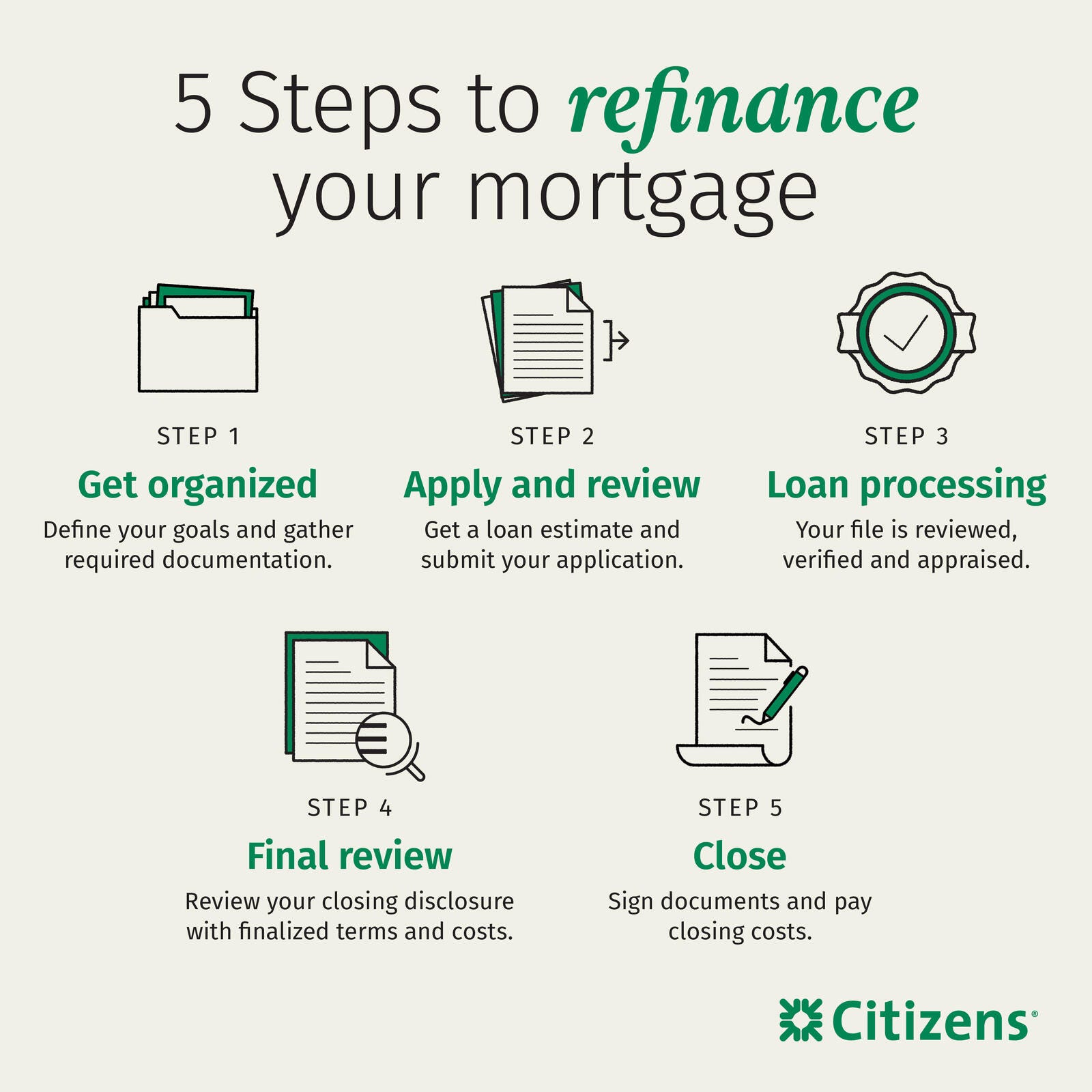

5 Steps of the mortgage refinance process

Key takeaways

- Refinancing your mortgage follows a structured process that includes preparation, application, underwriting and closing.

- You will need to provide documentation that shows your income, assets and ability to manage a new mortgage when you apply to refinance.

- Final loan documents outline the costs to refinance clearly before closing, so you can review important details in advance.

Refinancing a mortgage can feel like a big step, especially if it has been years since you last applied for a home loan. The good news is that refinancing follows a structured and predictable process. Each stage builds upon the last, from preparing your financial information to closing on your new loan. Once you understand how the refinance process works, you can set realistic expectations, stay organized and keep the process on track from start to finish.

Step 1: Get organized and prepare your information

Strong preparation sets the foundation for a smooth refinance. Lenders evaluate your financial profile when you apply to refinance your mortgage, so gathering documents early may help you avoid delays later in the process.

The checklist below can help you prepare key documentation.

- Pay stubs and W-2s

- Tax returns

- Bank statements and asset records

- Investment and retirement income documentation

- Current mortgage details

Before applying, it's important to clearly define your goal. Some homeowners pursue a cash-out refinance to lower monthly payments or adjust their loan term, while others want to access home equity for purposes such as consolidating debt, funding home improvements, or supporting other financial priorities. Understanding how you plan to use your cash-out refinance funds and evaluating whether a cash-out refinance is the right option for your situation can help you make a more informed decision. Taking time to prepare upfront can also help you avoid unnecessary delays and keep the refinance process moving smoothly from the start.

Step 2: Apply and review your loan details

The refinance application process follows many of the same steps you completed when you first purchased your home. You submit personal, financial and mortgage information, and your lender evaluates your request. Your credit profile also plays a role in the terms you receive, so reviewing your credit score ahead of time can help you know where you stand.

After you apply, your lender provides you with a loan estimate along with other required disclosures. The loan estimate outlines key details about your new loan, such as your interest rate, monthly payment and estimated closing costs. Lenders must provide this document within three business days after receiving your application, which gives you an early look at the total cost of the loan.

Take time to review these details carefully before moving forward. Interest rates can change daily, so you will also need to decide when to lock in your rate and confirm that timing and terms work for your situation.

Tax implications can vary depending on how cash-out refinance funds are used. Homeowners may want to consult a tax advisor to understand how using the funds could affect mortgage interest deductibility.

Step 3: Processing, underwriting and appraisal

This stage of the mortgage refinance process involves several professionals who help move your loan toward completion. Each plays an important role in verifying your information and assessing borrower risk.

- Loan processor: Collects and organizes your documentation

- Underwriter: Reviews credit, income, assets and debts, then decides whether to approve the loan

- Appraiser: Estimates your home's market value

- Title company: Confirms the property has no outstanding liens

- Insurance provider: Verifies coverage for the home

This phase often takes the most time when you refinance your home because lenders may request additional documentation. Staying responsive can help you keep the process on track.

Step 4: Review final numbers and prepare to close

As your loan reaches the final stage, your lender provides a closing disclosure that outlines your finalized costs, credits, fees, projected monthly payment and loan terms. This document reflects the most accurate version of your loan details based on confirmed numbers.

Federal guidelines require lenders to provide this disclosure for at least three business days before closing. Use this time to review the details carefully, confirm how much cash you may need at closing and make sure everything aligns with your expectations.

Step 5: Close on your new loan and transition

Closing completes your mortgage refinance. During this step, you review and sign your final loan documents and pay any required closing costs. Your lender or closing agent will walk you through the paperwork and answer any questions so you understand the terms of your new home loan.

Once closing is complete, your new mortgage replaces your old loan. The funds from your refinance pay off your original mortgage, and your new loan takes its place. You will then begin making payments based on the new terms, with your first payment typically due the following month.

What to keep in mind throughout the process

Staying organized and responsive can help you move through each step in the refinance process more smoothly. Lenders rely on accurate and timely information to finalize your loan. Keeping your long-term financial goals in focus can also help you determine whether refinancing supports your broader plans.

Get started with your refinance today

Refinancing gives you the opportunity to adjust your mortgage so it better fits your financial goals. Understanding each step in the mortgage refinance process can help you stay organized, make informed decisions and move forward more efficiently.

Explore your options with Citizens and get started with your refinance today

Related topics

Maximum cash-out refinance amount

Calculate your cash-out refinance amount using the 80% LTV rule and discover common uses for the funds.

Should I do a cash-out refinance?

Learn when a cash-out refi makes sense, including key financial conditions, common use cases and factors to consider before tapping your home equity.

5 smart ways to use cash-out refi funds

From home improvements to debt consolidation, learn how to decide which options make the most sense when you get a cash-out refi.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Mortgages are offered and originated by Citizens Bank, N.A. (NMLS ID# 433960). All loans are subject to approval.

Disclaimer: The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.