HELOC, personal loan, or credit card. Which option is best for you?

By Kate Gillan | Citizens Staff

Key takeaways

- There are several differences between HELOCs, personal loans and credit cards.

- HELOCs have been gaining in popularity as home values have risen.

- Reviewing the pros and cons of financing can help you determine the best choice.

You may be about to embark on a home renovation, pay for education, or make your home eco-friendly with solar panels or better insulation. When financing is needed, it can help to do a gut-check as to which option is right for your unique situation. But with so many options out there, how do you know which is right for you? Let's get some clarity by looking into three main financing sources: HELOCs (home equity lines of credit), personal loans and credit cards. After doing some research, you'll hopefully feel more confident around your choice.

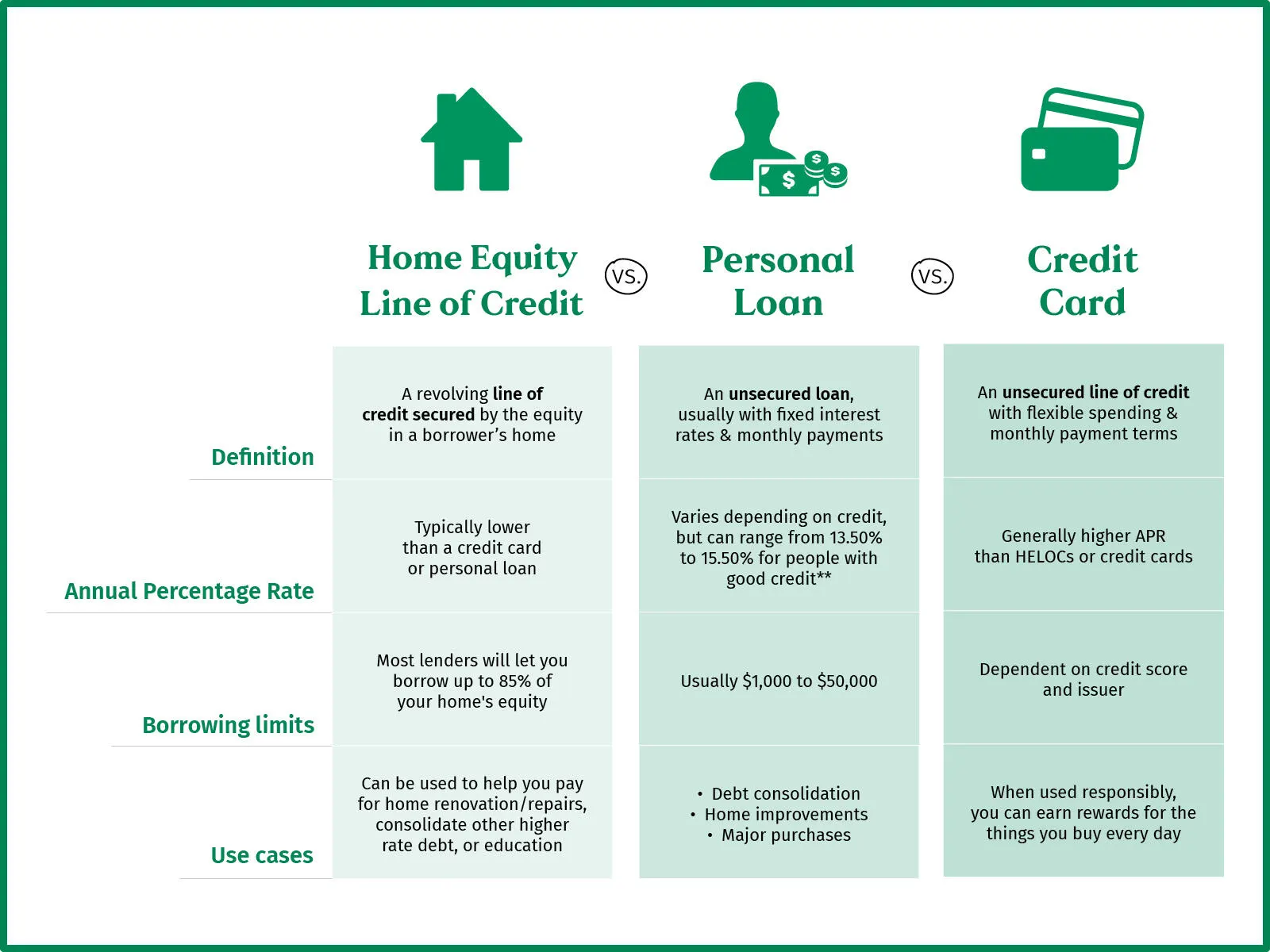

What are the main differences between a HELOC, personal loan and a credit card?

Some main differences between a home equity line of credit, a personal loan and a credit card are interest rates, repayment terms, fees and loan amounts. It can help to map out the blueprint of the exact terms in each choice when making decisions that can affect future goals. Here's how the three types of funding break down:

HELOC: A HELOC is a line of credit where you borrow money against the equity in your home. You may have heard that the popularity of HELOCs has been rising along with home values. Another term for a HELOC is a second mortgage, which essentially places a lien on your home. A general rule of thumb for how much equity is needed to get a HELOC, it's 20%, though some institutions differ on that figure. HELOCs usually come with lower APRs (annual percentage rates) than credit cards or personal loans, but there may be annual fees involved. To calculate how much equity you have in your home, you simply take the difference between the value of your home and what you still owe on your mortgage. Once you've determined the full amount of equity, you may or may not be able to borrow the full amount. The loan-to-value (LTV) ratio is your current loan balance divided by the appraised value of your home. An LTV of 80% is considered ideal by many financial institutions. This means they won't let you carry debt that is more than 80% of your home's value. This debt includes your current mortgage as well as the new loan or line of credit.

Personal Loan: With a personal loan, you're borrowing a specific lump sum of cash that is then paid back over a determined period of time, usually between two and five years. Also, the interest rate is fixed. Personal loans are unsecured (meaning your house is not used as collateral as it would be with a HELOC) and can be used for any purpose the borrower chooses, including consolidating debt or covering the cost of a large expense. Really, it's up to the borrower as to how they wish to use the loan.

Credit Card: A credit card, issued by a bank or institution, allows you to borrow money on a rolling basis with a variable interest rate to pay for goods or services. If you don't pay your bill in full every month, your remaining balance carries over. The kicker? Credit card interest is generally much higher than it is with a HELOC or personal loan.

To break things down simply, let's compare personal loans, home equity lines of credit and credit cards with a visual. It could help you decide which option is right for your life.

You may be wondering, when it comes to financing, what's the best option? Only you can determine which method is correct for your situation, but here are some practical uses for each.

When to use a HELOC: A HELOC is generally used for a home renovation, a large repair not covered by your homeowner's insurance, or a second home. HELOCs can also be used to consolidate higher rate debt, or free up cash for your life goals. If you're looking for a lower APR, you might want to consider a HELOC. Another reason some people use a HELOC is because they wish to "age in place," or remain in their home after retirement which may require renovations to make your home safe and accessible. A HELOC allows them to borrow against the equity they've gained in their home and provides more choices for the homeowner.

When to use a personal loan: It's fairly simple — Are you looking to cover a one-time expense and know the exact amount needed to achieve your goal? A personal loan might work best here, as you can borrow as little as $500. Some reasons why you might decide to use a personal loan are consolidating credit card debt, travel or medical expenses.

When to use a credit card: Credit cards with a 0% APR introductory offer might appeal to you, as they offer a flexible line of credit instead of a lump sum of money like you'd receive with a personal loan. When used responsibly, credit cards allow you to earn cash back or rewards for the things you buy every day.

Consider the pros and cons for each option

HELOC pros and cons:

Pros: With a HELOC, you have flexibility because you may qualify for a certain line of credit or amount of money, but you don't have to use it all. You just borrow what you need instead of taking all the funds right away and then (bummer alert!) pay interest on the full amount. It's also possible that with a HELOC, one can deduct interest when making IRS-eligible home improvements. If you're thinking of taking out a HELOC, be sure to discuss tax implications with a financial professional.

Cons: A HELOC is a lien on your house, so be sure you only withdraw what you need and can pay the money back to avoid foreclosure. Also, your rate can change based on market conditions over the life of the loan.

Personal loan pros and cons:

Pros: A personal loan might work best for those who are more risk averse. As mentioned, they are unsecured loans, which means your house isn't set up as collateral against the loan. You may need a new car, or an unexpected medical expense could pop up that isn't covered by insurance. A personal loan is a term loan, meaning you pay it back over a period of time with fixed monthly payments and a fixed rate.

Cons: If your credit score isn't quite up to par just yet, it might not be in your best interests to take out a personal loan because your desired amount exceeds your loan limit or you may be looking at a high APR. Also, the terms of the loan might be shorter than with HELOCs, so you'll have less time to pay the money back.

Credit card pros and cons:

Pros: With a credit card, you borrow what you need on a rolling basis, and funds are available when you need them. They're convenient and secured by banks and institutions. You might earn points or miles. Plus, paying your balance in full monthly can increase your credit rating.

Cons: If you are unable to pay your balance in full every month, you will begin to accumulate interest on the unpaid balance. In turn, your APR is variable, so it could increase. According to the NY Federal Reserve, in the second quarter of 2023, Americans carried $1.03 trillion in debt.1 That's a lot of zeroes! With a credit card, rates are typically higher than with a HELOC or personal loan. While paying off your balance monthly is a good thing, carrying a balance is not, and will eat into your budget.

The choice is yours

With the current economic landscape of higher interest rates, people are using their equity to improve their homes rather than buy a home. Home equity lines of credit can be an attractive asset for homeowners and provide financial flexibility to help you achieve your life goals. But in the end, it's up to you to determine what works best. From a HELOC to a personal loan to a credit card, it's important to weigh all the choices to determine what's right for you and your financial goals.

1 Total Household Debt Reaches $17.06 Trillion in Q2 2023; Credit Card Debt Exceeds $1 Trillion, New York Fed, Aug. 08, 2023

Related topics

Streamline high-interest debt

If you own your home, rising home values mean that you may have access to a home equity line of credit (HELOC), which could make your existing debt easier to manage.

Made ready to renovate

If you own your home, rising home values mean that you may have access to a home equity line of credit (HELOC), which could make your existing debt easier to manage.

Empower your life with a HELOC

Your home is many things — shelter, gathering place and comfort zone. It's also one of your most valuable assets. With a home equity line of credit (HELOC), you can tap into the equity you've built up in your home to take care of projects or consolidate debt.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public, and is not legal advice or a substitute for legal counsel, nor does it constitute advertising or a solicitation. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.

Home equity lines of credit are offered and originated by Citizens Bank, N.A. (NMLS ID#433960). Citizens corporate headquarters: One Citizens Plaza, Providence, RI 02903.