt during the promotional period.

- You want to consolidate your monthly payments: Moving balances from several credit cards and loans onto one credit card can simplify your finances. If you stop using the other cards, you'll have fewer monthly bills to track and pay each month.

A balance transfer might not be the best option if:

- You want to have all your accounts at one financial institution: You generally can't transfer balances between credit cards from the same issuer. If you don't want to open a credit card with a different company, then a balance transfer might not be possible.

- You tend to have credit card balances due to overspending: Moving the debt to a new credit card won't address the underlying issue if you regularly overspend. Some people even wind up deeper in debt because they transfer balances to a new credit card and then max out their original credit cards again.

- You can pay off the credit card debt quickly: A balance transfer might wind up costing you more in fees than you'll save in interest payments if you can pay off the debt quickly.

What are the qualifications, and who is eligible?

Although they generally won't reveal specifics, credit card issuers consider a variety of factors when deciding whom to approve and what credit limit to offer. It's important to consider these factors because applying for a credit card can hurt your credit score, even if you don't get approved, due to the hard inquiry into your credit history. Getting approved with a low credit limit will also reduce the usefulness of the balance transfer offer.

Some common considerations include:

- The type of credit card: You can find balance transfer offers on various types of credit cards, including cards without an annual fee, rewards credit cards and travel credit cards. Some cards may be easier to qualify for than others.

- Your credit score: There usually isn't a specific credit score requirement, but having a high credit score can generally help you qualify for more credit cards and higher credit limits.

- Your credit history and accounts: Card issuers might examine different information from your credit report, such as how many credit cards you have, how much you owe overall and your payment history with different accounts.

- Your income and monthly housing expenses: Card issuers will ask about and consider your income and rent or mortgage payments when reviewing your application for a new card.

- Your experience with the issuer: Having a good relationship with the card issuer, such as a long history of using their credit cards or bank accounts, might make getting approved for a new credit card easier.

Credit card issuers may also have special considerations when they're promoting introductory 0% APR balance transfer offers to attract new customers. For example, they might try to figure out how much debt you'll likely transfer to the card and how much money they will make or lose on your account over time.

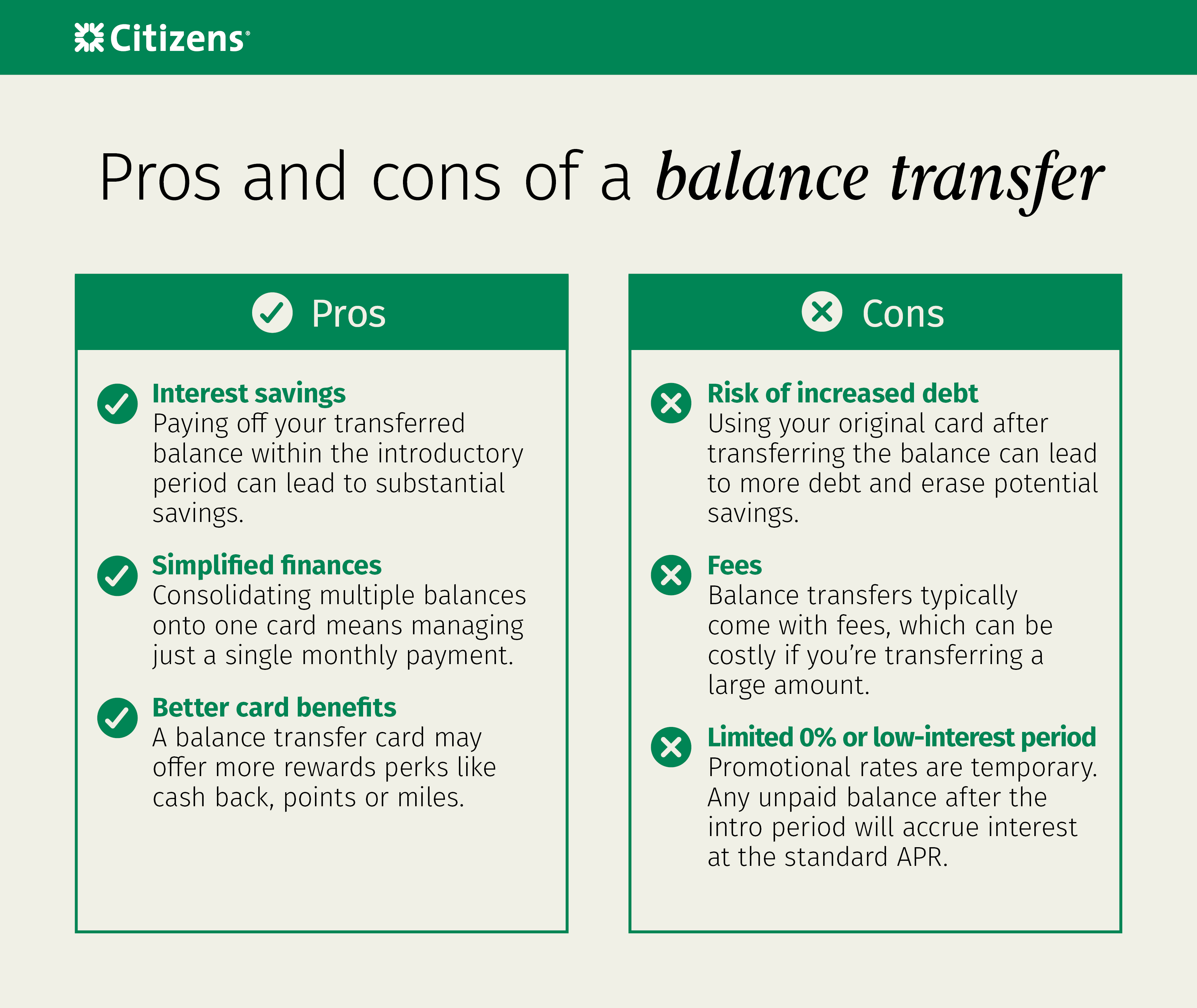

Balance transfer credit card pros and cons

Consider the pros and cons of balance transfer offers in general, and of specific balance transfer credit cards, before applying. Also, have a plan for how you're going to use the card during and after the promotional period to figure out which card will be the best fit.

How do credit card balance transfers work?

A balance transfer is a fairly straightforward process. From choosing the card to paying down your balance, research the best offer and then pay down your debt.

- Decide which credit card to use

If you already have credit cards, review your current cards for available balance transfer offers. Then, compare those offers with new credit cards with attractive intro APR offers. If you're applying for a new credit card, you'll submit your application. Once approved, you'll be able to initiate your balance transfer.

- Initiate your balance transfer

The simplest way to initiate a balance transfer is during the new account opening process or through your existing online credit card account. During the process, you'll indicate the card issuer, account number and balance you want to transfer to your new credit card. Once the process is complete, you'll typically receive a confirmation email from the credit card company receiving the transferred balances.

- Bide your time until the transfers go through

Transfers don't happen overnight, so patience is key. They can often take a few weeks to show on your account. Once complete, you'll see the transferred balance and the balance transfer fee noted in your account.

- Set up payments

Ideally, you'll want to pay down your transferred balance before the end of the promotional APR period. So if your promotional period is 12 months, you could set up an automatic monthly payment for one-twelfth of the balance.

- Keep your balance low

If you can pay down your entire transferred balance by the end of the promotional period, that's terrific. If you have a bit left to go, remember that the lower your balance, the more you'll save on interest. Try to keep your total balance at one-third of your credit limit or less for the best impact on your credit score.

What is a balance transfer fee?

Many balance transfer credit cards charge a balance transfer fee, a percentage of each balance transfer. The fee usually ranges from 3% to 5%, but sometimes it will be different during the initial window for balance transfer offers.

For example, if your card has a 5% fee and you transfer a $1,000 balance, your card will now have a $1,050 balance transfer balance. Although your balance increases, you can still come out ahead if the promotional APR saves you more than $50 in interest.

How does a balance transfer impact your credit score?

Opening a new credit card and transferring balances can impact your credit score in different ways.

It might hurt your credit score because:

- Applying for a new card can result in a hard inquiry.

- Opening a new account can decrease the average age of your credit accounts.

- Moving lots of balances to one credit card can lead to a high credit utilization rate on that card.

It might help your credit score because:

- Having more open credit accounts sometimes helps credit scores.

- You'll have more total available credit, which can lower your overall credit utilization rate.

- Paying off credit cards can help your score, even if you're moving the debt to a different credit card.

In the long run, the impact on your credit scores will largely depend on how you use and manage the credit card.

If you make your payments on time and slowly pay off the debt — without doing anything else that hurts your score — then your credit score may increase over time. If you miss payments or max out the credit cards that you transferred balances from, then your score might decrease over time.

Where can you find a balance transfer card?

To get the most bang for your buck, find a balance transfer credit card with a 0% introductory APR and a generous promotional term length. You can typically find cards with these features from a wide range of banks, each offering different features, rewards and more.

FAQs about balance transfer credit cards

While you don't need a particular credit score to make a balance transfer, your credit score may impact your qualification for balance transfer credit cards. A credit score of "good" or higher could boost your chances of qualifying for cards offering 0% APR balance transfer promotions.

Balance transfers aren't just for combining credit card debt. You can use balance transfer credit cards to lower your interest costs on multiple kinds of debt including:

- Car loans

- Personal loans

- Student loans

- Other high-interest debt

You can also use a balance transfer credit card that offers an introductory rate on purchases to finance gifting for the holidays or even a honeymoon. No matter your needs, you can find a credit card that can help turn life's "probables" into "possibles" — and at the lowest possible cost.

Once you complete your balance transfer, you don't need to close the old credit card. In fact, doing so could ding your credit. That's because credit scoring agencies consider the age of your oldest accounts when calculating your credit score. Keeping the account open could bode well for your score in the long run.

If you want to avoid temptation, you could lock the card away in a safety deposit box. At the very least, you can take it out of your physical and digital wallets. By doing so, you can help keep your credit score high and your debt in check.

When you transfer a balance from one credit card to another, the original card's balance decreases by the transfer amount. No matter the new balance on the original credit card, the account will remain open.

Considering a balance transfer credit card?

A balance transfer credit card might save you money and make managing your finances easier. However, you'll want to review the balance transfer offer's terms, consider the pros and cons and make sure a balance transfer is a good fit for your situation.

If you're ready to review a few options, check out the credit cards from Citizens to compare the cards' features and see which cards have balance transfer offers.

Related topics

How do cash back credit cards work?

What's the deal with cash back credit cards? Find out more about your options and why card companies offer rewards.

9 types of credit cards and how to choose one

Credit cards have different features and benefits. Find out the most common types of cards and how to choose the best one for your needs.

3 credit card habits to help build a solid credit score

Find out how you can use your credit card to increase your credit score.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Mastercard and the circles design are registered trademarks of Mastercard International Incorporated.

Credit Cards are issued by Citizens Bank, N.A. pursuant to license by Mastercard International Incorporated.

Disclaimer: The information contained herein is for informational purposes only as a service to the public, and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.