What is a CD ladder?

Key takeaways

- A CD ladder is a savings strategy that involves opening multiple certificates of deposit with different maturity dates, giving you regular access to your money as each CD matures.

- Unlike traditional savings accounts or money market accounts that have variable interest rates, CDs have fixed rates that vary based on the term length.

- You can build a CD ladder with short- or long-term CDs. A short-term CD allows you to take advantage of rising interest rates, while long-term CDs allow you to keep your current rate when rates are falling.

With a certificate of deposit (CD) ladder, you put your money into CDs with different term lengths to make the most of interest rates and to be able to access your funds more frequently.

A CD ladder can be a great way to save for the future. CDs typically earn a higher interest rate than traditional savings accounts or money market accounts. A CD ladder enables you to take advantage of benefits of short- and long-term CDs without tying up all your money.

Let's take a closer look at how CD ladders work and why you might consider building one.

How does a CD ladder work?

When you build a CD ladder, you open several CDs with staggered maturity dates. For example, you may open five CDs with the following terms:

- 12 months (1 year)

- 24 months (2 years)

- 36 months (3 years)

- 48 months (4 years)

- 60 months (5 years)

For each CD account, you deposit money and agree to leave it alone for a set term. When the first CD account matures after one year, you reinvest the money into a new 60-month CD account. The next year, when the 24-month CD matures, you'll reinvest that into another new 60-month CD.

With this laddering method example, you'll eventually end up with five 60-month CDs that are continuously coming to term, one per year. You've "laddered up" to the longest CD terms and rates while maintaining some liquidity by having annual access to the full balance of one of the account "rungs."

Instead of listing interest rates for their CDs, banks typically give the annual percentage yields (APY), or the total interest a CD will earn in a year, including the effects of compounding interest.

The APYs on CDs vary by term. Say the 12-month CD account pays 3.5% APY, and the 60-month account CD pays 4.5% APY. The remaining three CD rates will likely be between 3.5% and 4.5%.

Since you can't take money out of a CD before the term ends without paying an early withdrawal penalty, CDs typically offer higher interest rates than savings accounts or money market accounts. Usually, the longer the CD's term, the higher the interest rate it pays.

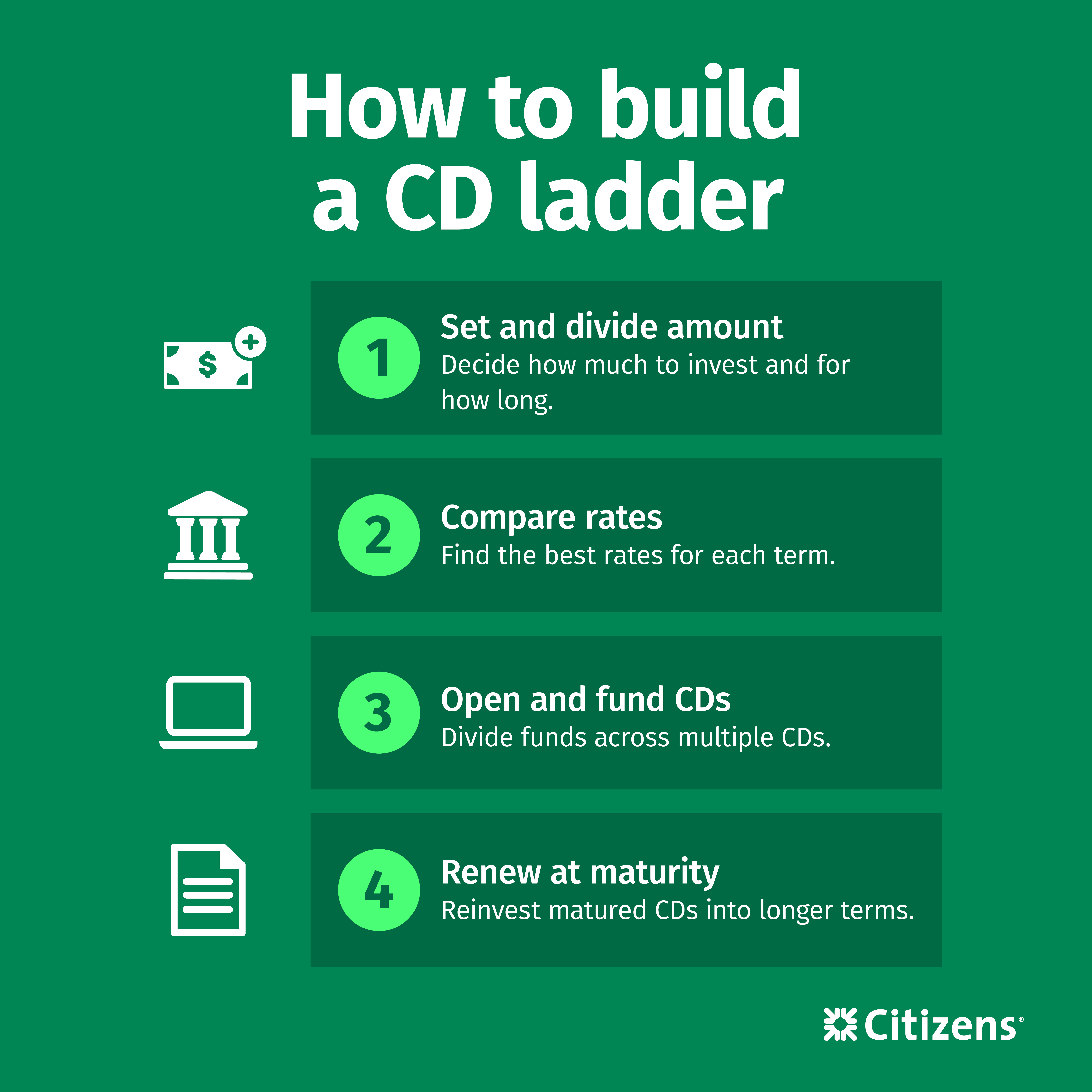

How to build a CD ladder

When building a CD ladder strategy, decide how much you want to invest and for how long. Look at your current savings, your budget and your financial goals to determine the size of your ladder.

Suppose you have $20,000 saved and want to buy a vacation home in about 10 years, meaning you want that money to keep working for you for at least a decade. You can build a CD ladder like this:

1. Divide your savings into equal amounts

If you're building a five-rung CD ladder with $20,000, you'll fund each CD account with $4,000.

2. Compare CD APYs from different banks

Shop around for the best CD APYs based on the term. Keep in mind that you don't have to open each CD account at the same institution. You may find a better APY at one bank on a 12-month CD account and a better APY at another on a 60-month CD account.

3. Open and fund the CDs

Once you’ve selected your CDs, you’ll need to open and fund them. Many banks let you do this online, or you can stop by a local branch. Be sure to gather your documents before applying to prevent delays.

Here’s what most banks require:

- Government-issued photo ID

- Social Security number or tax ID

- Address, phone number and other personal information

- Beneficiary information (optional)

You can fund each CD by writing a check or transferring funds from a bank account. Once the account is open, the bank representative will give you an account agreement. This document states your APY, term, the penalty for early withdrawal and the date the CD automatically renews. It also outlines the grace period when you can withdraw money after the CD term ends and before it automatically renews.

4. Renew the maturing CDs

Renew each CD account when it matures but pay attention to the term. When the first CD account matures after 12 months, renew it for a 60-month term so it moves to the top of your ladder. When the 24-month CD account matures, renew it for a 60-month term and so on.

What is an example of a CD ladder? Check out the below five-rung CD ladder, with varying terms, APYs and financial institutions:

| CD Number | Amount | Term | APY | Bank |

| 1 | $4,000 | 12 months | 3.50% | Bank A |

| 2 | $4,000 | 24 months | 3.75% | Bank A |

| 3 | $4,000 | 36 months | 4.25% | Bank B |

| 4 | $4,000 | 48 months | 4.25% | Bank B |

| 5 | $4,000 | 60 months | 4.50% | Bank A |

Benefits of a CD ladder

A CD ladder can be a flexible way to reach your financial goals. Instead of keeping your funds in a single long-term CD, you’ll have more frequent access to your cash.

Here are several CD ladder benefits:

- Fixed interest rates: With a typical savings or money market account, interest rates can rise or fall, and it’s hard to predict what might happen. With a CD, the interest rate is fixed for the term. This makes it easy to determine how much you’ll earn.

- Regular access to your cash: As each CD account renews, you can decide whether to renew it or withdraw the money. You can also choose shorter CD terms of three to six months if you think you’ll need your cash sooner.

- Flexibility: You can choose your CD ladder size and terms. You may decide to build a CD step stool with just two or three rungs, or build a ladder with CDs that renew at six months instead of 12 months. How much you put into each CD is also up to you.

- No annual fees: Unless you withdraw money before the maturity date, CDs typically don’t charge any fees.

- FDIC insurance: CDs are insured by the Federal Deposit Insurance Corporation for up to $250,000 per depositor at each bank.

Drawbacks of a CD ladder

A CD ladder isn’t always the best fit for everyone. It depends on your personal financial situation and goals. For some, the drawbacks could outweigh the benefits.

Here are potential negatives to consider:

- APYs may not be high: CD APYs are usually higher than savings accounts, but they may not match the potential return on the stock market.

- You lose access to your money for the term: Even if you choose short-term CDs of up to 12 months, you’ll need to leave your money alone during that time. Otherwise, you could face an early withdrawal penalty consisting of a few months of interest.

- You have to stay on top of the ladder: CD ladders are mostly set-it-and-forget-it, except when the maturity date rolls around. You’ll need to pay attention to those dates and decide what to do next.

- Beware of automatic renewals: After a CD matures, you’ll have a grace period of a few days before it automatically renews. During this time, you can withdraw your funds or reinvest in a new CD at the current APY. Banks typically send reminders before the maturity date to give you time to decide.

Additional CD ladder considerations

The CD ladder model is popular because it’s low-risk compared to the often volatile stock and bond markets. But that doesn’t mean it’s risk-free. Periods of high inflation or rising interest rates could make it harder to reach your financial goals.

Before opening a CD, consider the potential for inflation risk. This is when prices for goods and services increase at a faster rate than the interest you earn in a CD. High inflation reduces your purchasing power. For example, something that is $50 today could become $70 in just a few months. That means the money in your CD may not keep up with rising prices, even with the effects of compounding interest.

When you start building your CD ladder also matters. Interest rates rise and fall, and they are impossible to predict. If you start building a CD ladder when rates are rising, you could end up locked into a lower rate for the term. You’ll miss out on the higher interest rates you could’ve earned if you had waited.

Alternatives to a CD ladder

A CD isn’t the only way to grow your money. Another account or investment might be a better fit depending on your needs.

High-yield savings account

These savings accounts are mostly affiliated with online banks. Although CDs usually have higher APYs, high-yield savings accounts allow you to access your money without incurring an early withdrawal penalty.

Money market account

A money market account is both a savings account and a checking account. It typically earns a higher APY than a traditional savings account, but lower than CDs. Unlike with a CD, you can access your money market account funds whenever you need them.

Treasury Bills

A Treasury Bill (T-Bill) is a short-term security backed by the U.S. Treasury. It’s sold at a discount and redeemed at its face value at maturity. The return can sometimes outperform CDs, depending on the market. And just as you can build a CD ladder, you can also build a T-Bill ladder to take advantage of different maturity dates.

CD ladder FAQs

For more information on how CD ladders work, explore answers to some of the most frequently asked questions.

Is CD laddering a good idea?

Yes, CD laddering can be a good savings strategy if you want a predictable return on your money without the risk of locking up all of your savings for several years in longer-term CDs.

What is a mini CD ladder?

A mini CD ladder uses shorter-term CD accounts, such as three-month, six-month, nine-month and 12-month CDs, rather than one year or longer. It can be a useful strategy if you know you'll need to use your savings soon.

Can you build a CD ladder in a Roth IRA?

Yes, you can build a CD ladder in your Roth individual retirement account. Doing so may be particularly useful if you're approaching retirement age and want a more secure investment option.

Is a CD ladder better than a bond ladder?

It all depends on your goals. A bond ladder is similar to a CD ladder but uses bonds instead, which typically have longer terms. Bonds also aren't as secure as CDs, and the return isn't guaranteed. That said, the potential return can be higher with bonds than with CDs.

What happens when a CD matures in a ladder?

You can cash out the CD account at maturity or renew it.

What are the tax implications of a CD ladder?

You'll need to pay income tax on the interest your CD accounts earn when that interest gets credited to the accounts, usually at maturity.

Take advantage of a CD ladder

With a CD ladder, your money can earn a decent return while remaining somewhat liquid. Whether you're setting cash aside for a short-term or long-term goal, a CD ladder can give your savings a boost.

Interested in certificates of deposit and other ways to reach all your savings goals? Learn more about Citizens CD terms and rates and explore our savings account options for your financial needs.

Related topics

How many savings accounts should I have?

Saving for separate goals is easier with multiple savings accounts. Determine how many savings accounts you need to achieve your goals.

How a CD can help my financial plan

If you're saving for a future, long-term goal, a CD can be a useful tool. Read on to learn how a CD can help your financial plan.

How to start investing

Want to dip your toes into the stock or bond market? Check out our guide on how to start investing.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.