Checking vs. savings account: What's the difference?

Key takeaways

- Checking and savings accounts both allow you to manage and access your money, but they have several key differences that make each account ideal for specific goals.

- Most checking accounts don't earn interest like savings accounts. Keeping money in a savings account lets you take advantage of compound interest.

- With a savings account, you can access your money by transferring it to your checking account or making ATM withdrawals.

Checking and savings accounts serve different purposes, which is why many people have both types of accounts. You use a checking account to manage your daily expenses, and a savings account to grow your savings or set aside money for an emergency fund. Let’s take a closer look at checking and savings accounts to understand how they work, explore their features and benefits and see how they can help you reach your financial and savings goals.

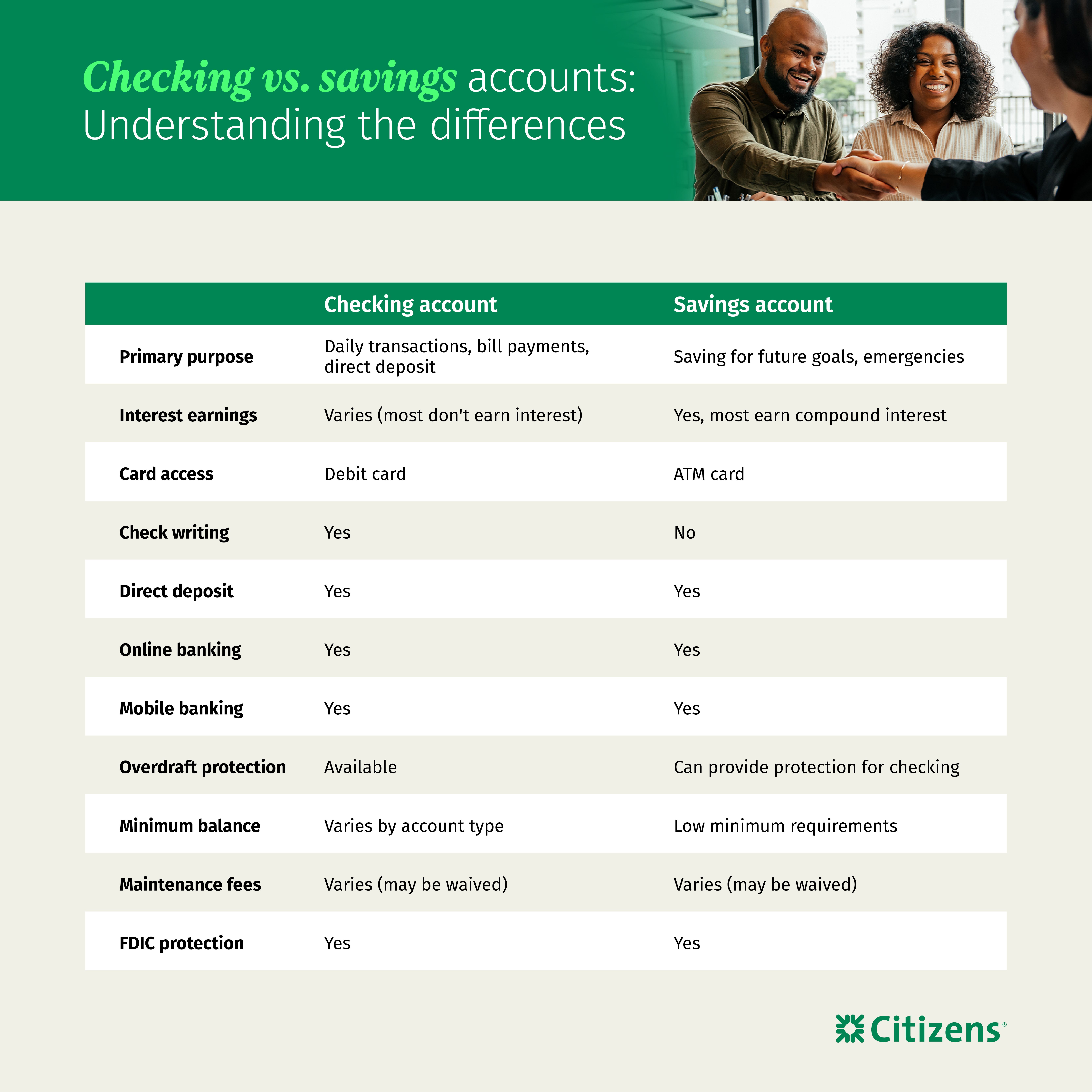

Checking vs. savings account at a glance

Checking and savings accounts both hold your money, but several important differences make them better suited for either spending or saving. Here's how they compare.

Checking account

A checking account is where most people keep their everyday spending money. You can use a checking account to receive paychecks through direct deposit, write checks and make online bill payments. It also comes with a debit card for convenient purchases.

A checking account typically offers:

- No withdrawal limits

- Online and mobile banking access

- A debit card

- Support for direct deposit

- Overdraft protection

- FDIC insurance

- Potential monthly maintenance fees

Savings account

You can use a savings account to set money aside for buying a car, covering college expenses, saving for a down payment on a home and other financial goals. It's also helpful for building an emergency fund, which can be an important financial lifeline when the unexpected happens.

A savings account typically offers:

- Interest earnings

- FDIC insurance

- Low minimum balance requirement

- Online and mobile banking access

- Potential monthly maintenance fees

Checking vs. savings account comparison

Take a look at how checking and savings accounts compare. Keep in mind that account features can vary depending on the bank and account type.

| Empty cell | Checking | Savings |

|---|---|---|

| Earns interest | Varies | Yes |

| Card access | Debit card | ATM |

| Check writing capabilities | Yes | No |

| Maintenance fees | Varies | Varies |

| Best used for | Everyday transactions | Savings |

What is a checking account?

A checking account is simply a holding place with easy access to your money by withdrawing cash, writing checks or making purchases. Some banks charge a maintenance fee, which may be waived if you meet certain requirements, like maintaining a minimum balance or regularly making deposits.

You can use checking accounts to receive a direct deposit from your employer, transfer money or connect a debit card for making purchases. Savings accounts can also receive deposits if you want to designate a portion of your direct deposit to checking and another part to savings.

Some checking accounts are geared toward specific categories, such as student checking accounts. They may have special fees and features to help with basic and more complex financial needs. It's a good idea to look into which particular type of account is right for you.

Benefits of a checking account

A checking account is often the starting point in establishing a relationship with a financial institution such as a bank or credit union. Here are some reasons to use a checking account:

- Online bill pay: This can eliminate paper statements and allows you to pay credit card bills from wherever you are, whether at home or on the go. It also provides an added layer of security and convenience that helps you pay bills on time.

- Ability to track transactions: Checking accounts have paper and electronic statements detailing every transaction. This allows you to monitor trends in spending, validate income and catch payment errors.

- Debit cards: With a debit card, transactions from your checking account — such as purchases and withdrawals — are deducted from what's already in your account. You can use debit cards to make purchases or withdraw money from an ATM, and you usually aren't limited to a certain number of transactions.

What is a savings account?

Savings accounts are intended more for longer-term savings goals rather than for everyday expenses. People often use them to save for special purchases or goals, like an emergency fund or a vacation. The goal with a savings account is to not spend the money on everyday purchases.

Some financial institutions require you to keep a minimum account balance and charge a fee if you don't. They may also limit savings account withdrawals or transfers to a certain number per month. But the trade-off is that you'll usually earn higher interest rates for leaving your money in the account. When you shop around to open a savings account, check the benefits, account requirements and fees.

Benefits of a savings account

A savings account is typically a better place to keep money you aren't using for everyday spending. It offers several benefits that can help you reach your short- and long-term goals:

- Earn interest: Unlike most checking accounts, savings accounts usually earn interest on your deposits. This allows you to take advantage of compound interest, where you earn interest on the interest you've already accumulated, which helps your savings grow faster.

- Create an emergency fund: Having a designated account for emergencies reduces the temptation to spend money as part of your regular expenses. Most experts recommend saving three to six months of expenses in an emergency fund. Interest-bearing savings accounts are the perfect place for that.

- Fund overdraft protection: You can link or anchor savings accounts to checking accounts to help cover any accidental overspending, helping you avoid overdraft fees.

- Expand your banking relationship: Some banks consider your total relationship or assets when determining things like fee rebates or lending decisions and may offer loyalty advantages for using multiple accounts and services.

Features shared by checking and savings accounts

While they both serve their own purposes, checking and savings accounts have many overlapping benefits. These vary by product and bank, but you'll find many common features.

Direct deposit

Direct deposit is the automatic transfer of funds from the account of someone paying you to your bank account, such as your paycheck from your employer. You usually set this up early in your employment, when you provide your account details to your workplace. You get the added benefit of not having to visit a branch in person or wait for a paycheck to clear, making the funds available faster.

Automated payments and transfers

Automated payments are prescheduled transactions on a certain date that pay a recurring bill from your bank account to a vendor or to a savings or investment account. Recurring bills could include payments for your electricity, phone, car, gym membership or streaming subscription. If you own your home, you may be able to set up your mortgage for automatic payment too. You can also set up automated transfers between accounts for savings goals, retirement goals or investments.

Mobile banking apps and notifications

Many banks provide an app for you to access your checking and savings accounts. These apps typically have notifications that usually include information about deposits, withdrawals or overdrafts. But they may also help you keep track of when checks are cleared, a failed purchase, a purchase made without your authorization or a suspicious change to your profile or login information.

How to use checking and savings accounts together

Although you typically use checking and savings accounts for different purposes, using them together helps you accomplish a variety of goals.

Simplify budgeting

Utilizing both a checking and savings account makes it easier to follow a budget. You can use online banking to track your checking account spending and spot purchases to cut back on or eliminate. You can also quickly see whether you're spending more or less than you planned in each budget category.

Having a savings account makes it easy to track your progress. To stay organized, you may want to open separate savings accounts for different goals — for example, one for college expenses, one for holiday spending and another for your upcoming wedding.

Separate spending and saving

Separating your money allows you to quickly see how much you have for groceries, gas, bills and other expenses, and how much you have for your goals. If you keep all your money in a checking account, there's no easy way to tell how much you've set aside for your daily spending needs and how much is for a savings goal. You might also be tempted to spend the money on unnecessary purchases, which makes it harder to save.

Transfer immediate funds to cover expenses

If your checking and savings accounts are with the same bank, you can easily transfer money between them. This can come in handy if your checking account balance is running low or if you need to cover an unexpected expense by transferring money from your savings to checking. You can still transfer money between accounts at different banks, but the process typically takes one to five days to complete.

Automate transfers to grow your savings

Transferring a portion of each paycheck to your savings account can help you grow your savings. Most banks allow you to set up automatic transfers from your checking to your savings, so your balance continues to grow even if you're busy and forget to add funds.

Set up overdraft protection

If your checking and savings accounts are with the same bank, you can link them to cover overdrafts. If you spend more than you have in your checking account, funds will be automatically transferred from your savings to cover it. This helps you avoid declined transactions or costly overdraft fees. Depending on the financial institution, a small transfer fee may apply.

Prepare for the unexpected

A dedicated emergency fund can help you quickly cover a car repair, home repair, medical expense or other bill you didn't see coming. It helps you avoid relying on high-interest credit cards that can be hard to repay if you can't pay the balance right away. With an emergency fund, you can quickly cover the expense, and then rebuild your financial cushion over time as your budget allows.

Checking vs. savings account FAQs

If you're wondering how to incorporate both checking and savings accounts into your financial plan, check out these frequently asked questions.

How secure are checking and savings accounts?

Banks protect accounts with strong security measures, including data encryption, secure online platforms, fraud detection and account alerts and monitoring. You can also enable two-factor authentication to prevent unauthorized access, even if someone has your password.

What fees do checking and savings accounts have?

The fees for checking and savings accounts vary depending on the financial institution.

Common fees include:

- Monthly maintenance fee

- Overdraft fee

- Minimum balance fee

- Inactivity fee

- ATM withdrawal fee

- Check reorder fee

- Stop payment fee

- Foreign transaction fee

Should I have my checking and savings account at the same bank?

Having both your checking and savings accounts at the same bank can make it easier to manage your money. You can quickly see your balances in one place through online or mobile banking, and transfers between accounts are usually faster when they're with the same institution.

Open your checking and savings accounts

Maintaining both a checking and a savings account is a smart financial strategy that leverages the strengths of each account type. By integrating both accounts into your financial plan, you can enjoy the benefits of seamless money management without having to choose between them.

Ready to open a checking account? Citizens has options for all your banking needs.

Related topics

How to create a budget

Managing your money wisely can help you reach your financial goals. Learn how to create a simple, effective budget.

How to set up direct deposit: A step-by-step guide

Direct deposit is a fast and simple way to receive your paychecks. Find out how to get started.

How to find your Citizens routing number and account number

Learn about your account number and routing number and when you may need to find them.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public, and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.