How to save for a house

Key takeaways

- Research home prices and work with a lender to determine how much you'll need for a down payment.

- Set a budget, find ways to cut spending and earn more income to save for a house faster.

- Savings account options with higher interest rates and savings tools can help you reach your home-buying goals.

Buying a new home is one of the most significant moments of your life, both personally and financially. Often, it can be a long road to saving for your down payment and other home loan costs. The following tips for how to save for a house can help you reach your goal of homeownership more quickly.

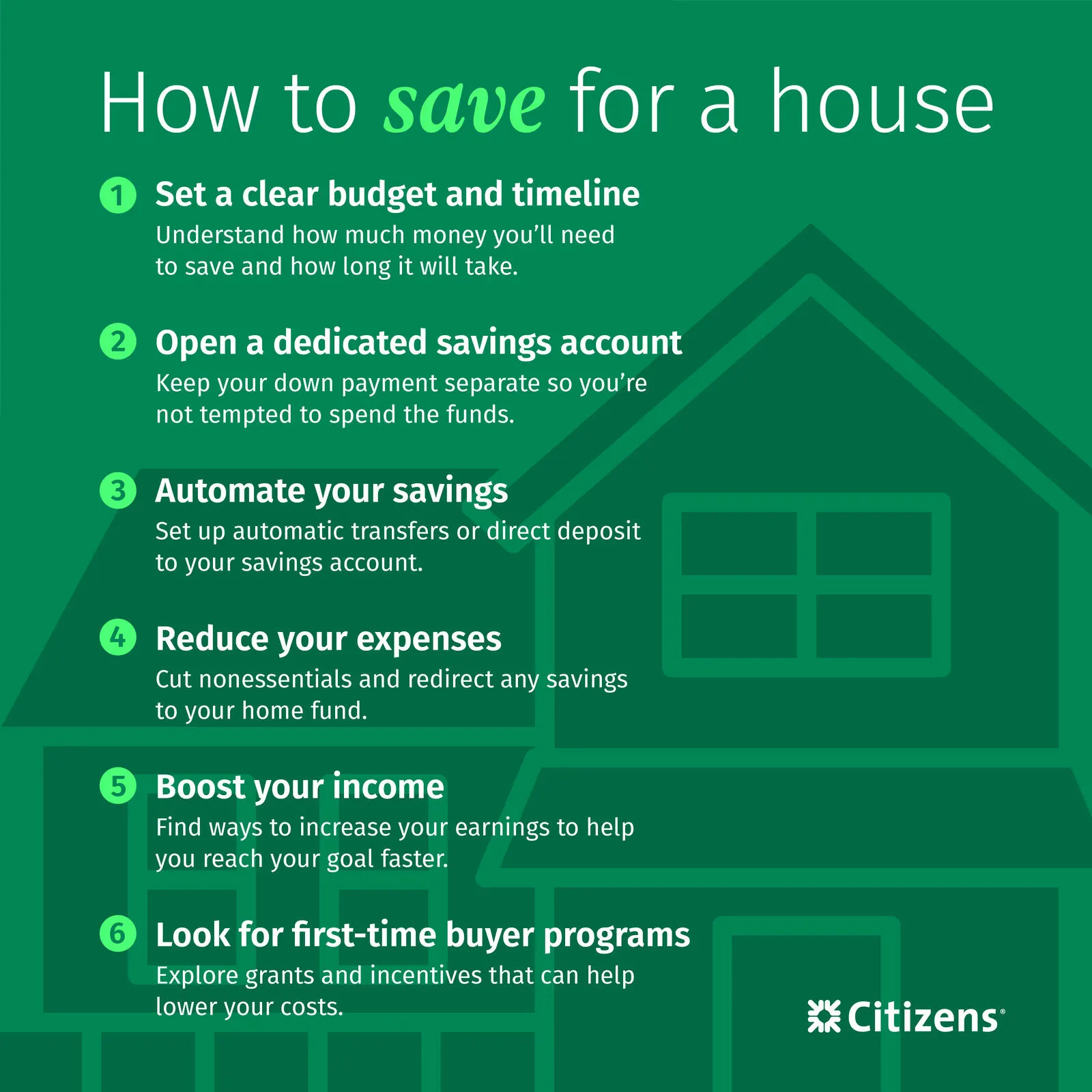

1. Set a clear budget and timeline

Before setting a budget and timeline, you'll have to consider your needs, like the number of bedrooms, square feet and proximity to schools, and wants, like a fireplace or a swimming pool, for your new home.

Then, research home prices in your area that meet your criteria. When you have an idea of the cost of your ideal house and how much you can afford, you can start calculating the down payment amount you'll need and how much your monthly payment will be.

How much money should you save before looking for a house?

To determine how much money to save before house hunting, you need to estimate potential down payment and closing costs, moving expenses and a reserve for unexpected costs:

- Down payment: 3.5%–20% of the purchase price

- Closing costs: typically, 2%–5% of the loan amount

- Moving expenses: typically, $500–$2,000 for local and $2,000–$5,000 for long-distance moves

- Reserve: 1%–3% of the home purchase price for repairs or other unexpected expenses

Working with a lender early in the process can help you determine the home price and mortgage payment you can afford, as well as additional closing costs and mortgage insurance expenses you may need to account for. Your home budget should also factor in any costs for renovations, upkeep and utilities, which could impact your price range.

Next, evaluate your monthly budget and calculate how long it will take you to save. For example, if you need a $50,000 down payment and already have $15,000 saved, you'll still need $35,000. If you're currently putting away $1,500 a month, it will take you two more years.

Want to move into your new home faster? You may have to make concessions on your wants and needs to find a more affordable home. If you still need to make some adjustments, the following tips can help you get to your savings goal faster.

2. Open a dedicated savings account

A dedicated house savings account separate from your checking and other savings goals makes it easy to track your progress and prevents you from accidentally spending your money on unrelated purchases. A separate account also makes it easier to document your assets when it's time to apply for a mortgage.

Three popular savings account options include:

High-yield savings accounts

A high-yield savings account offers higher interest rates than traditional savings accounts, which can help your savings grow faster. However, it often requires a higher minimum balance. Unlike a CD, your funds are accessible when you need them, although some banks may have monthly withdrawal limits.

Certificate of deposit (CD) accounts

CDs offer fixed interest rates that are often higher than traditional savings accounts. In exchange for a higher rate, you agree to keep your money in the account for a set term, ranging from a few months to several years. If you withdraw funds before the term ends (the maturity date), you'll incur an early withdrawal penalty, which typically consists of a few months of interest.

Money market accounts

Money market accounts combine the features of checking and savings accounts. They typically offer higher interest rates than savings accounts, and they may also come with limited check-writing privileges. These accounts often have higher minimum balance requirements than traditional savings accounts, and some banks may limit the number of withdrawals you can make each month.

3. Automate savings

A simple way to stay on track when saving money for a house is to automate your savings. This ensures your account continues to grow over time, even if you're busy and forget to make deposits. You can set up automatic account transfers in person, through online banking or in a mobile banking app.

Three tools you can use to automate include:

- Direct deposit: Deposit a set amount from your paychecks into your savings account each month.

- Automatic transfers: Schedule monthly transfers from your checking account into your savings account. You can choose the amount and frequency.

- Citizens Savings Tracker®: Set and track savings goals, and use automated savings options to grow your balance.

When you're saving for a home, you may be tempted to dip into your retirement savings or emergency fund to buy a home sooner. However, it's important to leave the money in those accounts and continue making regular contributions.

Withdrawing money from a retirement account may result in taxes and financial penalties. It also makes it harder to reach your retirement goals. If you use your emergency fund, you may have to rely on credit cards or other debt if an unexpected need arises.

4. Reduce your expenses

Saving for a house may seem like a large goal, but cutting back on existing monthly expenses can make a big difference. Small steps like packing a lunch or skipping your morning latte may help you get started, but don't forget to look at other aspects of your lifestyle.

For example, you may consider moving to a less expensive apartment, using public transportation to save money on gas or canceling monthly streaming subscriptions. Make sure you reallocate those savings toward your down payment goal.

5. Boost your income

A side job earning extra income can give you more money to put toward saving for a home. If your schedule allows, look for part-time work on nights and weekends, such as reselling, dog walking, babysitting, food delivery or freelancing. Even if you can't work consistently, one-time gigs or money-making hobbies can help boost your progress toward your home savings goal.

6. Look for first-time homebuyer programs

First-time homebuyer programs from states and the federal government can help low- and moderate-income families become homeowners.

These programs offer down payment grants or home loans with down payment requirements lower than those for conventional loans, reducing how much you need to save. Some loans require mortgage insurance, guarantee fees and funding fees.

Programs that help first-time homebuyers include:

- State programs: Many states and local governments offer down payment assistance grants or forgivable loans for first-time buyers, but those who haven't owned a house in a few years may also qualify. Check the National Council of State Housing Agencies for opportunities where you live.

- FHA loans: Partially backed by the Federal Housing Administration, FHA loans may have minimum down payment requirements as low as 3.5%. They also have more flexible credit requirements than conventional loans, making it easier for buyers with limited credit histories to qualify.

- USDA loans: Partially backed by the U.S. Department of Agriculture, USDA loans are popular because you don't need a down payment, they have flexible credit requirements, and you can finance 100% of the purchase price. You must meet income requirements, and the home must be in an eligible rural or semi-rural area to qualify.

- VA loans: Partially backed by the U.S. Department of Veterans Affairs, VA loans have flexible credit requirements and don't require mortgage insurance. They help veterans, active-duty service members and some surviving spouses buy a home with no down payment. To qualify, applicants must obtain a Certificate of Eligibility (COE) from the VA.

Start saving for your new home

Learning how to save for a house can help you feel more confident and motivated to reach your financial goals. Explore Citizens' savings account options and choose a way to save for a new home that's right for you.

Related topics

First-time homebuyer tips

Buying a home for the first time can be intimidating. Explore eight first-time homebuyer tips to help you understand the home-buying process.

How to improve your credit score before buying a home

Learn practical ways you can improve your credit score to help you get approved for a mortgage.

Buying a home: The down payment myth

Discover the pros and cons of a low-down payment mortgage to help determine if you really need a 20% down payment when buying a home.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only, as a service to the public, and is not legal advice or a substitute for legal counsel, nor does it constitute advertising or a solicitation. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.