What is a checking account and how does it work?

Key takeaways

- Checking accounts offer a secure way to store your money that you can then withdraw or spend using a debit card, send money electronically, access cash at ATMs and, when needed, write checks.

- A checking account can make it easier to responsibly budget and manage your finances with tools and features like mobile banking.

- In many cases, checking accounts are free or have low fees, and you can often avoid additional charges.

A checking account is a type of bank account designed for everyday use. It allows you to easily deposit, withdraw, transfer and send money to others electronically (such as through bank transfers or person-to-person payments like Zelle®). Tools like debit cards, digital banking and electronic transfers make managing your funds simple and convenient. Here's a closer look at how checking accounts work.

What does a checking account do?

With a checking account, also known as a demand deposit account, you can deposit money with your bank that you can later withdraw or use checks or a debit card to pay others use a debit card, send money electronically, access cash at ATMs and write checks. It gives you a secure place to store your cash and other payments made to you, and you can easily access and spend this money when needed.

You can open a checking account in person or online. Once you deposit money in the account, you can usually access it right away. Your account enables you to make an ATM withdrawal and use checks or a debit card to make payments and purchases.

A checking account also gives you a system to track your income and expenses. You can start simplifying your personal finances with money management tools like direct deposit, recurring bill payments and mobile banking.

Why should you have a checking account?

Checking accounts can provide a convenient and secure way to store your money. They're also considered an important part of proving your financial health, as a checking account gives you a documented track record of responsibly managing your cash and can help with budgeting. Some top reasons to have a checking account:

- Allows direct deposit of your paychecks, providing near-instant access to funds

- Eliminates the need to carry or store a lot of cash, ensuring your money's safety and security

- Helps account for your income and expenses via bank-prepared statements and online banking

- Gives you the ability to easily handle electronic transfers to and from your account on a day-to-day basis

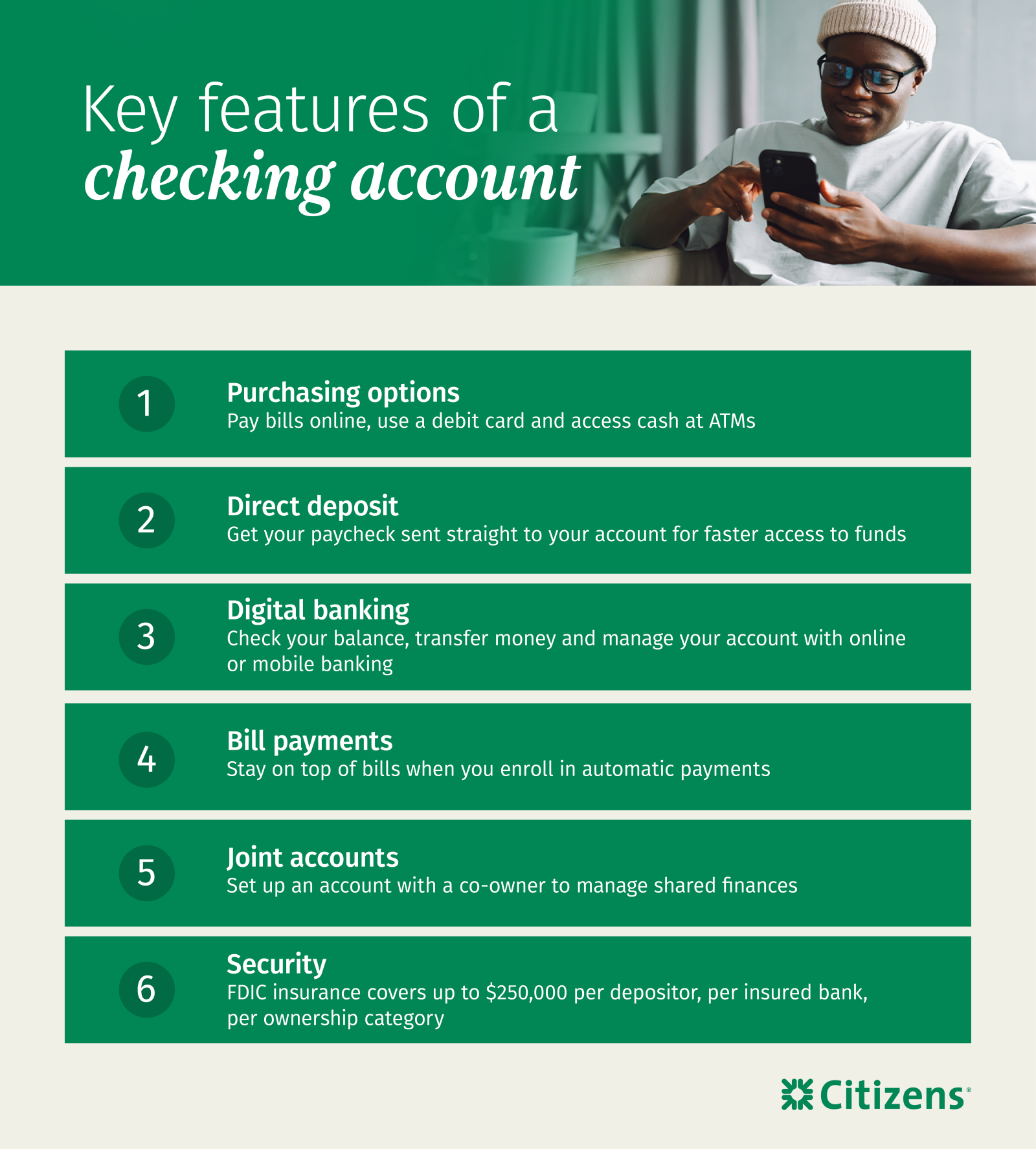

Key features of a checking account

While financial institutions may have different offerings, checking accounts generally share several standard features, such as:

- Convenient spending: Use a debit card to make transactions, send money electronically, access funds at ATMs and, when needed, write checks.

- Direct deposit: Set your paycheck to go directly into your checking account for near-instant access to funds.

- Mobile and online banking: View your account online or via a mobile app, where you can check your current balance, transfer money and review recent transactions.

- Money management: Set up recurring payments to pay bills (including recurring or online bill pay) from your checking account and transfer available funds between accounts and institutions.

- Joint checking: Designate co-owners on a joint checking account who can also access the account funds to simplify shared finances.

- Security: Keep your money secure with an account at an FDIC-affiliated institution, where your money is insured up to $250,000.

What are the fees for a checking account?

Checking accounts may have associated bank fees for certain activities. In most cases, you can avoid stacking up a lot of charges by paying attention to account requirements.

Maintenance fees

Some checking accounts have monthly maintenance fees for not regularly using your account or not maintaining a specific balance. To avoid or waive these types of maintenance fees, you can:

- Keep the minimum balance in the account

- Set up a recurring direct deposit

- Make a certain number of debit card purchases each month

Overdraft and NSF fees

An overdraft charge or non-sufficient funds (NSF) fee occurs when you spend more money than what's available in your checking account. In these cases, the bank may charge two fees:

- One for overextending your account balance

- One for having to decline a transaction or return a check

You can usually avoid overdraft fees by enrolling in overdraft protection, which automatically transfers funds from another account or line of credit to cover the difference.

ATM fees

Your debit card allows you to access your money and make certain transactions at ATMs. You typically won't be charged a fee when you use an ATM that's owned by your bank or is in its network. Other ATMs may cost you a few extra dollars in out-of-network ATM fees. To minimize these fees, aim to use your bank's ATMs whenever possible.

What is a checking vs. savings account?

Generally, you use checking accounts for incoming and outgoing transactions and savings accounts for holding and growing money. Most checking accounts don't offer interest like savings accounts, and savings accounts often limit the number of withdrawals you can make per month. The chart below outlines the differences between checking and savings accounts.

| Empty cell | Checking account | Savings account |

|---|---|---|

| Comes with a debit card | Usually | Not often but you may get an ATM card |

| Allows you to make purchases | Yes | No |

| Pays interest | Sometimes — may be available on specialty or high-balance accounts | Always — rates and APY vary by institution and account type |

| Can use checks | Yes | No |

| Online account access | Yes | Yes |

| Minimum balance requirement | Usually | Usually |

| Limits on withdrawals or transfers | No | Sometimes |

Checking account FAQs

Here are answers to some commonly asked questions about checking accounts.

A checking account is a place to store your money, and a debit card is a tool to access and use that money. With a debit card, you can make withdrawals and deposits at ATMs. You can also make purchases in person and online.

Yes, banks may offer a variety of checking accounts. In addition to a standard checking account, they may have student checking accounts for young adults, premium accounts for customers eligible for loyalty perks or low-balance accounts for people who don't make many transactions or need to prove they can keep an account in good standing.

No, banks don't usually allow you to deposit checks made payable to someone else, including when there are joint payees but the account isn't a joint account. It's possible to have someone sign over a paper check to you by indicating a new payee in the endorsement area on the back of the check, but not all banks accept this.

Yes, FDIC-insured* banks protect up to $250,000 per account ownership type.

Getting started with a checking account

Citizens has several checking account options with features like easy account access via our Citizens mobile banking app**. Find one that meets your needs.

Related topics

How to choose a checking account

Explore the different types of checking accounts to find the best fit for you and your financial goals.

8 bank fees explained and how to avoid them

Discover common bank fees and some practical tips you can use to avoid them.

6 tips to get the most from your checking account

From alerts to automatic payments to direct deposits, get the most out of your checking account with these tips.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public, and is not legal advice or a substitute for legal counsel, nor does it constitute advertising or a solicitation. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.

** Wireless carrier, text and/or data charges may apply.

* FDIC insurance up to the maximum amount allowed by law.