Maximum cash-out refinance amount: Calculate how much you can borrow

Key takeaways

- Funds from a cash-out refinance can be used for many needs, including major life events, consolidating debt, unexpected expenses, education costs and more.

- Several factors affect the maximum cash-out refinance amount you can borrow, including your credit score, debt payments, type of property and the type of loan.

- The closing costs for a cash-out refinance may reduce the amount of cash you receive, although some lenders may allow you to roll them into the new loan.

Qualifying homeowners may use a cash-out refinance to get a better rate on their mortgage and access cash for another need. Because the loan is secured by the equity in your home, the interest rate is often lower than other financing options, like credit cards and personal loans.

Lenders often use the 80% loan-to-value (LTV) standard to determine the maximum cash-out refinance amount you can borrow. Although it may sound complex, the 80% LTV is actually very easy to calculate. You can quickly crunch the numbers to see if a cash-out refi fits your needs.

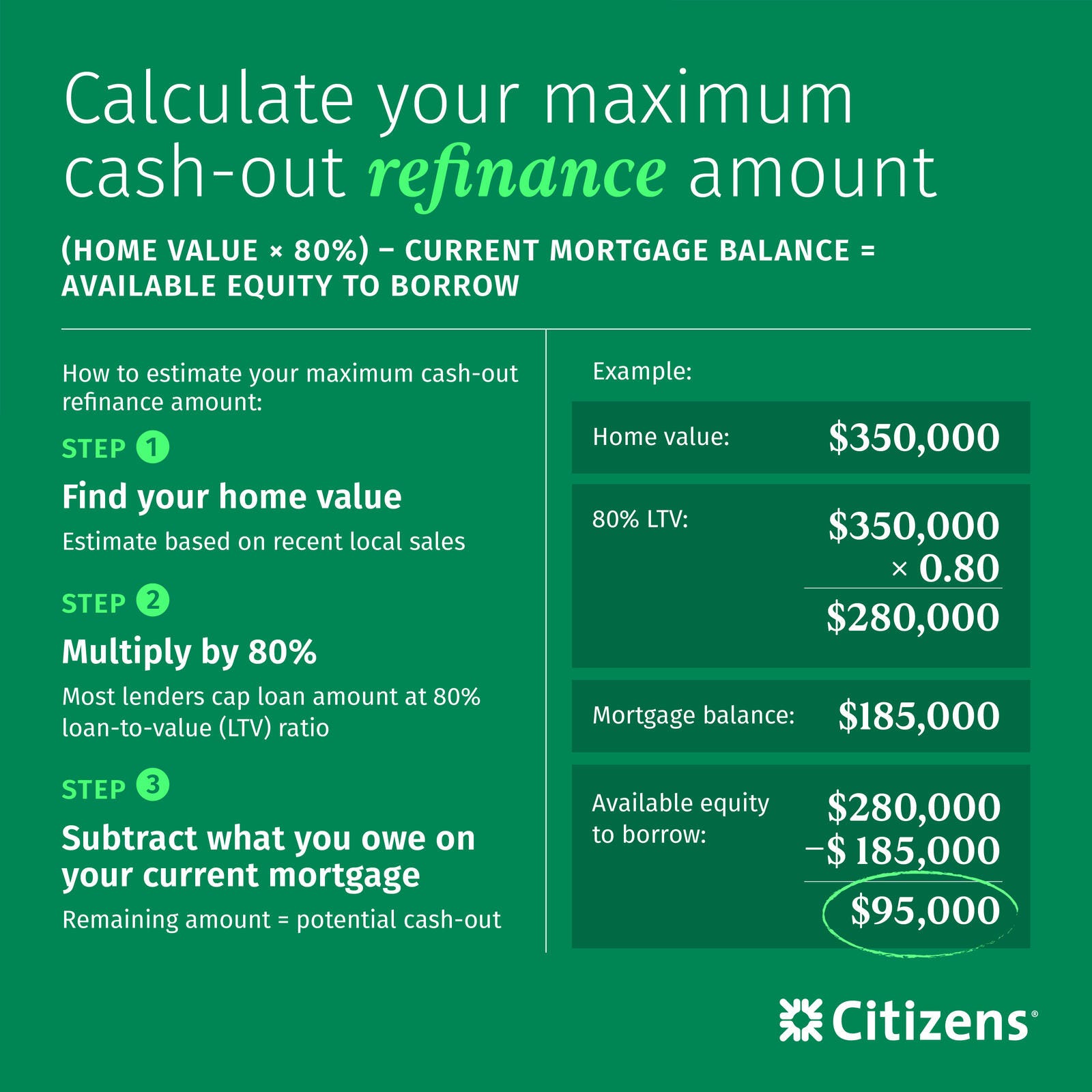

The cash-out refinance calculation formula

The formula for the 80% LTV standard is straightforward:

(Home value × 80%) – Current mortgage balance = Estimated cash-out amount

Here are the steps to determine how much you can borrow:

1. Determine the value of your home

Check the listings for similar homes in your community that have recently sold to estimate your home's current market value.

2. Multiply by 80%

Multiply the current market value of your home by 0.80.

3. Subtract your current mortgage balance

Subtract the amount from Step 2 from what you still owe on your mortgage to determine the approximate cash-out loan amount before closing costs.

Most lenders use the 80% threshold for conventional loans with cash-out refinances to reduce their risk. They often require that you leave at least 20% equity in your home after the refinance to act as a buffer in case the value of your home decreases. For example, if your home value drops by 10%, the loan amount still hasn't exceeded what your home is worth.

Real calculation examples

A helpful way to see how the cash-out refinance formula is calculated is with some practical examples. Closing costs are typically 2% to 5% of the loan amount and may be added to the new loan or deducted from the cash-out you receive, depending on the lender.

Here are three scenarios that assume you are borrowing the maximum cash-out refinance amount.

Scenario #1

Home value: $350,000

80% LTV: $280,000 ($350,000 × 0.80)

Current Mortgage balance: $185,000

Estimated cash-out amount: $95,000 ($280,000 – $185,000)

New loan amount: $280,000 ($185,000 + $95,000)

3% Closing costs: $8,400 ($280,000 × 0.03)

Cash received after closing costs: $86,600 ($95,000 - $8,400)

Scenario #2

Home value: $400,000

80% LTV (max loan): $320,000 ($400,000 × 0.80)

Current Mortgage balance: $250,000

Maximum available equity before costs: $70,000($320,000 - $250,000)

Estimated closing costs financed into loan(2%): $6,400 ($320,000 × 0.02)

New loan amount: $326,400 ($250000 + $70,000 + $6,400)

Estimated cash received: $70,000

This example is for illustration purposes only. Estimated closing costs shown are financed into the loan and reduce the amount of cash received. Actual amounts may vary.

Scenario #3

Home value: $250,000

80% LTV: $200,000 ($250,000 × 0.80)

Current Mortgage balance: $50,000

Estimated cash-out amount:: $150,000 ($200,000 - $50,000)

New loan amount: $200,000 ($50,000 + $150,000)

4% Closing costs: $8,000 ($200,000 × 0.04)

Cash received after closing costs: $142,000 ($150,000 - $8,000)

Factors that affect your borrowing limit

Additional factors influence your maximum LTV ratio and final approval amount for a cash-out refinance.

- Credit score: Lenders will check your credit score to see how you've handled debt in the past.

- Debt-to-income (DTI) ratio: Your DTI is a comparison of your gross monthly income to your monthly debt payments, will also be reviewed. Lenders typically prefer DTI ratios of 43% or less to ensure you aren't overextended.

- Type of property: Primary residences typically qualify for higher LTVs, while second homes and investment properties often have lower LTV caps.

- Type of home loan: The type of home you choose also influences the maximum LTV and the final loan amount. Conventional and FHA loans usually have a maximum LTV of 80%, while VA loans may have a maximum LTV of 90%.

What homeowners typically use cash-out refinance funds for

Cash-out refinance funds can be used for nearly anything. There are usually no restrictions on what you can do with the money you borrow. Common uses include:

- Debt consolidation: A cash-out refinance may have a lower interest rate than credit cards, personal loans and other financing.

- Home improvements: Funds can be used to renovate, remodel or build an addition to your home.

- Education expenses: A cash-out refinance may have a lower interest rate than a private student loan.

- Emergency funds: Some borrowers save their funds in an emergency savings account for unexpected expenses.

- Investment opportunities: Funds can be used to cover new business startup costs or the purchase of an investment property.

Understanding the true cost of accessing your equity

Accessing the equity in your home with a cash-out refinance typically comes with closing costs of 2% to 5% of the loan amount. Depending on your needs, another financing option that doesn't have closing costs, like a personal loan or credit card, may be a better fit.

Tax implications can vary depending on how cash-out refinance funds are used. Homeowners may want to consult a tax advisor to understand how using the funds could affect mortgage interest deductibility.

When you replace your mortgage, your new loan will likely have a different interest rate. A cash-out refinance may be worth it if rates have dropped at least 1% to 2%. This helps to ensure the potential benefits outweigh the costs.

Refinancing can also extend your loan term. A higher loan balance that you are taking longer to repay may increase your mortgage payments and the total interest paid over the life of the loan.

Determining if the calculated amount meets your needs

Before you apply for a cash-out refinance, consider whether the amount you can borrow justifies the closing costs. Also, determine whether you comfortably afford the new monthly payment to make sure it fits your financial goals and budget.

Also, consider whether a different type of financing would be better suited for your needs. If interest rates haven't dropped much, you can still access your equity with a home equity loan or home equity line of credit (HELOC) without replacing your mortgage. Talking to your lender can help you determine which financing option best fits your needs.

Borrow more with a cash-out refinance

Ready to explore your options? See how refinancing with Citizens could help you achieve your financial goals. Explore mortgage refinance options from Citizens.

Related topics

5 steps of the mortgage refinance process

Learn the five key steps of the mortgage refinancing process, from preparing your application to closing on your new loan.

Should I do a cash-out refinance?

Learn when a cash-out refi makes sense, including key financial conditions, common use cases and factors to consider before tapping your home equity.

5 smart ways to use cash-out refi funds

From home improvements to debt consolidation, learn how to decide which options make the most sense when you get a cash-out refi.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Mortgages are offered and originated by Citizens Bank, N.A. (NMLS ID 433960).

Disclaimer: Views expressed may not necessarily reflect those of Citizens. The information contained herein is for informational purposes only, as a service to the public, and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.