I was planning to retire next year. Now what?

Ask an Advisor is a series in which people receive complimentary, personalized feedback from a Citizens Wealth Advisor. The following financial advice is for informational purposes only and doesn't take into account personal or financial information not submitted to the Financial Advisor.

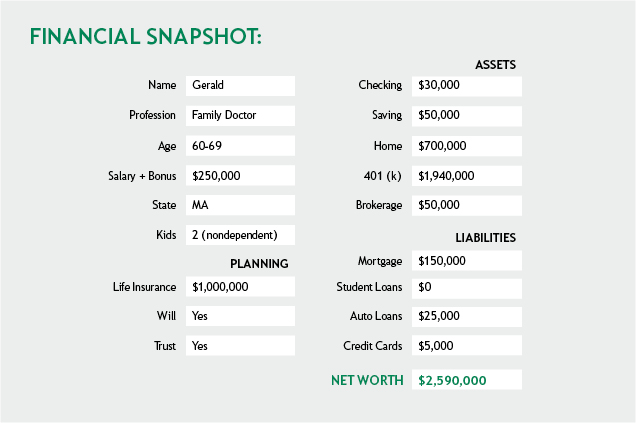

Gerard, from Massachusetts, writes:

I promised my wife I was going to retire next year. I was looking forward to it, actually. There are so many movies I've wanted to catch up on. I'm 66 and I already have worked two years more than I was planning to. My sons are both professionals and left home long ago. In fact, we're expecting our first grandson in November.

Then COVID-19 hit. Both kids lost their jobs and we helped them for a couple of months. To make things worse, my wife was furloughed from her job at a local university. We had to dip into our retirement funds and now I'm not certain I can stop working. We have a healthy 401(k) of almost $2 million, but our savings were nearly wiped out, with only $50,000 left.

Can I still retire next year?

A financial advisor's viewpoint

While retirement has become increasingly uncertain in the current climate, it's not unattainable. The first step is to create a post-retirement budget and see if you can cover it. Your ability to meet your obligations is critical to even consider retiring.

1. Aim for 70% of your pre-retirement income

The rule of thumb on how much Americans in their 60s should have in their retirement accounts is 8 to 10 times their annual salary. The majority of workers don't come close to reaching that number. In fact, one-third of near-retirees (ages 55 to 64) don't have a pension or a 401(k).

Considering all your assets, Gerald, you and your wife are on the right track.

More than amounts, you need to think in percentages. Most advisors believe your retirement income should be around 70% of your pre-retirement salary. You make $250,000 a year, so you should aim for $175,000 a year in retirement income.

While 401(k) plans vary, if your plan averages an annual return between 5% to 8%, you're probably in good shape. Right now the value of your 401(k) is $1,940,000, so you're looking at returns between $97,000 and $155,200 (estimate). The average pension in the state of Massachusetts in 2018 was $37,310 and I suspect a family doctor like you would be paid much more. Plus, there's your wife's pension and Social Security to consider.

2. The spend-down and cash cushion strategies

Retirement spend-down refers to your strategy to spend, decumulate or withdraw assets. Retirees are advised to spend down their taxable assets first (bank accounts, stocks, non-retirement savings in general), tax-deferred assets second [401(k), IRAs], and tax-free accounts last.

The principle behind this approach is that in all likelihood, you have already paid taxes on your non-retirement savings. This means some or all of your assets may come back to you as a tax-free return of your own money, and you'll end up with a lower tax bill. Also, you can access these savings at any age without having to deal with penalties.

The cash cushion that already served you well by compensating for your wife's loss of income, can help you absorb any losses in your portfolio or deal with tax payments. We recommend a standard savings account with the equivalent of at least a year of living expenses. You won't gather much on interest but the cash cushion will give you some peace of mind and may empower you to be as aggressive as you want with your investments.

3. Turn bad debt into good debt

Debt doesn't have to stop you from retiring, as long as it's the right kind. Good debt — the money owed for things that can build wealth — is something you can carry into retirement (mortgages, car loans).

In turn, bad debt (credit cards, high-interest consumer loans) is something near-retirees should aggressively pay down. Otherwise it will eat away your retirement income.

In your particular case, you only have $5,000 in credit card debt. Tighten your budget in this final year to get your credit card debt off your plate.

4. Be prepared

While the economy may go through ebbs and flows during your retirement, the most likely surprises that you'll face are health-related costs. The typical 65-year-old couple will spend an average of $295,000 in health care for the remainder of their lives.

Even if you're eligible for Medicare or opt for Part B or C (meaning paying a premium), you will still have to pay for dental, vision and long-term care out of pocket. You should consider a private insurance plan to cover those needs.

First, review your existing Medicare plan and evaluate if you have the right level of coverage. If you decide to change plans, be sure to compare prices through medicare.gov.

Then, start a health savings account immediately. Not only the money you contribute is tax deductible, earnings and withdrawals are not taxed, as long as they're for health care expenses.

Lastly, consider long-term care insurance, so you'll have the funds to cover assisted living, nursing home or at-home care. Most of these policies will help you deal with the cost of care from two to five years or longer.

5. One final push

In short, Gerald, retirement in one year is feasible for you and your wife, but will require an aggressive savings attitude. Eliminate your bad debt, bring your 401(k) to at least $2,000,000, and since your children are no longer living with you, consider downsizing from the family home to a condo. It could free up to $300,000 you can use for a cash cushion and a health savings account.

How does Gerald compare to his peers?

With a net worth of almost $2.6 million, Gerald is in better shape than most of his peers. The median retirement savings for Americans in their 60s is $172,000.

Ready to find a Citizens Wealth Advisor?

Can I afford to send my child to a private college anymore?

Should I start collecting social security?

How to keep costs down and rebuild in 2021

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: Views expressed may not necessarily reflect those of Citizens. The information contained herein is for informational purposes only as a service to the public, and is not legal advice or a substitute for legal counsel, nor does it constitute advertising or a solicitation. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.

Citizens Wealth Management is comprised of both banking and brokerage affiliated companies.

Securities, Insurance and Investment Advisory Services offered through Citizens Securities, Inc. (“CSI”). Citizens Securities, Inc. is an SEC registered investment advisor and Member – FINRA and SIPC. One Citizens Bank Way, Johnston, RI 02919. (800) 942-8300. Citizens Securities, Inc. is an affiliate of Citizens Bank, N.A.

Please be aware that the security products offered are different from those offered by a bank and are subject to investment risk, including possible loss of principal amount invested.

Securities, Insurance Products and Investment Advisory Services are:

· NOT FDIC INSURED · NOT BANK GUARANTEED · MAY LOSE VALUE · NOT A DEPOSIT · NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY