When to use credit vs debit card

Key takeaways

- Making on-time credit card payments can boost your credit score, which may help you qualify for loans and other opportunities.

- Credit cards offer stronger fraud protections than debit cards, and you typically aren't responsible for unauthorized purchases.

- A debit card helps you avoid debt by drawing funds directly from your account, which makes it easier to stick to a budget.

Although they look the same, credit cards and debit cards work differently. With a credit card, you can borrow money up to your limit and repay it over time. When you use a debit card, money is immediately drawn from your checking account.

Credit cards and debit cards are both secure, convenient ways to manage everyday spending. However, there are some situations where one may be a better choice than the other. Both cards have unique benefits, and it's important to understand the credit vs debit differences so you can make the most of each one.

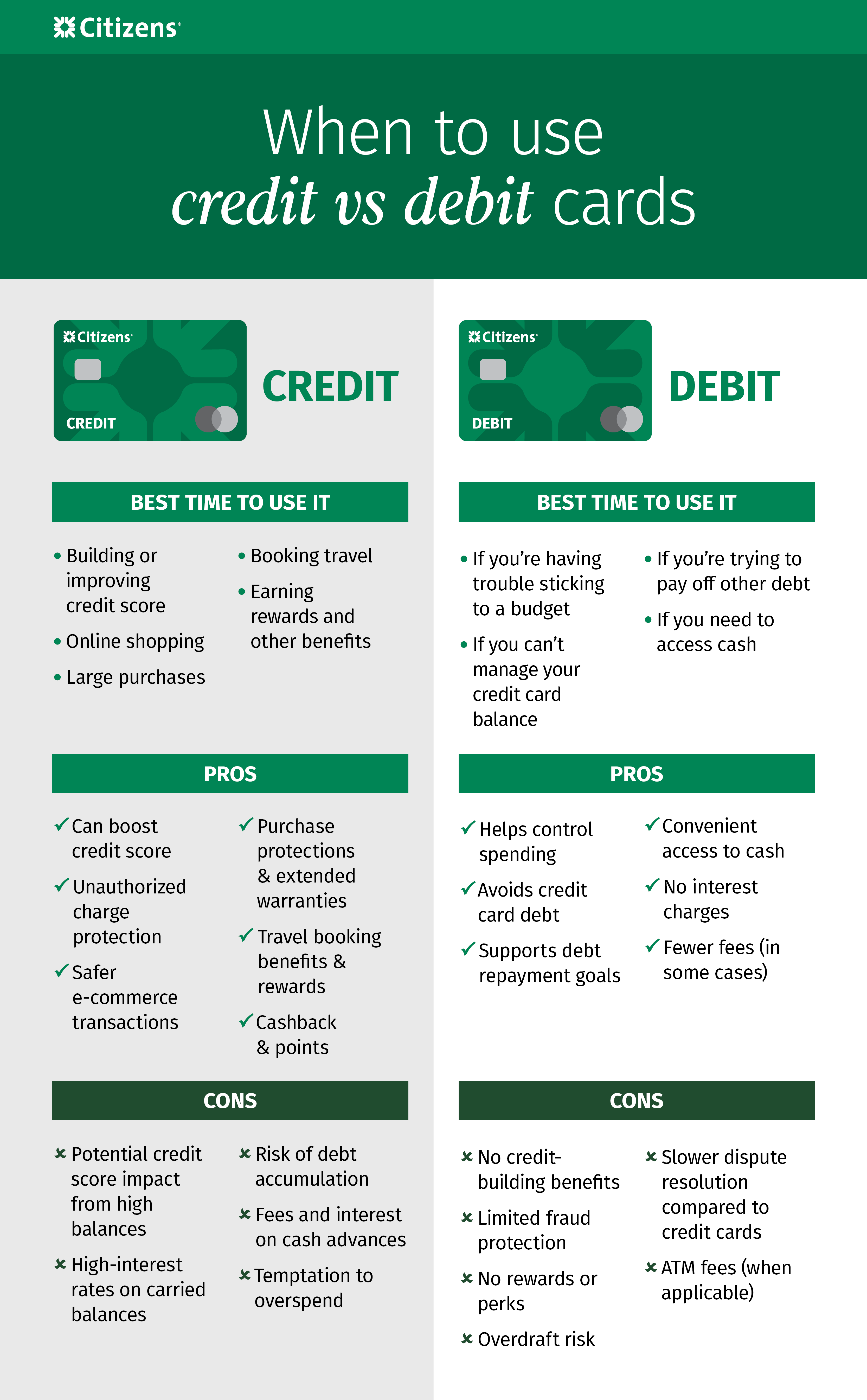

When you should use your credit card

Credit cards offer several important benefits that debit cards can't match. That's why many people use them for the majority of their purchases.

A credit card can help improve your credit score, which is essential for qualifying for loans, like for a home or car. When you consistently make on-time payments and keep your balance low, the activity is reported to the credit bureaus, which benefits your score.

If lost or stolen, credit cards typically have zero-liability policies, which protect you from unauthorized purchases. They are also safer for e-commerce transactions if you need to dispute a charge. Your money won't be tied up while the card company investigates. Although debit cards are safe, the disputed amount is withdrawn immediately, and you may not get it back until the claim is resolved.

Credit cards offer valuable protections that make them ideal for large purchases. Purchase protection covers damage or theft, and certain purchases may qualify for extended warranties. You'll also need a credit card to book flights, hotels and rental cars.

One of the most popular credit card benefits is earning rewards. Many cards allow you to earn 1-2% cash back on qualified purchases. You may also earn points that can be exchanged for merchandise or used for airfare, hotels and rental cars. Some cards also offer sign-up bonuses, like 0% APR for an introductory period or points for spending a certain amount within the first few months of opening your account.

When you should avoid using your credit card

While credit cards offer many benefits, they aren't ideal for all situations, like if you struggle to manage your balance. Credit cards typically have higher interest rates than other borrowing options, like personal loans. The longer you carry a balance, the more it can grow, which makes it more difficult to pay off.

Ideally, you should aim to use no more than 30% of your credit limit at any given time. This not only protects you from taking on too much debt, but it also tells the credit bureaus that you aren't too reliant on credit, which can help your credit score.

Using a credit card for cash advances is a more expensive way to borrow money. Most cards charge a fee of 3% to 5% of the amount you are withdrawing or a flat fee. The interest also starts accruing immediately.

Having easy access to credit can also lead to impulse purchases if you aren't careful. Swiping a card or entering your card details online makes it easy to buy things you don't need. If you are tempted to overspend, stay within your limit by using a budget and paying with cash or a debit card.

When you should use your debit card

Sometimes, it's better to use a debit card than a credit card, like when you're having trouble sticking to a budget. A debit card can help you stay on track since funds are drawn from your checking account. You can also check your balance anytime online or with the Citizens mobile banking app*.

If you are carrying a credit card balance or other debt that you are struggling to pay off, a debit card may help you avoid taking on new debt. It prevents overspending because you can only spend what's in your account. This may help to free up room in your budget to make larger payments toward your debt.

A debit card also makes it easy to get cash from an ATM when you need it. Unlike credit card cash advances that come with withdrawal fees and interest, you can use your debit card to make surcharge-free withdrawals from your bank's ATM network.

What are the limitations of using your debit card?

While debit cards can help you avoid debt, they do have some limitations. One is that they don't help you build your credit score. Unlike your credit card payments, which are reported to the credit bureaus, debit card transactions are not reported.

Debit cards are also linked to your checking account. If you spend more than you have in your account, you may be charged an overdraft fee or the transaction may be declined. You may also be charged a fee if you withdraw cash from an out-of-network ATM.

Credit vs. debit card: What else to consider

Choosing when to use using credit vs debit card depends on how each option fits into your lifestyle and financial goals. Credit and debit cards are both convenient payment options, but what should you consider?

Your balance

With a debit card, you must keep a watch on your balance. Low balance alerts can help avoid overspending and overdraft fees. You can also set up overdraft protection, which automatically transfers funds from your savings account to your checking account to cover transactions.

Small purchases

For everyday purchases like groceries and small items, credit cards may provide cash back or points. However, credit cards can make it easy to overspend, especially when making frequent small purchases. Additionally, some small merchants may charge a small processing fee for both credit and debit cards. Also, some merchants place temporary holds on your funds, which can affect your available account balance.

Travel

Credit cards are better for traveling because they offer stronger fraud protections. They may also waive foreign transaction fees. Also, if a hotel or car rental company places a temporary hold on your credit card when you make a reservation, it will only impact your available credit. Using a debit card will impact your account balance.

Convenience

A convenient way to simplify your finances is to bundle your credit card, checking and savings accounts with Citizens. Keeping all your accounts in one place makes it easy to manage your finances. You can also monitor your account for fraud or set alerts in one online platform.

Lifestyle and financial needs

Your financial goals are the most important factor when choosing credit vs debit. For best results, consider using both cards, depending on your needs and current financial situation. If you are focused on living debt-free, you could use your debit card for most purchases and use your credit card for traveling to take advantage of fraud protection. It doesn't have to be an either/or choice. You can use each card when it makes the most sense.

Find a credit card that fits your needs

Credit cards and debit cards both have advantages, and the right one depends on your needs and goals. Whether you're looking for rewards, low rates or convenience, Citizens offers a variety of credit card options. Explore the full selection of credit cards to find the one that's right for you.

Related topics

3 credit card habits to help build a solid credit score

A strong credit score can open many doors. Learn how to boost your score to increase your chances of getting approved for loans, credit cards and more.

How do cash back credit cards work?

With cash back credit cards, you can earn valuable rewards for your everyday spending. Find out how these cards put money back in your pocket.

Should I use my credit card for everything?

Credit cards offer advantages that cash and debit cards can't match. Find out why some people use their credit cards for all of their purchases.

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public, and is not legal advice or a substitute for legal counsel, nor does it constitute advertising or a solicitation. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.

Mastercard and the circles design are registered trademarks of Mastercard International Incorporated.

Credit Cards are issued by Citizens Bank, N.A. pursuant to license by Mastercard International Incorporated.

* Wireless carrier, text and/or data charges may apply.