What is APR on a credit card?

Key takeaways

- Annual percentage rate (APR) refers to the yearly interest rate you'll pay if you carry a balance on your credit card.

- Some credit cards have variable APRs, meaning your rate can go up or down depending on market conditions.

- Check to see if your credit card's APR is tied to a promotional or introductory rate; your APR could go up after the introductory period ends.

What is APR on a credit card? Your credit card's annual percentage rate (APR) is the yearly interest rate you're charged, including any fees. The card's APR will depend on your credit history and the card.

Whether you're looking for a card to use for your routine expenses or want a card for a major purchase (like a new sofa or laptop), your credit card APR is a key consideration to keep in mind. Read on to learn more.

What to know about credit card APR

The APR (annual percentage rate) on a credit card represents the yearly cost of borrowing money when you carry a balance. It includes the interest rate and, in some cases, additional fees like an annual fee. The higher your APR, the more expensive it is to maintain a balance on your card. Several factors influence how APR works and how much you end up paying, — including how interest is calculated, whether your rate is fixed or variable and your credit score.

Here's what to keep in mind when considering a credit card's APR:

- Annual fee: A credit card's APR is typically the same as its interest rate, unless your card charges an annual fee, which is then factored into the APR.

- Credit score: Credit card companies take your credit score into account when setting your APR, with a higher credit score generally translating to a lower interest rate.

- Compounding interest: Compound interest on a credit card is the interest calculated not only on your unpaid balance but also on the interest that has already been added to that balance. Credit card companies typically calculate the interest you owe daily, using your daily average balance for your monthly billing period.

- Grace period: Most credit cards offer a grace period. This period is the time between the end of the credit card's billing cycle and the day your minimum payment is due. During the grace period, the credit card company doesn't charge you interest. If you pay off the balance by the payment due date, no interest accrues.

- Fixed vs. variable rates: Credit cards often have a variable APR, meaning your rate can go up or down over time. Variable APRs are tied to an underlying index, such as the federal prime rate, which is the lowest interest rate at which banks will lend money. If the prime rate increases, your card's APR will also likely increase, and vice versa if the prime rate goes down. In contrast, a fixed-rate APR will remain the same from the time you open the credit card account. APRs may also vary by credit card; it's possible to have one card with an APR of 19%, and another with a rate of 25%.

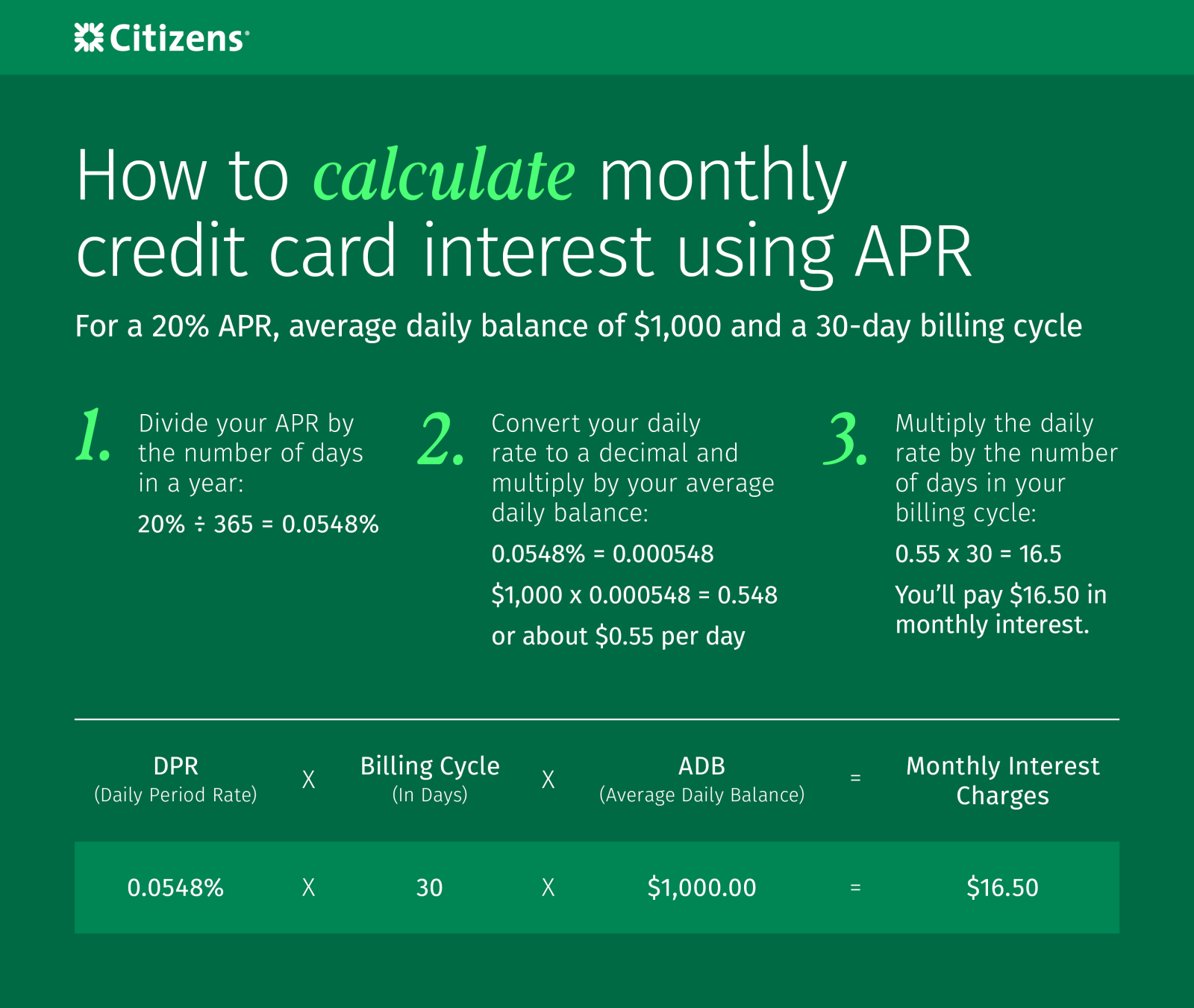

How to calculate credit card interest using APR

To calculate how much interest you'll pay on a credit card, you need to know how often your interest is compounded in addition to your APR. Credit cards usually charge daily compound interest, using your daily average balance for your monthly billing period.

If your card charges an annual fee, you'll have to read the fine print to find your interest rate without the fee factored in.

When you know the APR or interest rate on your credit card, you can use it to calculate how much you may have to pay on a balance. To do that, you'll need to figure out the daily periodic rate, or how much credit card interest you're charged per day on your balance.

Say you owe $1,000 on a card with a 20% APR. Here's how to figure out how much you'll actually pay:

- Divide 20% by 365, the number of days in a year: 20% ÷ 365. You'll get 0.0548% as a daily rate.

- Convert your daily rate to a decimal. Multiply the daily rate by the balance you owe: 0.000548 x 1,000. You'll get 0.548, or about 55 cents per day.

- Multiply the daily rate by the number of days in your billing cycle. If you have a 30-day billing cycle, multiply 0.55 by 30. On a $1,000 balance with a 20% APR, you'll pay $16.50 in interest for that billing period.

What is a “good” APR for a credit card?

What is considered a "good" APR depends on your credit, typical credit card use and economic conditions. While some cards may advertise 0% APR, those offers are promotional APRs that only apply to certain transactions for a limited time. For example, a card may offer 0% APR on balance transfers for six months. After that, the purchase APR applies.

Five years ago, it was possible to find credit cards with purchase APRs under 15%. Today, most cards have APRs over 20%, and users with poor credit can expect APRs over 30%.

In general, the lowest credit card APRs are available to those with excellent credit. When comparing card options, also consider the following factors:

- Fees: Some cards charge annual fees that you have to pay regardless of how you use the card.

- Rewards: With some cards, you can earn cash back, airline miles or points on purchases. You can redeem those rewards for cash back, travel, gift cards or merchandise.

How to lower your APR

If you have a credit card with a high APR, you may have options for lowering it:

- Improve your credit score: Credit card companies typically offer better rates to people with higher credit scores. Make payments on time and avoid opening multiple accounts at once to keep your score trending upward. If you're behind on any credit cards or loans, get current on your payments to increase your score.

- Open a card with a balance transfer offer: Card companies occasionally offer promotional balance transfer APRs to encourage people to open new cards. If you carry a balance on a card with a high APR, it can be worthwhile to open a balance transfer card and take advantage of the lower rate. With a lower rate, you can reduce how much interest builds and potentially pay off your debt faster.

Types of APR on credit cards

Your credit card may charge a different APR depending on how you use it. For example, some credit cards have a separate APR for balance transfers, which may be higher or lower than the standard APR. The APR on cash advances is usually considerably higher than for standard card purchases. If you pay late or otherwise violate the terms of your card agreement, you may have to pay a penalty APR.

Examples of credit card APR include:

- Purchase APR: The purchase APR is the interest you pay on standard purchases when you carry a balance.

- Cash advance APR: If you use your credit card to get cash, you'll typically pay a separate, higher APR that doesn't have a grace period.

- Balance transfer APR: You can transfer a balance from one card to another. When you do, you'll usually pay a different APR on the transferred amount, often for a limited time. Some cards offer a lower APR for balance transfers to entice you to switch.

- Promotional or introductory APR: Credit cards sometimes offer a promotional or introductory APR, such as 0%, to encourage you to open a new account. The promotional rate may apply to new purchases for the first few months or year that you have the card.

- Penalty APR: If you pay late or miss two or more payments, your card issuer may charge you a penalty APR, which is often much higher than the purchase APR. (Setting up recurring monthly payments or payment alert reminders can help you avoid late payments.)

Read the terms and conditions closely when signing up for a new credit card. The card offer should include a table with rates and fees that make it easy to see your APR.

Understand APR when you apply for a new credit card

As with any financial agreement, familiarize yourself with your credit card's terms and conditions, including its APR. Remember that the higher your balance, the more interest you’ll pay. Keeping your balance low can help you save on this expense.

Selecting the right credit card shouldn't be complicated. Learn about all our credit card options and how we're ready to help you reach your money goals. Whether you want to earn cash back rewards or transfer a balance, find the card that will fit your lifestyle and needs.

Related topics

How do cash back credit cards work?

What's the deal with cash back credit cards? Find out more about your options and why card companies offer rewards.

How to build your credit score

If you're looking to open a credit card to establish a credit history, here are three habits that can help you build a solid score.

6 credit card tips for all users

A cash back credit card gives you rewards with every purchase. Make the most of your credit card rewards and get the maximum cash back.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Credit Cards are issued by Citizens Bank, N.A. pursuant to license by Mastercard International Incorporated.

Disclaimer: The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.