Building a Business Succession Plan: Everything You Need to Know

By Mark Valentino, Head of Business Banking | Citizens

Key takeaways

- Start early. Business succession planning works best when it begins three to five years before a transition. This timeline allows for building leadership depth, optimizing tax and estate plans, and building operational independence.

- Strengthen business value. A well-executed succession plan demonstrates to potential successors, buyers and lenders that the business is financially sound, operationally independent, and ready to perform under new ownership.

- Find expert help. A Citizens survey found that 52% of businesses plan to use expert help for valuation and transition at some point1. A business banker can assemble an advisory team with experience in similar transactions.

Most business owners spend years building a company but not enough time planning how to transition it. Citizens found that 51% of businesses with $5M+ in annual revenue are planning for a succession path, yet more than half have no plan in place to guide it.

A well-executed succession plan does more than just map out a leadership transition. It actively strengthens a business by ensuring operational independence, solidifying management, and applying experts to the task of planning for financing, tax, legal and estate considerations.

Business owners with the best succession outcomes start planning early.

What are the succession options?

One of the first questions business owners ask is how they can structure a succession. A range of choices exist to fit owner preference, business situation and financial goals, but they are not all widely understood. That knowledge gap matters: A lack of clarity about what is possible keeps some owners from planning at all. In fact, research shows that roughly one-third of business owners have not made a succession plan simply because they have not identified a suitable successor.2

Internal transitions

| Empty cell | What it is | What to know |

| Family ownership transition | Transfers leadership and ownership to the next generation. | Requires integration with estate planning to avoid unintended tax consequences and inheritance and wealth distribution disputes. |

| Executive and leadership team succession | Ownership transitions within the existing management team. | Provides continuity for employees and customers but requires a structured equity or buy-sell agreement to define how ownership transfers and at what value. |

| Management buyout | The management team purchases the business from the current owner. | Provides strong leadership continuity since buyers already know the business. Requires careful structuring to manage the conflict of interest that arises when managers are both operators and prospective buyers. |

| Employee stock ownership plan (ESOP) | Employees gradually acquire ownership through a company-funded retirement trust. | Rewards loyal employees and can provide meaningful tax advantages for the selling owner but requires specialized legal, tax and financing expertise to structure properly. |

External transitions

| Empty cell | What it is | What to know |

| Sale to strategic buyers | Sale to a company that values the business’s customers, capabilities or market position. | May command a premium valuation but typically requires clean financials, streamlined operations, and updated technology and equipment. |

| Sale to financial buyers | Sale to private equity firms or family offices, usually involving a post-sale partnership with existing management. | Private equity buyers typically plan to grow and resell within 3-7 years while family offices often prefer to hold longer term. |

Hybrid and partial options

| Empty cell | What it is | What to know |

| Minority investment and recapitalization | Allows owners to realize partial liquidity while retaining control by bringing in an outside investor. | Provides access to capital and expertise without a full exit but involves complex financing decisions that benefit from experienced advisor guidance. |

| Hybrid and staged succession | Owner delegates operational responsibilities first, then transfers ownership gradually over time through equity sales or buy-sell agreements. | Reduces transition risk by allowing incoming leaders to develop fully before a complete ownership transfer occurs. |

For owners whose succession path involves a sale to an outside buyer, exploring exit strategy options and the preparation and process involved in selling a business are important to understand.

Important factors to any succession plan

The right succession option depends on a variety of factors related to the current owner and the business. Business owners and their advisors will arrive at this selection together, but owners who take the time to familiarize themselves with important inputs will be better prepared to contribute meaningfully to the process when it begins.

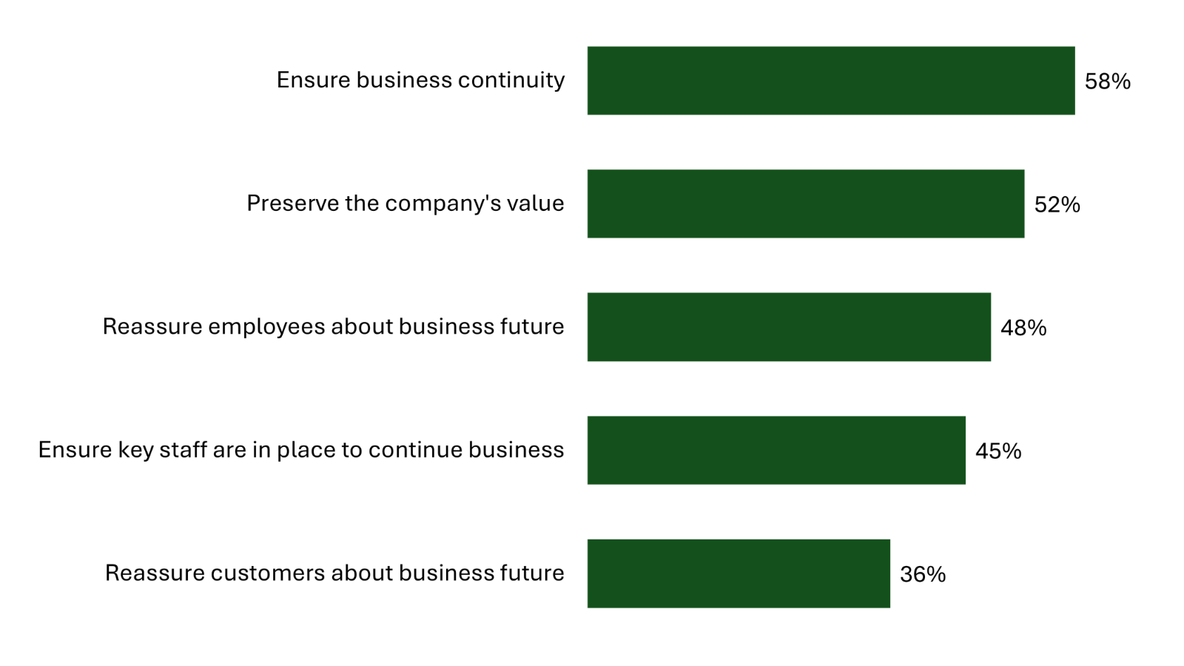

Ownership and personal goals. Succession planning starts with clarity on what a business owner wants to achieve. To make goals actionable, they should be tied to measurable outcomes like valuation targets, timeline, and the owner’s financial and personal objectives.

Among businesses with $5M+ in revenue planning for succession, the Citizens survey found the following priorities1:

Business valuation. A mismatch between what an owner believes the business is worth and what the market will pay is common going into succession planning. A formal business valuation from an M&A advisor, certified business valuator, or investment banker may set realistic expectations and determine how much preparation time is needed before a business transition.

Tax, estate, and legal considerations. How a succession is structured directly affects what an owner keeps. Asset versus stock sale treatment, entity structure, buy-sell agreements, and estate planning decisions should all be evaluated early with a CPA and attorney before a path is chosen.

Succession path. Successors can be internal, external or a combination of the two. The right choice of path is impacted by the owner’s desire for a clean exit versus ongoing involvement, the financial and operational readiness of the business, the status of current leadership, timeline, and the financial outcome each option is likely to produce.

Personal financial readiness. For most owners, the value locked in their business represents a significant part of their personal net worth. Whether expected proceeds align with the owner’s long-term financial goals and post-succession plans is a foundational question that should be answered before committing to any path.

How to build a succession plan, step by step

The most essential element of succession planning is also one that is easily overlooked: starting early. Some owners recognize this is imperative and are taking action. Among the businesses in the Citizens survey considering an ownership transfer, most began the process within the past one to three years, a timeline that reflects the depth of preparation a successful succession requires.

Knowing the steps can lead toward better advanced preparation.

Step 1: Build a team of advisors. Succession planning involves business operations, legal structure, tax planning, and personal wealth management, so it requires a team of specialists. The right team includes an M&A advisor, a transaction attorney, a CPA, and a wealth advisor. A business banker who understands your company can help to find advisors who are experts in succession planning and have worked with similar companies.

Citizens data finds that businesses understand the need for a broad base of help. When asked who they will turn to for advice, the top five choices are: 3

- An attorney or law firm

- A CPA or accounting firm

- A financial advisor

- A business banker

- A business consultant

Step 2: Build a capital and liquidity plan. Many succession paths require financing, whether it’s to fund a buyout, refresh equipment or manage working capital. Owners should assess the right mix of credit and term loans well in advance, and stress test cash flow under multiple scenarios to confirm the business can sustain itself through the transition without a liquidity squeeze. A business banker is a valuable early resource, both for structuring the right financing approach and for stress testing assumptions before commitments are made.

Step 3: Determine business value. A formal valuation early in the process grounds every subsequent decision in reality. Business value is shaped by earnings quality, revenue consistency, management independence and operational strength, and a formal valuation identifies where gaps exist and how much time may be needed to close them before pursuing a transition. Owners who understand their valuation before entering the process are better positioned to set realistic goals, choose the right path and negotiate from a position of strength.

Step 4: Solidify company leadership. Identifying and developing leadership, codifying critical roles, establishing cross training and mentorship tracks, and linking compensation to readiness milestones all strengthen the business for whatever succession path is ultimately chosen. How leadership transitions are communicated to employees and customers deserves careful attention since uncertainty can affect morale, decision-making and client confidence.

Step 5: Optimize tax, estate and legal structure. The tax implications of a succession are highly dependent on how the transaction is structured. Asset versus stock sale treatment, buy-sell agreements, trusts, and entity structure all affect what an owner keeps. These decisions should be modeled with a CPA and estate attorney two to three years before a planned transition, when the most options are still available. Legal documentation is equally important, to protect both the owner and the business if circumstances change unexpectedly. Governance structures that establish clear decision-making authority in a family succession can prevent disputes that derail even well-planned transitions.

Step 6: Build a business that runs without you. A business that runs well without its current owner is worth more and transitions more smoothly. Documenting core processes, clearly assigning key customer relationships to specific team members, and having a clear plan for maintaining service levels during the transition all reduce risk for the owner and any incoming leadership or buyer. Reviewing and aligning insurance coverage, including policies that protect the business if a key person becomes unavailable and coverage that addresses potential revenue loss during the transition, helps protect a business against unexpected disruptions during what is often a vulnerable period.

How business succession planning impacts value

Succession planning does more than ensure a smooth handoff. It can directly affect what a business is worth to buyers, lenders, and successors because business succession planning:

- Reduces perceived risk. Businesses with a documented succession plan and a capable leadership team are viewed as lower-risk investments, supporting higher valuation multiples across all succession scenarios.

- Demonstrates operational independence. A business that runs without its current owner commands a higher valuation because buyers and successors have confidence that performance will continue through a transition.

- Preserves customer and employee relationships. A well-planned succession signals to employees that their future is secure and to customers that service will continue without disruption, both of which protect revenue and can contribute to higher valuation.

- Creates competitive advantage in a sale. Businesses with clean financials, documented processes and a prepared leadership team attract more buyers, generate more competitive offers, and close transactions faster.

How successful business owners plan for what comes next

The business owners who achieve the strongest succession outcomes share a few things in common. They start earlier than they think they need to, they take the time to understand their options and the steps involved, and they build the right team to guide the financial, legal and personal decisions along the way. Without a plan, options narrow, and the value built through years of hard work can be harder to protect. The best time to start is well before you think you need to.

Thinking about what's next for your business?

Related topics

Why it pays to know what your business is worth

Learn why understanding your business’s value is so important.

Building your business exit strategy: 5 questions to ask yourself

Learn how five key questions can help shape your business exit strategy.

Self-employed retirement plans: 6 options to consider

What are your retirement plan options if you’re self employed?

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

1 Citizens 2025 Business Survey

2 An online survey of 500 SMB principals at U.S. companies with 1-500 employees fielded August 20-September 2, 2025, conducted by Bredin.

3 Citizens 2026 Q1 Small & Midsize Business Outlook

Disclaimer: Views expressed may not necessarily reflect those of Citizens. The information contained herein is for informational purposes only, as a service to the public, and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.