What is a debit card?

Key takeaways

- Debit cards make it easy to complete purchases without using cash, writing checks or charging to a credit card.

- Paying with a debit card won't lead to interest charges because it draws money from your checking account.

- Safeguarding your debit card number and PIN is just as important as protecting any other personal or financial information.

A debit card looks and acts like a credit card, but it's powered by your checking account. With a tap, you can make a purchase or complete bank account transactions at an ATM. You can also use debit cards to make online or in-app purchases. They're a convenient way to spend money from your checking account without using cash or checks.

Explore what debit cards can do, how they differ from credit cards and their advantages and disadvantages.

What is a debit card?

A debit card is a payment card issued by your financial institution and linked directly to your checking account. While it looks like a credit card and may display a major card network logo such as Visa® or Mastercard®, it functions more like a digital version of a check.

How do debit cards work?

When you use a debit card in person or online, the money is deducted from your checking account — usually within seconds. That means your spending is generally limited to your available balance. This is different from using a credit card, where you borrow against a line of credit and repay the amount later, usually with interest.

Beyond making purchases, debit cards also allow you to send money to another person, withdraw, deposit and transfer money at ATMs, as well as check your account balance.

How to use a debit card

When you open a checking account, you'll typically receive a debit card — either immediately at the bank branch or shortly after by mail. The card has a unique 16-digit number, separate from your checking account number, which enables electronic and digital transactions.

When you receive your card, you'll choose a PIN (personal identification number) or be assigned one. Your PIN acts like a password and is required for ATM transactions and sometimes for purchases. Keep your PIN private and shield the keypad when entering it to protect your account.

You can use a debit card by:

- Tapping, inserting or swiping it at checkout terminals

- Entering or storing your card number with merchants to make online or in-app purchases

- Adding it to a digital wallet* to use your smartphone or smartwatch for contactless payments

- Using it at ATMs to withdraw cash from your bank account

Because debit cards run on major payment networks, you can generally use them anywhere credit cards are accepted, although some merchants only accept certain networks like Visa® or Mastercard.®

Do you get charged fees for using a debit card?

Debit cards sometimes come with fees in addition to any checking account maintenance fees. Common debit card fees include:

- ATM fees: You may be charged a fee when making cash withdrawals at an ATM outside your bank's network. In some cases, both the ATM owner and your bank charge a fee.

- Overdraft fees: If you use your debit card to spend more than the available balance in your checking account and your bank covers the transaction, you may be charged an overdraft fee.

- Insufficient funds (NSF) fees: If a debit card transaction is declined because you don't have enough money in your account and your bank doesn't cover it, the bank may charge an NSF fee.

- Replacement card fees: Some banks charge a fee if you need an expedited replacement.

- Foreign transaction fees: When you make purchases or withdraw cash outside the U.S. — or even when transactions are processed in a foreign currency — you may be charged a percentage-based foreign transaction fee.

Unlike credit cards, debit cards typically don't require you to pay annual fees on the card itself. Your checking account may have one, but many banks offer ways to waive these fees.

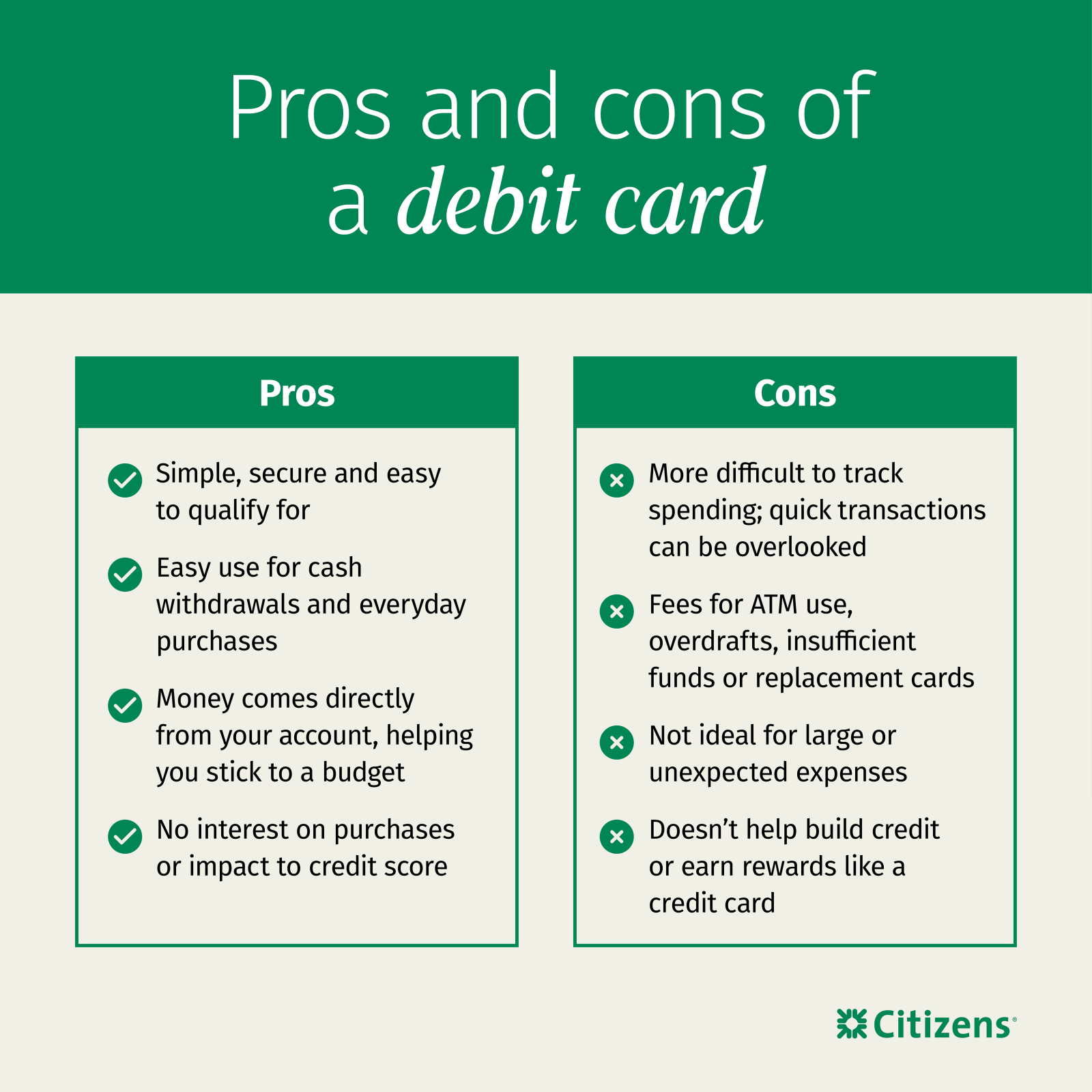

Pros and cons of debit cards

Debit cards offer a straightforward way to access the money in your checking account. Like any financial product, though, they come with both advantages and potential drawbacks. Here's a closer look at the key pros and cons.

Pros

- Convenience: Tap-to-pay technology and digital wallet compatibility make debit cards fast and easy to use.

- Versatility: A debit card doubles as both a payment method and an ATM card to withdraw cash.

- Security: PIN protection, chip technology, transaction alerts, zero-liability protection and contactless payments help safeguard your account.

- Budgeting: With spending limited to your available checking account balance, debit cards can reduce the risk of taking on debt or paying interest charges.

Cons

- Tracking your debits: Quick transactions and a lack of receipts can make it easy to lose track of spending, which increases the risk of overdrawing your account.

- Out-of-network ATM fees: Using an ATM outside your bank's network can lead to multiple fees.

- Not ideal for large or unexpected purchases: You can only spend what's already in your account, which can make it harder to cover big or surprise costs if you don't have enough funds available.

- No credit-building benefits: Unlike credit cards, debit card usage doesn't help you build a credit history or improve your credit score.

How is a debit card different from a credit card?

Although debit cards and credit cards can look similar and you can use them in many of the same places, they operate in very different ways:

- Source of funds: A debit card draws money directly from your checking account, so you can only spend what you have. A credit card uses a line of credit provided by the issuer, which you pay back later.

- Interest and debt: Debit card purchases don't incur interest because the money is taken from your account immediately. Credit card balances can accrue interest if not paid in full each month.

- Impact on credit: Debit card use does not affect your credit score. Responsible credit card use, such as paying on time and keeping balances low, can help build or improve your credit.

- Fraud and purchase protections: Both types of cards include security features, and protection from unauthorized use. The main difference is that disputed funds from your credit card are not immediately withdrawn from your bank account, where unauthorized charges on a debit card can temporarily reduce your available balance until the dispute is resolved.

- Fees and costs: Debit cards typically have fewer fees and no annual card fee. Credit cards may charge annual fees, interest, late fees or foreign transaction fees, depending on the card.

- Spending control: Debit cards limit you to the money in your account, which can help you stick to a budget. Credit cards allow you to spend beyond your account balance, which can be useful in emergencies but may increase the risk of overspending.

When to use a debit vs. credit card

If you're trying to decide when to use a debit vs. a credit card, consider each card's features that may make one a better fit than the other in certain financial situations.

When to use a debit card

A debit card might be a better choice if:

- You have enough money in your account. Using your debit card avoids interest charges and possible effects on your credit score.

- You're going to withdraw cash. Credit cards generally charge hefty cash advance fees.

- You want to use cash but don't want to carry it. Paying with your debit card is just as easy as using cash, as long as you track your balance and avoid unnecessary fees.

- You don't qualify for a credit card yet. If you qualify for a checking account, you qualify for a debit card.

When to use a credit card

A credit card might be a better choice if:

- You want pay-over-time financing. A credit card can let you break down larger purchases into affordable monthly payments.

- You're stacking up on credit card perks. It can be worth using your credit card to get the points, miles or cash back and then pay off the balance before you're charged interest.

- An unexpected expense comes along. If your emergency savings come up short and you don't want to pull a large amount out of your checking account, a credit card can bridge the financial gap.

Debit card FAQs

If you still have questions about debit cards, get the answers to frequently asked questions here.

Is a debit card the same thing as an ATM card?

No, a debit card isn't the same as an ATM card, though they do both allow you to withdraw cash from an ATM. A debit card is connected to your checking account and also enables you to make purchases. An ATM card may be connected to checking accounts, savings accounts or both, but you can't use it for purchases.

What happens if I overdraw my account with a debit card?

If you overdraw, or spend more than what’s in your account, you may be charged a fee every day that your account has a negative balance or for every purchase you make without available funds. If this happens, deposit money into your account as soon as possible to return to a positive balance. Some financial institutions offer overdraft protection, which links your checking account to another source, like a savings account or line of credit, to fund your checking account if it becomes overdrawn. However, this service often comes with a fee if you need to use it.

Can I stop a payment I made with my debit card?

No, there isn't a way to block a pending transaction from posting to your account. However, if that purchase was fraudulent or made without your authorization, you can't cancel it, but you can dispute the charge if you didn't authorize the transaction, were billed after canceling a service or didn't receive what you paid for.

How do I prevent debit card fraud?

To avoid becoming the victim of debit card fraud, don't share your card number or PIN with anyone. Avoid shopping on unsecured sites or while using public Wi-Fi. Check your account frequently for fraudulent activity or set up transaction alerts to review charges.

Use your debit card with ease

Debit cards are multifunctional money tools that offer convenience without the hassle of cash and checks or the interest charges of credit cards. With a Citizens checking account, you can get a debit card with fast and secure purchasing capabilities and mobile banking features that include the ability to change your PIN or freeze a card's activity. Find out more about Citizens debit cards.

Related topics

Is my debit card safe?

Keep your debit card and the money in your checking account safe by reviewing your transactions, using mobile wallets and turning on alerts.

Types of checking accounts: How to choose the best for you

When choosing a checking account, look at minimum balance requirements, fees and interest-bearing options to find the best fit.

8 bank fees explained and how to avoid them

Learn the most common bank fees associated with various bank accounts, and how to avoid them.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.

* Wireless carrier, text, and/or data charges may apply.

Mastercard and the circles design are registered trademarks of Mastercard International Incorporated.

Visa is a registered trademark of Visa International Service Association.

The Contactless Symbol and Contactless Indicator are trademarks owned by and used with permission of EMVCo, LLC