How to catch a (tax deduction) break on your student loans

Key takeaways

- The student loan interest deduction is a federal deduction that could allow you to deduct up to $2,500 in student loan interest on your 2019 taxes.

- Qualified interest will be deducted right from your taxable income, potentially earning you a bigger refund.

- Eligibility is based on your modified adjusted gross income (MAGI) and tax filing status.

College was fun. Student loan payments — and the interest that comes with them — not so much. But this tax season, there may be a way to earn back some of that money you paid in interest in 2019 and put a little more cash in your pocket. That's thanks to a special deduction created to provide relief for some 44 million student borrowers: the student loan interest deduction. It could help you potentially deduct up to $2,500 in interest paid on your student loans in 2019 — which could translate to as much as $550 in extra money for you, if you're in the 22% tax bracket.

But before you make plans for that extra cash, you need to read on to learn more about how the deduction works and determine your eligibility. While that may not sound fun, it could be really helpful when you file your taxes.

Ready? Let's do it…

What is the student loan interest deduction?

If you're just starting your career, this federal tax deduction, which was reinstituted with the Taxpayer Relief Act of 1997 and maintained with the Tax Cuts and Jobs Act (TCJA), can be a pretty big deal. It allows you to deduct student loan interest paid in 2019 — including both required and prepaid interest — on any of your qualifying student loans (federal and private loans), up to a maximum of $2,500. The term "deduction" is a fancy way of saying that the qualified interest you paid (subject to limits) could be subtracted directly from your taxable income on your return.

What does that mean for you? It means you'll have to pay less tax, which, depending on how much tax you already paid out in 2019, could score you a bigger refund … or lower the amount you owe, if you have to pay.

This deduction is not something you have to itemize as an expense on your taxes; it's subtracted right from your taxable income. That means if you qualify for the deduction, you can still deduct your eligible student loan interest even if you choose to take the standard deduction on your taxes. If that all sounds good, keep reading, because the amount you can deduct is impacted by a few important factors, including your income and your filing status.

What's the income limit for the student loan interest deduction?

Though the student loan interest deduction allows you to deduct a maximum of $2,500 in student loan interest paid, you may not be able to deduct the full amount. The amount you can claim is subject to annual income limits, which could reduce — or completely eliminate — the amount of student loan interest you can deduct. The income limit is based on your modified adjusted gross income (MAGI).

MAGI is the way the IRS determines your eligibility for certain deductions, including the student loan deduction. It's calculated by taking your adjusted gross income and adding back tax-exempt interest income and certain deductions. These deductions could include student loan interest payments, deductions from IRA contributions, or foreign income.

So, for example, if your adjusted income is $50,000 and you paid $500 in student loan interest that you claimed as a deduction, your MAGI would be $50,500.

For tax year 2019 (the taxes you file in 2020), the MAGI threshold was increased to $70,000 for single filers. So, if your MAGI was $70,000 or less in 2019 and your tax filing status is single, you could potentially deduct the full amount of qualified student loan interest you paid, up to a maximum of $2,500. If, however, it falls between $70,000+ and $85,000, you could qualify for a partial deduction. Anything above $85,000 would not qualify for any student loan interest deduction.

While the maximum deduction amount of $2,500 has not changed since tax year 2018, the income brackets have increased. The chart below highlights the differences for single heads of household and married couples filing joint returns.

2018 vs. 2019 Student loan interest deduction MAGI limits

| Filing Status | MAGI limit for student loan interest deduction in 2018 (filed in 2019) |

MAGI limit for student loan interest deduction in 2019 (filed in 2020) |

|---|---|---|

|

Single, head of household, qualified widow(er) |

$65,000 or less, full deduction $65,001 - $80,000, partial deduction $80,001 and up, no deduction |

$70,000 or less, full deduction $70,001 - $85,000, partial deduction $85,001 and up, no deduction |

|

Married filing jointly |

$135,000 or less, full deduction $135,001 - $165,000, partial deduction $165,001 and up, no deduction |

$140,000 or less, full deduction $140,001 - $170,000, partial deduction $170,001 and up, no deduction |

How to calculate the student loan interest deduction

Again, the deduction you'll qualify for will depend on your income (as shown in the MAGI chart) and filing status. It also depends on other qualification factors (which we'll discuss later). Assuming you meet those requirements, you would calculate the amount of your student loan deduction as shown in the examples below:

- Example of full deduction: If your MAGI was $50,000 (below the $70,000 threshold) in 2019 and you paid a total of $700 in student loan interest, you could deduct the full amount of interest, $700, of your taxable income on your return filed in 2020. If, however, the interest you paid on your student loans was $2,700, you would only be able to deduct $2,500, since this is the maximum amount allowed. The amount you can deduct will always be the lesser of the interest you paid or $2,500.

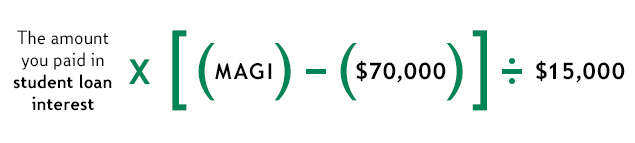

If, however, your MAGI was more than $70,000 but less than $85,000, you would be eligible for a partial deduction. To calculate that, you need to apply a formula. That formula is as follows:

[The amount you paid in student loan interest ] x [(the amount of your MAGI) - ($70,000)] / [$15,000]

- Example of partial deduction: Let's assume your MAGI was $75,000 and the student loan interest you paid in 2019 was $1,000. Using the formula above, you would take $1,000 (the interest paid) and multiply it by $5,000, then divide that answer by $15,000. The result would be $333, which is the amount you could potentially deduct from your taxable income on your 2019 return.

NOTE: If you prefer not to "solve for X" on your own, you can use this handy student loan interest calculator to calculate the interest you could potentially deduct.

What are the eligibility requirements for the student loan deduction?

The student loan interest deduction could be taken by you (the student) or your parent(s) if they're making payments on your behalf as their dependent. But to qualify for the deduction, you have to meet these requirements (courtesy of our friends at the IRS):

- You paid interest on a qualified student loan in 2019. That means if Bank of Mom or Dad provided you with a loan for school and charged interest, you wouldn't be able to take the tax deduction. Nor could you deduct interest on higher education loans provided by your employers.

- You're legally obligated to pay interest on the student loan. If you had a cosigner on the loan, such as your parent, you cannot both take the deduction. It's one or the other.

- The loan had to be for you, your spouse, or a dependent.

- You and your spouse, if filing jointly, can't be claimed as dependents on someone else's federal tax return.

- Your tax filing status cannot be married filing separately.

- You must have been enrolled at least part time in school.

- The loan had to be paid or incurred with a reasonable period of time before or after you received it.

- The loan was used for qualified educational expenses, such as tuition, fees, books, supplies, and equipment.

It's important to note that the student loan interest deduction applies both to interest you pay on qualified federal and private student loans as well as graduate and undergraduate loans.

Wondering if you qualify? The IRS has an interactive tool to help you determine eligibility for the student loan deduction.

How do you file for the student loan tax deduction?

When filing your 2019 taxes, you'll need to provide supporting documentation regarding deductible student loan interest. If you paid $600 or more in interest, the servicer of your loan will automatically send you Form 1098-E by January 31 to use when filing your taxes. Note that if you paid less than $600 in interest, you won't receive the form — but you can still deduct the interest. Your student loan servicer(s) can provide you with the total amount of interest you paid.

If you use TurboTax to prepare and file your taxes, you should have your 1098-E(s) available. You'll also have the opportunity to add in interest not reported on 1098-Es (amounts less than $600). If, based on the information you provide, TurboTax determines you're eligible for the student loan interest deduction, it will automatically add the amount to your required tax forms.

Ready to help put more cash in your pocket?

There's no question: Student loan interest can be a drag. But even if you don't qualify for the student loan interest deduction, you may have an opportunity to refinance and save on the interest you pay. To learn more about the Citizens Education Refinance Loan® and the benefits of refinancing, call 1-877-405-2262 to speak with one of our Student Lending Specialists.

Related topics

Student loans or retirement: where should your money go?

To refinance or not to refinance student loans?

How to budget for a mortgage with student loans

© Citizens Financial Group, Inc. All rights reserved. Citizens Bank, N.A. Member FDIC

Disclaimer: The information contained herein is for informational purposes only as a service to the public, and is not legal advice or a substitute for legal counsel, nor does it constitute advertising or a solicitation. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.